Typically, we’ve used this serial to highlight overbought and oversold conditions on sector funds, thematic funds, macro indices and individual stocks to highlight short-term dislocations that we think investors can take advantage of. We wanted to switch gears to focus on longer-term themes that have alpha generating implications for equity and blended strategies. While themes usually involve specific factor characteristics or industry/product cycle characteristics, we want to start at a higher level. The most obvious theme that is dominating US equities is the bull trend that has taken the S&P 500 to new all-time highs on 46 different days this year. We want to show some examples of how equity sector funds really shine vs. Fixed Income when equities are in a sustained bull trend as they are now.

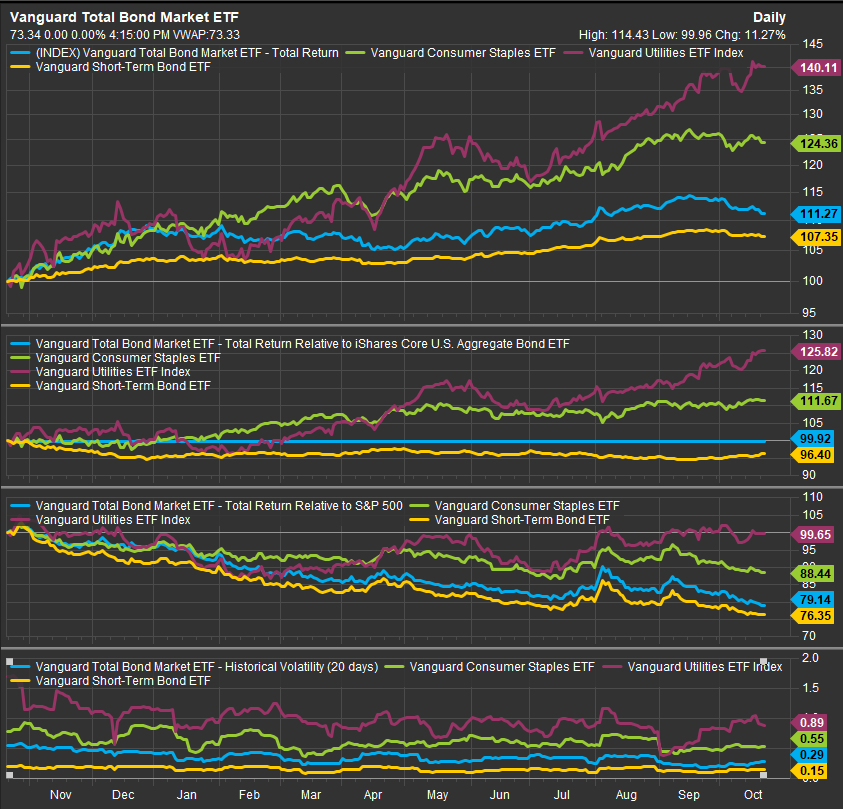

The chart below shows a comparison of two bond ETF’s, Vanguards Total Bond Market ETF (BND), Vanguard’s Short-term Bond Market ETF (BSV) and Vanguard’s Large Cap. Consumer Staples ETF (VDC) and its Utilities Sector ETF (HVJ). We’ve measured them against each other on 4 metrics; Indexed Total Return, Relative Performance vs. AGG (ETF), Relative Performance vs. S&P 500 and 20-day volatility. The takeaway here is that min vol. equities provide compelling outperformance vs. Fixed Income in bull trends along with some income generation and volatility profiles that can approach low levels of traditional bond funds.

We think this comparison is worth highlighting as large cap. defensive sectors like Utilities and Staples are comprised of large liquid companies that operate in established industries. Utilities are heavily regulated and function as monopolies or oligopolies in their respective geographies. They do face risks from natural disasters and other exogenous events, but they generally have a captured customer base, and they sell an essential product. Staples haven’t been quite as strong a performer as Utilities, but performance in 2024 has doubled up both BSV and BND despite Staples being one of the weakest performing sectors vs. equities.

There are certainly risks with pushing some traditional fixed income allocation into an equity product. Near-term volatility and market risk are somewhat higher with equities. But there are times in the business cycle and the market cycle where the risk/reward calculus becomes favorable, and we believe we are in one of those periods presently.

Supportive Fed

The Fed has shifted focus to helping Main Street grapple with affordability. Rates moved lower over the summer in anticipation of contractionary pressure on the economy, but now that policy has been unveiled rates have backed up. We think this is a dynamic that will be here with us for a sustained period of time as the optimism surrounding dovish policy will keep rates higher than the Fed wants and will keep policy makers in a supportive stance as major price increases over the past 5 years continue to be digested by the Consumer.

While the Fed is a boon to equity investors in the near-term, its policy intervention is creating a feedback loop which is a headache for fixed income investors. The optimism for equities at the advent of dovish interest rate policy is a headwind for bond performance. On the one hand, the Fed wants rates (and yields) lower, but on the other hand, investors get more bullish and more up the risk curve, selling treasury bonds for assets with higher return profiles like equities. Given the amount of passive product in the equity market, index funds would propel all sectors higher on an asset-class level trade. Dovish policy usually motivates investors to sell bonds and buy equities.

Housing Crunch

One thing keeping the economy motivated in the US is the shortage of single-family homes for sale at prices that average Americans can afford. We touched on this in our weekly market letter mentioning the strong performance of Homebuilders over the past 2 years vs. other Consumer segments like Retail, Leisure and Auto’s. The housing market dynamics are likely to keep pressure on the Fed to maintain dovish Interest Rate Policy as interest expense on top of high housing prices is an affordability killer for the average US household. The other factor here is the labor and material input demand of the homebuilding industry. We’d expect housing demand to underpin a bid for commodities throughout this cycle that could make it hard for the Fed to influence pricing at the market level.

Full Employment

And finally, structural demand for housing is a key driver of potential expansion. There is a lot of demand for homes. There has been a lot of family formation over the past 5-years despite the pandemic and inflation pressures, and we still have a robust employment picture in the US. With the Fed trying to lower costs without damaging the economy, we don’t see a high potential for a market clearing event like a credit crunch at this time.

Conclusion

Given an inflationary overhang that has crimped the housing market, a dovish Fed and an US economy at or near full employment, we think the equity bull trend is set up to run into 2025. Tactically, we recommend considering lower volatility equity sectors as a way to add capital appreciation characteristics to a portfolio or strategy while still enjoying a lower volatility profile than broad equities and some income generating characteristics as well.

Data sourced from FactSet Research Systems Inc.