October 30, 2024

The technology sector has once again pulled ahead of the market. Over the past three months, the S&P 500 Information Technology Index has gained nearly 7 %, while every other major GICS sector has either been flat or negative, according to data from S&P Dow Jones Indices. That divergence reflects a familiar combination of fundamentals, fund flows, and investor psychology: tech remains the only sector with both structural earnings growth and consistent capital inflows in a market defined by uncertainty elsewhere.

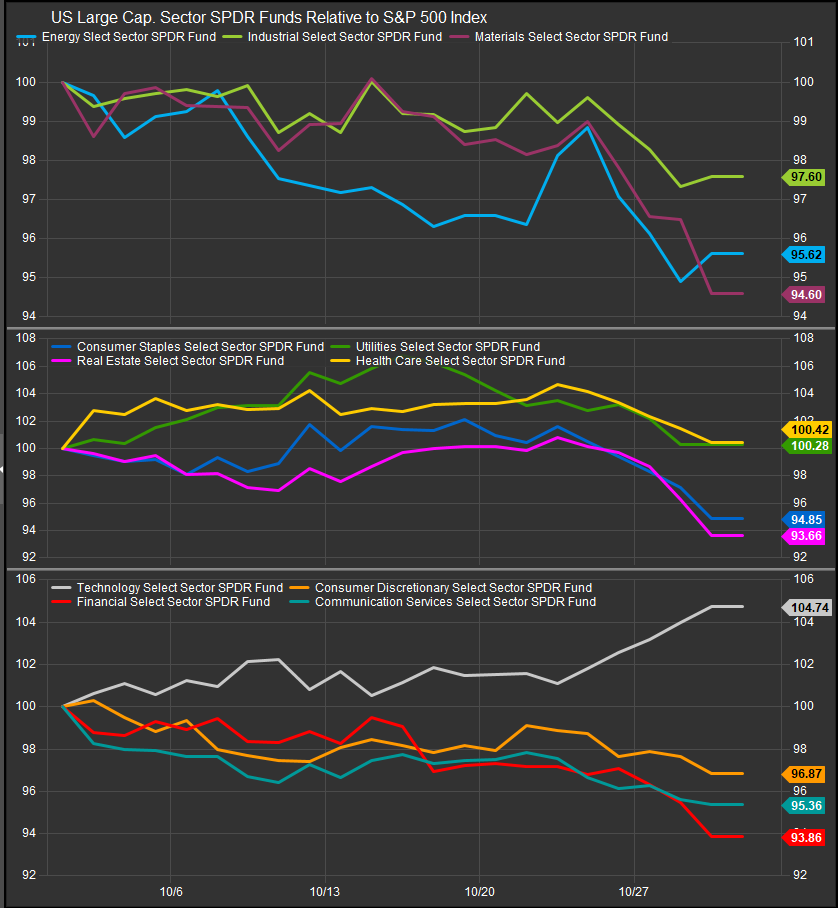

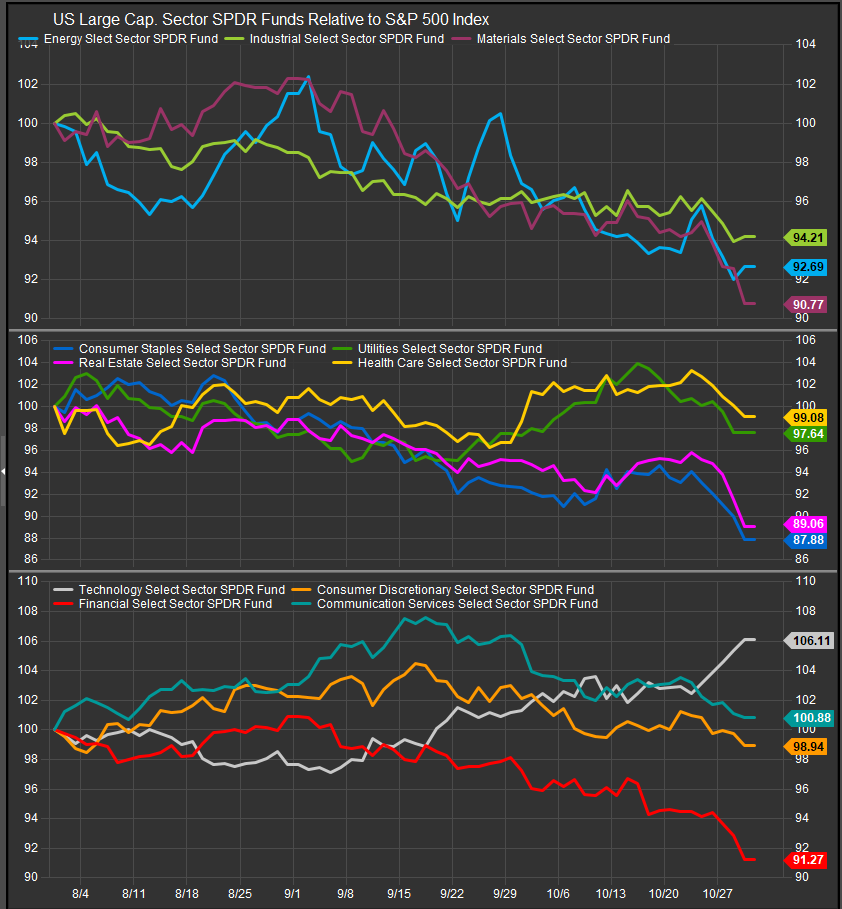

Sector Performance (Trailing 1 Month)

Sector Performance (Trailing 3 Month)

Sector Performance (Trailing 6 month)

Relentless Fund Flows

Investor appetite has been remarkably concentrated. Morningstar’s U.S. fund-flow dashboard shows that technology sector mutual funds and ETFs have pulled in roughly $36 billion in net inflows YTD 2025, while most other sectors have seen net outflows exceeding $60 billion.

State Street Global Advisors’ SPDR Sector and Industry Dashboard (Q3 2025) reports that the Technology Select Sector SPDR (XLK) alone captured over $8 billion in fresh inflows between April and September—more than the combined net inflows of the next four largest sector ETFs. BlackRock’s Flow & Tell series similarly identified technology as the top sector recipient of global ETF inflows for five consecutive quarters, underscoring how institutional portfolios continue to consolidate around a narrow group of growth leaders.

Superior Earnings Momentum

The inflows are grounded in fundamentals. FactSet’s Earnings Insight (October 2025) shows S&P 500 Information Technology EPS growth at +23 % year-over-year, compared with +6 % for the broader index. The sector’s profit margins average 23 %, versus 11 % for the S&P 500, while revenue growth near 8 % outpaces every other sector. McKinsey’s Technology Trends Outlook 2025 attributes much of this resilience to capital deepening in AI computing, cloud infrastructure, and edge semiconductors, which together account for nearly half of global tech capex. Even after a strong multi-year run, IDC expects global AI spending to reach $325 billion in 2025, up 35 % from 2024—providing a long-term tailwind for semiconductor, software, and cloud earnings.

Valuation Support and Investor Confidence

High valuations have not deterred investors. MacroMicro data show the tech sector’s forward P/E ratio at 29.8×, versus 22.6× for the S&P 500 overall—a premium roughly in line with its five-year average. JPMorgan’s TMT: Digging Into the Big Tech Rally report notes that despite elevated multiples, free-cash-flow yields near 3 % and balance-sheet cash holdings exceeding $600 billion among the 10 largest tech firms underpin market confidence. With the Federal Reserve signaling a gradual easing bias, investors view large-cap tech as both a growth play and a defensive haven—a rare combination in today’s macro landscape.

Why Other Sectors Lag

Outside tech, fundamentals look less inspiring. Industrials and materials have seen negative earnings revisions amid slowing global demand; consumer discretionary stocks face margin compression; and utilities have underperformed as yields stay elevated. Meanwhile, cyclical sectors remain vulnerable to sluggish capex and sticky input costs. Against that backdrop, technology’s high margins, strong cash generation, and secular growth narrative make it the only corner of the market where earnings visibility is improving rather than deteriorating.

The Risks Ahead

Still, the concentration risk is clear. Technology now represents roughly 32 % of the S&P 500’s market cap, and the broader “AI complex”—including semiconductors, software, and cloud—accounts for nearly 40 %. A reversal in rate expectations or any disappointment in AI monetization could quickly unwind crowded positions. Goldman Sachs’ prime-brokerage data show hedge-fund exposure to mega-cap tech in the 97th percentile of the past decade. History suggests that such crowding can amplify drawdowns when sentiment shifts. But for now, investors appear content to keep betting that innovation will keep paying the bills.

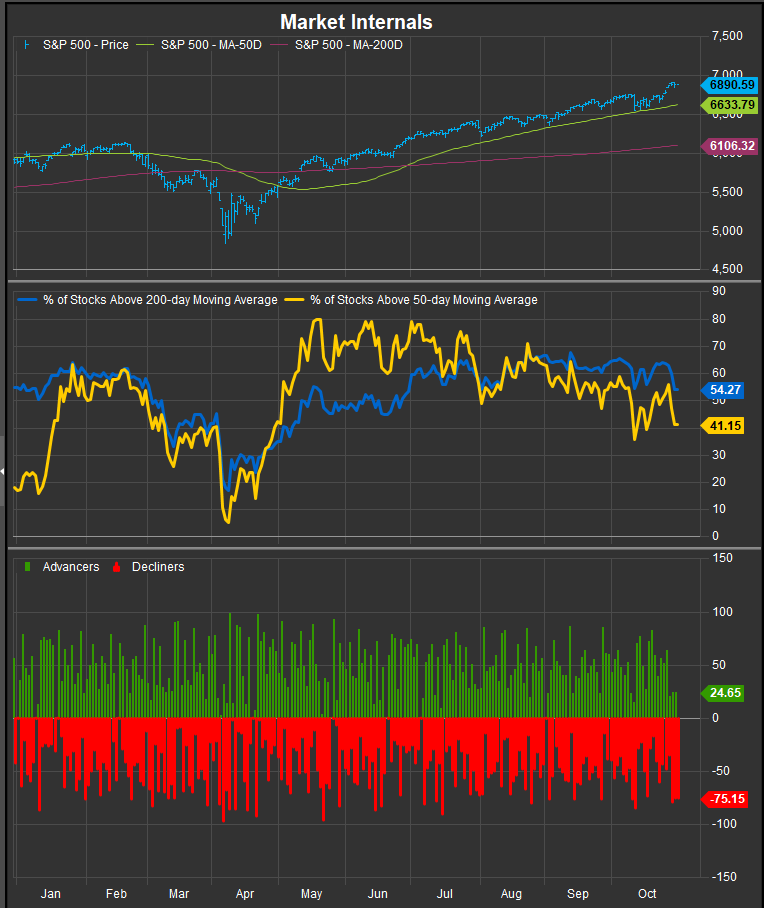

S&P 500 Internal Strength Measures

Rates are Pivotal to Complimentary Positioning

While it is clear that there is widespread speculative enthusiasm for Technology/AI exposures and crowding is a risk, there is also the fact that speculative excess offers an opportunity to make a lot of money in the stock market. While the macro picture remains favorable (low rates, tame inflation), we recommend maintaining at least a market weight position in Technology shares. We believe the direction of interest rates (chart below) is an important “tell” for anticipating rotation. Structural risks to the AI trade fall into two broad buckets, inflation risk and recession risk. Given the position of the 10yr yield we think 4.2%-4.4% is a key zone of transition. Above 4.4% there’s less congestion and rates would likely begin to re-exert pressure on the consumer and the credit cycle.

Conclusion

We want to use the direction of interest rates as guide for how we position around Technology in our portfolio. If rates stay contained below 4.2% we would hedge a potential tech correction with lower vol. sector positions (XLV, XLU, XLP) while if rates moved higher we’d want to move into sectors that are potential inflation beneficiaries (XLI, XLF, XLB, XLE).

Sources

- S&P Dow Jones Indices. (2025, October). S&P 500 Sector and Industry Performance Summary, Q3 2025.

https://www.spglobal.com/spdji - Morningstar. (2025, September). U.S. Fund Flows Dashboard – Sector Equity Funds.

https://www.morningstar.com/business/insights/blog/funds/us-fund-flows - State Street Global Advisors. (2025, Q3). SPDR Sector and Industry Dashboard.

https://www.ssga.com - BlackRock /iShares. (2025, Q3). Flow & Tell: ETF Flow Trends.

https://www.ishares.com/us/insights/flow-and-tell-q3-2025 - FactSet Research Systems. (2025, October). Earnings Insight: S&P 500 Q3 2025 Scorecard.

https://insight.factset.com - McKinsey & Company. (2025). Technology Trends Outlook 2025: AI, Semiconductors, and Cloud.

https://www.mckinsey.com/business-functions/mckinsey-digital - International Data Corporation (IDC). (2025). Worldwide Artificial Intelligence Spending Guide 2025.

https://www.idc.com - MacroMicro. (2025). S&P 500 Information Technology Forward P/E Ratio Tracker.

https://en.macromicro.me/series/20517/s5inft-forward-pe-ratio - J.P. Morgan Asset Management. (2025). TMT Sector: Digging Into the Big Tech Rally.

https://www.jpmorgan.com/wealth-management/insights - Goldman Sachs Global Investment Research. (2025). U.S. Equity Strategy: Tech Premiums and Growth Multiples.

https://www.goldmansachs.com - Visual Capitalist. (2025). S&P 500 Sector Returns 2025 YTD Chart.

https://www.visualcapitalist.com - UBS Global Wealth Management. (2025). Global Tech Earnings and Macro Update.

https://www.ubs.com - EisnerAmper. (2025, June). Private Equity Investment in Technology Trends.

https://www.eisneramper.com - Semiconductor Industry Association (SIA). (2025). Global Semiconductor Sales Report 2025.

https://www.semiconductors.org - Deloitte Insights. (2025). Tech Industry Outlook 2025.

https://www.deloitte.com/insights

Charts and additional data sourced from FactSet Research Systems Inc.