April 23, 2026

S&P futures are down 0.5% Thursday morning after another record close for the S&P 500 and Nasdaq on Wednesday. Recent leadership has remained concentrated in Mag 7, semis, software, and higher-beta trading themes, with the SOX extending its winning streak to 16 sessions and software up for an eighth straight day. Cross-asset tone is weaker this morning: Treasury yields are up 2 bp, the dollar is modestly firmer, gold and silver are lower, Bitcoin is down, and WTI crude is up 2.5%.

The market appears to be reassessing some of the recent complacency around the Iran conflict. Oil has now risen for a fourth straight session as tensions around the Strait of Hormuz continue to build, raising concern that equities may be underpricing the risk of a more persistent energy and growth shock. Outside geopolitics, the broader backdrop is still supported by strong Q1 earnings metrics, though stock-level reactions remain mixed. Other areas in focus include slowing mechanical buying support from systematic strategies, a more bullish sentiment backdrop, and renewed scrutiny on private credit after reports of creditor pressure in software and increased regulatory attention on the industry.

Today’s macro focus is on initial claims and April flash PMIs. Manufacturing PMI is expected at 52.5 and services PMI at 50.1, with investors also watching for any renewed evidence of pricing pressure after firmer regional manufacturing surveys. Friday brings final University of Michigan sentiment and inflation expectations.

Company Highlights

- TSLA: Posted a strong beat with margins a standout and AI/AV timelines largely reiterated, though enthusiasm was tempered by a large capex guidance increase

- IBM: Pressured by a lack of upside in Software growth and unchanged guidance

- TXN: Beat and raised, with industrial and data center demand standing out

- NOW: Under pressure on Middle East-related deal pushouts and largely unchanged organic growth guidance

- LRCX: Raised its 2026 wafer fab equipment outlook

- CSX: Beat on stronger margins and raised guidance

- URI: Moved higher after beating and raising on strong rental revenue and margins

- LUV: Results and guidance disappointed

- MEDP: Weakened on softer book-to-bill

- MOH: Beat with support from improved Medicaid cost trends

- LULU: Lower after hiring former Nike executive Heidi O’Neill

U.S. equities moved higher on Wednesday, with the S&P 500 gaining 1.05%, the Nasdaq rising 1.64%, the Dow adding 0.69%, and the Russell 2000 advancing 0.74%, as both the S&P and Nasdaq closed at fresh record highs. Treasury yields were modestly lower, helped by a well-received $13B 20-year Treasury auction, while gold rose 0.7%, silver gained 1.9%, Bitcoin futures rallied 5.3%, and WTI crude climbed 3.7%, finishing near the highs of the day.

The key macro support came from the ceasefire extension, which allowed equities to look through geopolitical risk and continue the recent grind higher. That said, the broader Middle East backdrop remains far from fully resolved. Persistent constraints on energy and product flows continue to raise questions about whether markets are underestimating the physical and structural disruption risks to growth, particularly as oil prices continue to push higher.

Outside of geopolitics, the dominant macro and market themes remained consistent with recent sessions. Investors continued to lean into the AI trade, with semiconductors posting a record 16th straight advance and another round of upbeat AI-related headlines reinforcing the capex and infrastructure narrative. Earnings remained an important bullish talking point, with first-quarter results continuing to come in better than expected. At the same time, there was growing scrutiny around narrow breadth, softer guidance trends, and a weakening earnings revision ratio. Flow dynamics were less central than in prior weeks, though ongoing buyback support, fear-of-missing-out behavior, and month-end positioning remained part of the broader backdrop.

With no economic data released on Wednesday, attention now shifts to Thursday’s jobless claims and flash PMIs, followed by Friday’s final University of Michigan consumer sentiment and inflation expectations.

Sector Performance

Sector performance reflected a growth-led advance, with leadership again concentrated in technology and a handful of cyclical beneficiaries. Technology (+2.31%), Communication Services (+1.41%), and Energy (+1.14%) were the clear outperformers, benefiting from the return of AI momentum and higher oil prices. By contrast, the weakest groups were Real Estate (-0.69%), Industrials (-0.20%), Financials (-0.17%), and Utilities (-0.16%), while Health Care, Materials, Consumer Discretionary, and Consumer Staples posted only modest gains. Breadth was positive overall, but the equal-weight S&P notably lagged the cap-weighted index by roughly 110 bp, reinforcing the view that index gains remained driven by narrow large-cap leadership rather than broad participation.

Company Highlights (GICS Organized)

Information Technology

- ADBE +3.5%: Announced a new $25B stock repurchase program

- VICR +9.5%: Q1 earnings and revenue beat, with management highlighting ongoing capacity constraints despite planned expansion

- CALX -14.0%: Better Q1 results were overshadowed by weaker Q2 gross margin and EPS guidance tied to higher memory prices

- VRT -2.3%: Beat on revenue and operating income and raised elements of FY26 guidance, though expectations had become very elevated

- TEL -9.1%: Mixed quarterly results, with revenue and EBIT light and margin performance a key area of concern

Consumer Discretionary

- UAL -5.6%: Slight beat on Q1 revenue and EPS, but lowered FY26 EPS guidance amid higher fuel costs despite strong corporate and premium demand

- BBY -4.6%: Announced a CEO transition, with Jason Bonfig set to succeed Corie Barry on 31-Oct

- TMHC +4.9%: Q1 EPS and EBITDA beat, with margins and management commentary on orders seen as constructive

Consumer Staples

- PM +7.0%: Q1 EPS, revenue, and operating income beat, with analysts highlighting resilience in shipment trends and continued IQOS momentum

- SON -16.2%: Guided FY EPS to the low end of its range, citing weather disruptions, a fire, weaker demand, and inflation-related cost pressure

Health Care

- ISRG +7.2%: Q1 earnings, revenue, and margins beat; raised procedure growth and gross margin guidance

- BSX +9.0%: Q1 revenue and EPS beat, with stronger-than-feared results and guidance that was viewed as conservative enough to help stabilize sentiment

- HCSG +18.3%: Posted a large Q1 beat and highlighted new client wins, strong retention, and positive momentum into Q2

- INBX +37.5%: Reportedly drawing acquisition interest from MRK and Ono Pharma

- TFX +11.3%: Rose on a Reuters report that private equity firms had submitted a joint bid to take the company private

- CYH -12.6%: EBITDA missed, with softer volumes, mix pressure, and macro-sensitive consumer headwinds in focus

Financials

- BKU -1.6%: Q1 earnings missed, with weaker NII, NIM, fee income, and below-consensus loan and deposit growth

- PRU -1.6%: Downgraded at Jefferies on uncertainty tied to the extended sales suspension at Prudential of Japan

- CB -1.2%: Q1 core operating EPS and net premiums written beat, though management flagged softening insurance market conditions

Industrials

- GEV +13.8%: Q1 earnings and revenue beat, with backlog growth and data center electrification demand standing out; raised full-year guidance

- BA +5.5%: EPS and free cash flow beat, backlog reached a record, and management pointed to improving certification timing and better Defense performance

- MANH +5.9%: Q1 results beat and management raised its 2026 outlook, with bookings, renewals, and customer momentum all highlighted positively

Eco Data Releases | Thursday April 23rd, 2026

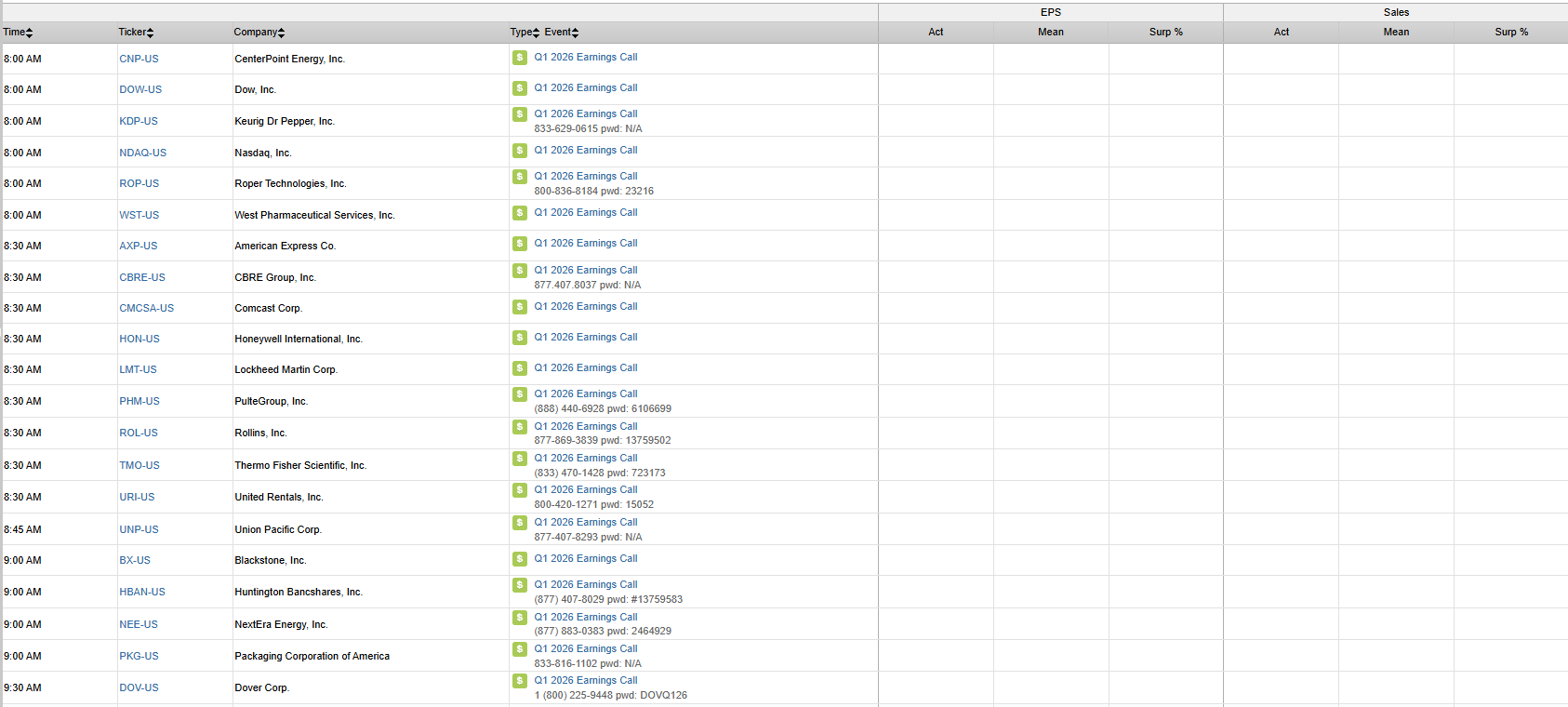

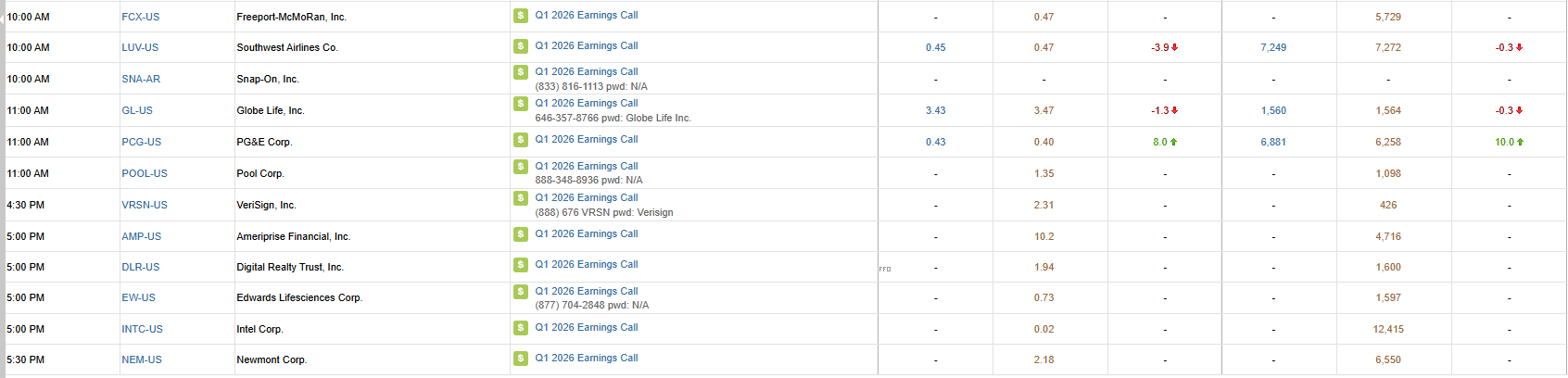

S&P 500 Constituent Earnings Announcements | Thursday April 23rd, 2026

Data sourced from FactSet Research Systems Inc.