We introduced the Elev8 Sector Rotation Model in June. Here’s a look under the hood at the inputs we use to score the 11 GICS Sectors for December and our resulting positions. We’ve streamlined the model slightly since inception to include up to 14 indicators that range from stock level technical, macro-overlays for equity trend, interest rate trend, commodities trend and USD trend, relative performance vs. the benchmark S&P 500 and overbought/oversold oscillators.

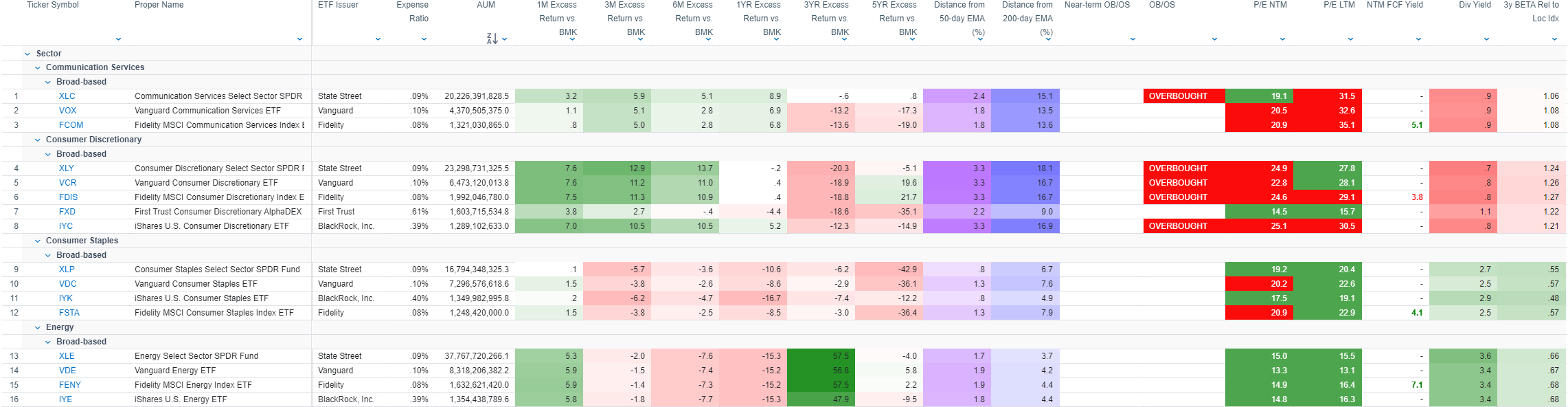

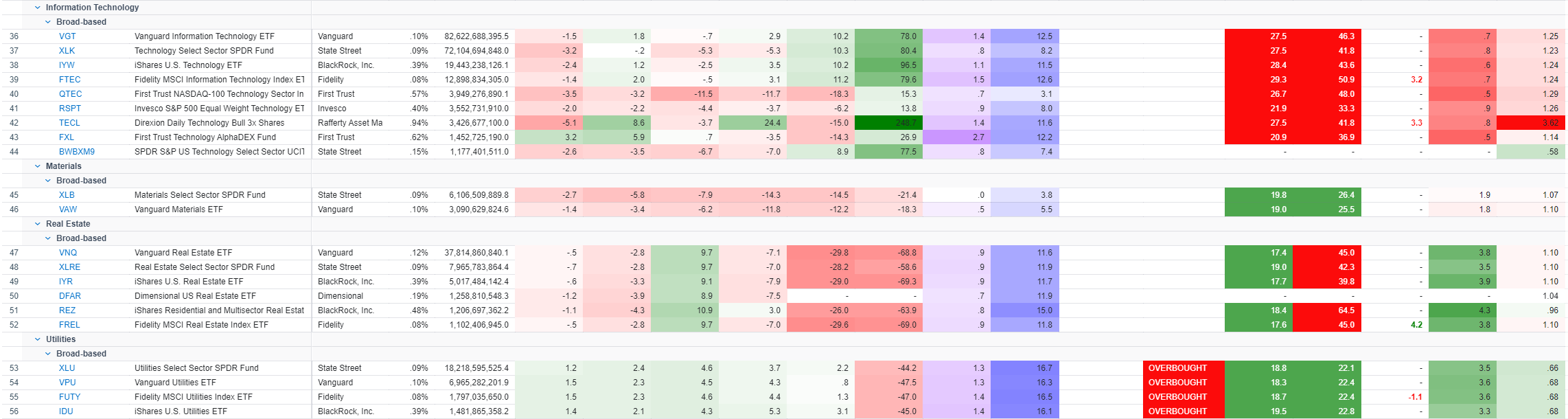

This month we’ve tweaked the process for sector fund selection. We have been using the SPDR Sector fund family as our sector proxies for Elev8. We have adjusted our process to use the largest passive sector-based ETF by AUM ($) for each sector as our proxy for Elev8 sector positions moving forward. This adjustment has us swapping out XLK and XLRE for VGT and VNQ as the latter are the largest sector funds replicating the US large cap. Information Technology and Real Estate Sectors respectively. Check out our appendix at the bottom of this report for the largest 58 sector themed ETFs and their near-term and long-term performance!

Elev8 Model Input Scores: December

The table below shows the model’s scores for December. Communication Services, Financials, Discretionary and Technology continue as overweight positions. Industrials climbed the rankings and is a top 3 overweight this month. Our zero-weight sectors for December are Materials, Energy and Healthcare. These sectors scored the lowest in our model. Energy and Materials Sectors got some boost from the election, but commodities and crude prices remain weak. We have seen a loss of near-term upside momentum in interest rates as well, and we expect lower vol. exposures, Growth exposures and consumer adjacent exposures will get some near-term relief from rates moving lower into year-end. Rates going higher would be a signal we are errant in our prognostications and would have us eyeing a rebalance.

Key: Pattern = L/T (1yr+) Price Pattern of the Sector ETF, Mean Rating = simple average of 1-6 ratings (buy–>sell) of all stocks within the sector, WTD Mean Rating = Cap Weighted Sector Constituent rating, OB = Overbought, OS = Oversold, N=Neutral

Model Input Commentary

With equities strong through November generally, pattern scores have improved broadly as they reflect absolute price. Our “Mean Rating” and “Wtd Mean Rating”, reflect an equal and cap. weighted evaluation of every stock in each sector. They are then scored against the average score across all 11 GICS sectors to get a plus-1, minus-1 input into the scheme. This is the stock level message from each sector. It is confirmed in the model through a higher-level relative strength score at the sector and industry level which is a 3-level scheme (+1, 0, -1). XLP, for example, is buoyed by exceptional performance from just 2 stocks, COST and WMT, but since they are major players, they have an outsized influence on sector performance in aggregate. A similar phenomenon occurs within the Comm. Services Sector as Alphabet, Meta and Netflix wield outsized stock-level influence.

At the macro level, the established trends in place continue to be bullish equities and lower commodities prices. Yields are in consolidation and have potential to pivot higher or lower from here. Given the enduring weakness in commodities prices, we are anticipating yields to move lower this month.

Under the “Output” section we have a “Tactical” column that adjusts certain sector scores for dislocations we perceive will affect the market in the near-term. This month we have no tactical overlays, and the raw model scores are the final scores.

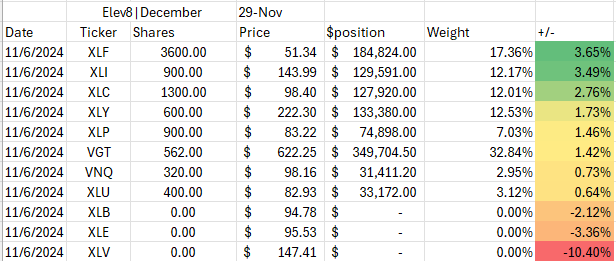

Elev8 Sector Rotation Model Portfolio: December Positioning vs. Benchmark Simulated S&P 500

Previous Positioning as of last Rebalance: November 6, 2024

Our month-end review of our 14 Elev8 Sector Rotation Model inputs results in a paring of our long exposure in Technology and Discretionary Sector shares and increasing exposure to Communications Services. We’ve maintained our overweight position in Financials, Industrials, Utilities and Real Estate, and with weak earnings hitting the tape at the end of the month and Commodities prices retreating we have gone zero-weight both Energy and Materials to start the month. Our final zero-weight sector remains Healthcare, which, similar to Staples, is deeply oversold.

At a high level this allocation leaves us exposed to underperformance risk from a macro scenario of downside correction in equities particularly if inflation pushes rates higher as that happens. We are also negatively exposed to any potential spike in Oil prices in the near-term. In exchange for the risks, we are positioned for a continued bullish expansion while keeping some lower vol. stocks in the portfolio as we anticipate yields are overdone to the upside in the short-term. We are aligned generally with historical beneficiaries of rising equity prices and falling interest rates. We also continue to like Financials as a reflationary play from their trough in 2023. Please read through our model input commentary for details.

Sector Rotation Model Weights and Share Counts by Fund Family

For those interested in replicating our results, but contractually tied to one fund family or another, we replicate our monthly positioning for SPDRs, Vanguard and iShares Sector fund families. The model weights and share counts for each family are as follows:

Conclusion

November saw Donald Trump gain the US Presidency for the 2nd time and the longer-term bull trend for equities continue with the S&P 500 registering multiple new all-time highs during the month. We expect some bullish momentum to carry us into year-end and we intend to be overweight upside exposures. We are short Energy, Materials and Healthcare this month, betting that weak trends will stay weak into the new year. Please keep an eye on etfsector.com for December’s S&P 500 and Large Cap. Sector insights where we identify key outperformers and the biggest potential drivers of future performance.

Appendix: US Domiciled Large Cap. Sector Funds w/ Performance Data and Metrics

Data from Factset Research Systems Inc.