February 26, 2026

S&P futures are slightly lower after Wednesday’s rally, which marked the Nasdaq’s first back-to-back 1%+ gains since mid-December. Tech led again, with strength in Mag 7, software, and semis/memory. Banks drove a sharp rebound in financials, while other cyclicals and defensives lagged.

Overnight, Asia was mostly higher with South Korea up over 3.5% again. Europe is +0.2%. Treasuries and the dollar are little changed. Gold -0.5%, silver -4.3%, Bitcoin -0.7% (after a 7.5% surge Wednesday), and WTI crude -1.3%.

Tech Earnings Highlights

Earnings — particularly in tech — dominate the narrative.

- NVIDIA (NVDA) delivered another major beat and raise (revenue +~$2B vs consensus; guidance +~$6B; 75% GM maintained), but the result has not meaningfully lifted broader risk sentiment.

- Salesforce (CRM) underwhelmed on core performance despite announcing a new $50B buyback.

- Software stabilization remains the broader theme following pushback against the more dire AI-disruption scenarios outlined earlier in the week.

Macro is quiet ahead of next week’s ISM data, which will be closely watched after January’s upside surprise helped fuel cyclical outperformance that has since come under scrutiny amid AI-related disinflation concerns. Geopolitics remains in focus with U.S.–Iran talks today and ongoing speculation about a limited U.S. strike.

Economic Data

- Initial Claims: Street looking for 215K vs 206K prior.

- Fed Vice Chair Bowman testifies before Senate Banking Committee.

- Treasury auctions $44B of 7-year notes (after soft 5-year auction Wednesday).

- Friday: PPI (+0.3% m/m expected headline and core) and construction spending.

Next week: ISM Manufacturing (Mon), ISM Services & ADP (Wed), Retail Sales & NFP (Fri).

Corporate Highlights

Tech:

- Snowflake (SNOW) weaker despite +27% product revenue growth guide (~2pp ahead), valuation in focus.

- Synopsys (SNPS) down despite Q1 beat; muted IP growth and China headwinds noted.

- Pure Storage (PSTG) beat and guided above; hyperscaler shipments a positive.

- Zoom Video Communications (ZM) Q4 ahead but FCF margin guide scrutinized.

- Trade Desk (TTD) down sharply on Q1 revenue guide ~2% below expectations.

- Nutanix (NTNX) up on strategic partnership with Advanced Micro Devices (AMD).

- Fair Isaac Corporation (FICO) announced $1.5B buyback.

Other Sectors:

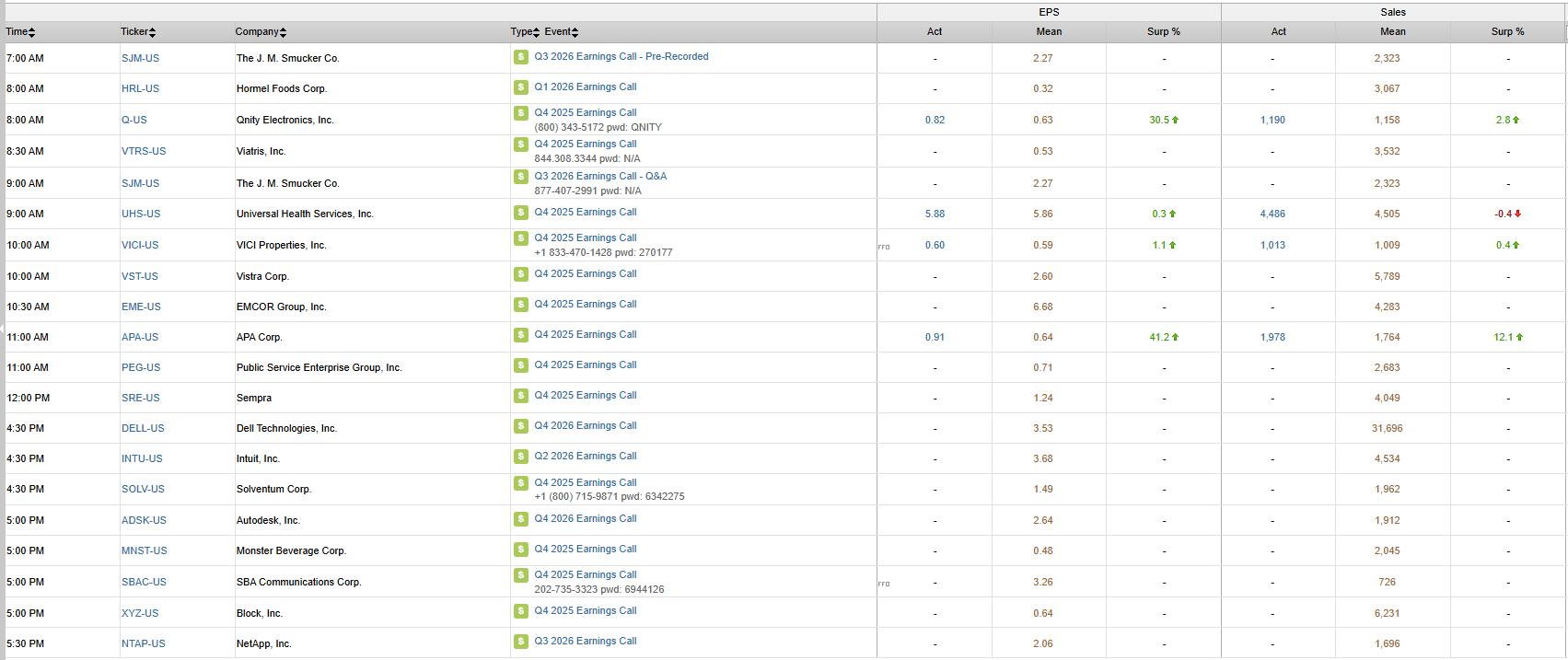

- Universal Health Services (UHS) weaker on softer acute volumes.

- Urban Outfitters (URBN) beat on stronger gross margins.

- Marriott Vacations Worldwide (VAC) higher on margin-driven EBITDA beat and improved 2026 guide.

- FS KKR Capital (FSK) down on NII miss, NAV erosion, and credit deterioration.

U.S. equities extended their rebound Wednesday (Dow +0.63% | S&P 500 +0.81% | Nasdaq +1.26% | Russell 2000 +0.41%), finishing just off session highs with leadership again concentrated in large-cap tech. Beneath the surface, dispersion remained elevated as cap-weighted indexes outpaced equal-weight benchmarks by roughly 75 bp.

Treasuries were slightly weaker with yields up 1–2 bp across the curve (10-year at 4.05%). The Treasury’s $70B 5-year auction saw the largest tail (0.7 bp) and weakest bid-to-cover since last July. The dollar index slipped 0.2%. Gold rose 1%, silver jumped 4% (back above $90), Bitcoin futures surged 7.4%, and WTI crude fell 0.3% amid a large crude inventory build and discussion of a possible OPEC+ production increase.

There was no major economic data. Fed commentary remained consistent with a “wait-and-see” posture. Kansas City Fed President Schmid said more progress is needed on inflation, while St. Louis Fed’s Musalem reaffirmed commitment to the dual mandate under potential new leadership. USTR Greer reiterated the White House intends to formalize a 15% tariff level where appropriate in coming days.

With over 90% of the S&P 500 having reported, Q4 earnings growth is tracking closer to +14% y/y.

Sector Highlights

Leadership rotated firmly back to Financials (+1.68%) and Technology (+1.79%), with Communication Services (+0.97%) also outperforming. Industrials (-0.79%), Real Estate (-0.70%), Consumer Staples (-0.58%), Materials (-0.43%), Energy (-0.42%), and Healthcare (-0.02%) lagged, while Utilities (+0.36%) and Consumer Discretionary (+0.48%) posted modest gains. The session reflected continued enthusiasm for semis and software stabilization, even as many traditional cyclicals (homebuilders, machinery, building materials) underperformed.

Information Technology

- NVIDIA (NVDA) – Higher into earnings amid expectations for another beat-and-raise.

- Microsoft (MSFT) – Best-performing mega-cap.

- Workday (WDAY) +2.3% despite lighter FY27 growth guidance; margin headwinds tied to AI investments and longer sales cycles.

- Oracle (ORCL) +1.2% on upgrade citing resilience to AI disruption.

- IBM (IBM) +3.6% on upgrade.

- First Solar (FSLR) -13.6% on weaker 2026 guidance and Southeast Asia headwinds.

- GoDaddy (GDDY) -14.3% on weaker FY26 revenue guide.

- Clear Secure (YOU) +39% on strong Q4 beat and capital return.

- Circle Internet Financial (CRCL) +35.5% on stablecoin adoption momentum.

Financials

- Nasdaq (NDAQ) +3.6% after raising medium-term revenue outlook.

- Banks, IBs, credit cards, payments, and PE broadly firmer as recent disinflationary angst around AI disruption eased.

Communication Services

- Netflix (NFLX) +6% after Warner Bros. Discovery indicated a rival PSKY offer could be superior, though the existing merger agreement remains in place.

- Fox Corporation (FOX) -3.6% on downgrade citing NFL rights renewal risk.

Consumer Discretionary

- TJX Companies (TJX) – Helped by upbeat early 2026 commentary and capital return.

- Lowe’s (LOW) -5.6% on weaker FY26 margin/EPS guide despite comp beat.

- Cava Group (CAVA) +26.4% on strong Q4 results and 2026 outlook.

- MercadoLibre (MELI) -8.1% on margin miss tied to investment spend.

- Oddity Tech (ODD) -49.2% on sharply negative Q1 revenue guide tied to ad algorithm disruption.

Healthcare

- Jazz Pharmaceuticals (JAZZ) +13.2% on strong Q4 and solid 2026 outlook.

- United Therapeutics (UTHR) +13% as Q4 overhang cleared.

- Tempus AI (TEM) -7.3% on weaker EBITDA guide.

Materials & Energy

- Albemarle (ALB) +4.8% as Zimbabwe banned lithium exports.

- Mosaic (MOS) -5.3% on soft phosphate volumes.

- Talos Energy (TALO) -13.7% on production miss and softer capex outlook.

- O-I Glass (OI) -13.2% on volume declines and weak guidance.

Industrials

- Axon Enterprise (AXON) +17.6% on strong Q4, robust 29% CAGR outlook through FY28, and AI traction.

- Driven Brands (DRVN) -30.2% after disclosing accounting errors and delaying financials.

Eco Data Releases | Thursday February 26th, 2026

S&P 500 Constituent Earnings Announcements | Thursday February 26th, 2026

Data sourced from FactSet Research Systems Inc.