November 28, 2025

Elev8 Model Input Scores: December 2025

The table below shows the Elev8 model’s scores for December. Near-term rotation away from Technology Sector shares was the story of November, but we are expecting some accumulation into year end as the cycle’s most important stocks like NVDA and PLTR sit at near-term oversold levels. The S&P 500 has bounced off its own oversold condition to close November on expectations that the Fed will continue easing at its December meeting. US Treasury Yields have fallen accordingly with the 10yr testing below 4% to close November. Falling rates historically favor low vol. sectors and Growth over Value styles. However, we’ve also seen commodities prices firm and we’re taking a long position in structurally oversold Energy and Materials Sector shares as well in December. In the simplest terms, the question for equity investors is whether weakness in the AI trade will continue to be seen as a buying opportunity. The Value style has lagged considerably since the beginning of the current cycle in early 2023.

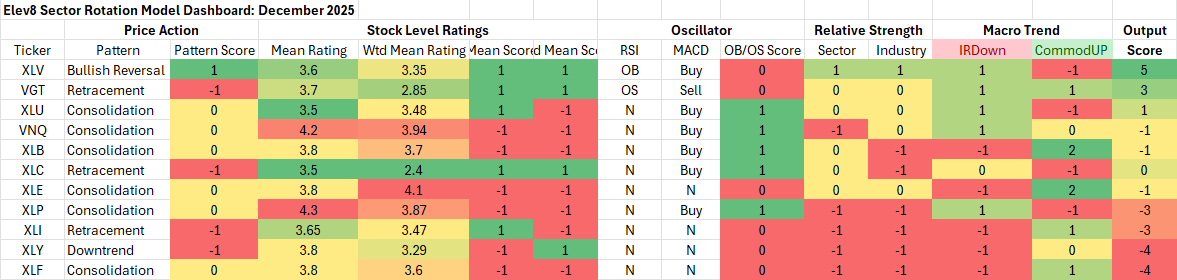

Key: Pattern = L/T (1yr+) Price Pattern of the Sector ETF, Mean Rating = simple average of 1-6 ratings (buyàsell) of all stocks within the sector, WTD Mean Rating = Cap Weighted Sector Constituent rating, OB = Overbought, OS = Oversold, N=Neutral

Model Input Commentary

Our trend following process still likes the Technology Sector despite retracement in the near-term. However, the Healthcare Sector has shown significant technical improvement in the near-term at the stock and industry level. This has been supported by falling interest rates at the macro level, but we’ve noted in past reports that Biotech, Life Sciences and Pharma stocks have seen increased buying since the summer. Falling interest rates have historically favored low vol. exposures over the past 30 years so we’ve added more low vol. exposure to our barbell strategy in December while going into the current month lighter in economically sensitive cyclical names. We think stubbornly high prices over the longer-term are likely to pressure Discretionary stocks and the housing market is likely to stay chilled into 2026 muting banking prospects as well.

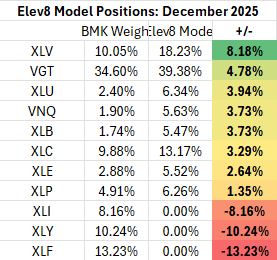

Elev8 Sector Rotation Model Portfolio: December Positioning vs. Benchmark Simulated S&P 500 (data as of 11/28)

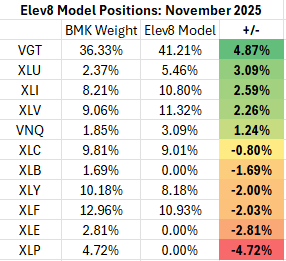

Previous Positioning as of last Rebalance: October 30, 2025

For December we’re “bar-belling” our Tech exposure with increase low vol. hedges. We’ve funded that by taking Discretionary, Financial and Industrial allocations to zero weights this month. Rising commodities prices have us overweight Energy and Materials sectors while economic concerns have us negative on pro-cyclical sectors. We think increased liquidity dynamics from lower interest rates in the near-term are likely to benefit the Growth trade rather than continuing the Growth to Value rotation we saw in November. We think the weakest link in the current setup is the mass market consumer. With yields on the 10yr and 2yr treasury moving lower, capex. financing costs are likely to remain lower, and buybacks should be a potential tailwind.

Conclusion

The AI trade cracked in November, but we think rumors of its demise are greatly exaggerated. When we evaluate the technical and macro conditions through our Elev8 model we see the Consumer Discretionary sector as facing the most current headwinds and low vol. stocks as a solid setup with some concerns over economic prospects and falling rates as a backdrop. We think a supportive Fed is likely to benefit Mega Cap. Growth stocks as much as any cyclical exposure and we think continued cost pressures will limit the appeal of a wholesale rotation from Growth to Value as the latter typically outperforms when economic growth and earnings are abundant and rates are moving higher.

About Elev8

We introduced the Elev8 Sector Rotation Model in December of 2024. Here’s a look under the hood at the inputs we use to score the 11 GICS Sectors for April and our resulting positions. The model includes up to 14 indicators that range from:

- Stock Level Technical Characteristics

- Macro-overlays:

- equity trend (S&P 500)

- interest rate trend (10yr US Treasury Yield)

- commodities trend (Bloomberg Commodities Index)

- USD trend (vs. EUR & Broad Currency Indices)

- Relative performance vs. the benchmark S&P 500

- Overbought/Oversold oscillator studies

We use the largest passive sector-based ETF by AUM ($) for each sector as our proxy for Elev8 sector positions. We select 8 out of 11 Sectors each month and have no exposure to the 3 with the lowest scores in our model.

Data from Factset Research Systems Inc.