May 25, 2025

The S&P 500 is attempting bullish reversal after a near 20% correction from February through early April. As May progresses, equities have begun a consolidation. The chart below outlines the pivot zone between 5671 and 5783. Both levels have functioned as support and resistance during the previous twelve months’ price action.

Another important level is 5504 which is the neckline for bottom formation and a point where market participants began discounting a recession due to a potential collapse in normal trading relationships (chart below).

Our base case is continued reflation towards new highs with a >50% chance of finishing 2025 with gains based on the current trajectory of negotiations and agreements. We think the primary risks to that scenario stem from inflation risk that could lead to stagnation in the lending market. We think the residential housing market is vulnerable to affordability issues if rates stay at present levels. However, we remain positive due to the relatively low levels of stress in our credit indicators, strong employment and corporate earnings.

Concerns: Rates, Housing, Consumer

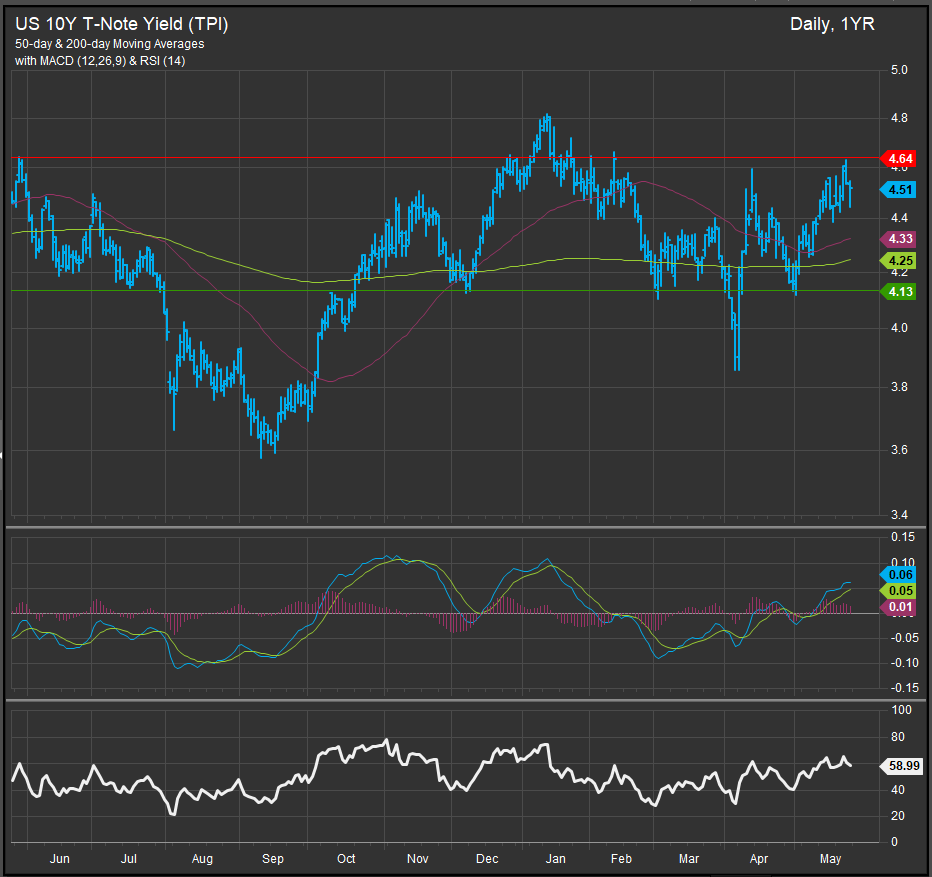

Rising rates have been a persistent concern in this cycle, coming off the 2022 bear market. In 2024 when 10yr Yields moved above the 4.7% level, equities typically corrected on inflation concerns. Yields (US 10yr, chart below) have been moving higher since trade reconciliation started to gain momentum. Equity correction has come with falling rates.

Housing related stocks are important weights in the Discretionary, Materials and Industrial Sectors. With US 10yr yields remaining above the 4% level and 30yr Mortgage rates still well above 6% in most areas, the housing market has stagnated. The stock charts of big builders like Lennar Corp. (below) reflect the dual headwinds of stubbornly high rates and high costs.

With government yields still above 4%, the cost of capital is still a headwind to the mortgage market and to consumer spending. Tariffs themselves are also a cost that will be transferred as much as possible to the consumer, Our opinion is that rates need to move lower in order for the cycle to sustain expansion.

Positives: Credit Indicators Firm, Strong Employment, Technology Innovation

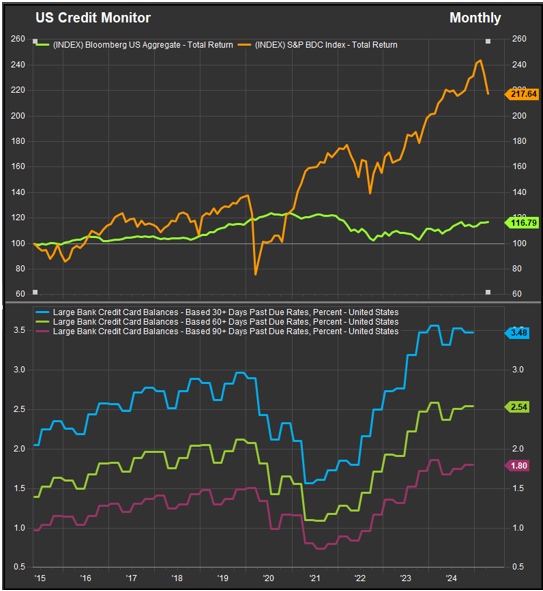

Global trade concerns have challenged 2024 consensus assumptions around a soft landing and an easy Fed, causing rotation into lower vol. assets in the first half of 2025. However, traditional credit indicators like the % of credit card delinquencies are still short of levels that have historically correlated with recession…In both 2001 and 2008 credit card delinquency rates were above 4.5%, while the chart (below) shows the series flattening out in 2024 around the 3.5% level.

The unemployment rate, while rising in the near-term remains low by historical standards below 5% while average hourly earnings have continued to climb into 2025. There’s not enough deterioration in the former to cause significant concern. We think a risks are likely to be inflationary catalysts.

Finally, while there are some signs of late cycle behavior from our economic indicators, the AI cycle continues to mature. The technological promise of AI has been optimistically discounted by the market for several years. The efficiency gains are a potential driver of growth for many business lines. WMT has been one of the biggest users and implementers of AI based solutions in its staffing and supply chains. Wall-Mart has benefitted from consumer “trade-down” trends, but it has also made gains on earnings efficiency and growth. The stock (chart below) has been a long-term outperformer.

US Tech stocks also continue to lead when equities are in “risk-on” mode. 2023 and 2024 saw broad strength across the semiconductor complex. That broad enthusiasm has narrowed, but stocks like AVGO, PLTR and NVDA continue to be accumulated on pullbacks.

Conclusion

Global trade tensions have highlighted the specter of stag-flation, but with conciliation gaining momentum there is a path forward towards expansion. The consumer is slowly getting squeezed, but credit indicators and income remain firm. We continue to be constructive on the cycle despite concerns about rising rates.

Patrick Torbert, Editor & Chief Strategist, ETFSector.com

Data sourced from FactSet Research Systems Inc.