S&P futures are down 0.2% Tuesday morning after a modestly positive Monday session. The market remains in wait-and-see mode ahead of a critical stretch of Mag 7 earnings on Wednesday and Thursday. Cross-asset moves are mildly risk-off: Treasury yields are up about 2 bp, the dollar is firmer, gold and silver are lower, Bitcoin is slightly down, and WTI crude is up another 3.1%.

The main macro themes are familiar but important. Investors are still balancing a solid earnings backdrop and AI enthusiasm against rising concern around higher oil, firmer yields, and geopolitical risk. In the Middle East, Trump reportedly reacted negatively to Iran’s latest proposal, while reports suggest Iran may be running short on storage capacity. At the same time, the market is increasingly shifting its AI focus away from pure capex excitement and toward ROI and spending sustainability, especially ahead of hyperscaler results. That theme got more attention overnight after reports that OpenAI has recently missed internal user and revenue targets, raising fresh questions about whether current data-center spending expectations are fully justified.

Another important overnight development was the Bank of Japan’s hawkish hold, which added to the firmer global rate backdrop. Today’s U.S. calendar includes Case-Shiller, FHFA house prices, and Conference Board consumer confidence, along with a $44B 7-year Treasury auction. The rest of the week is packed with catalysts, including durable goods, the FOMC decision, Q1 GDP, PCE inflation, jobless claims, and ISM manufacturing.

Company Highlights

- OpenAI: Reportedly missed internal targets for users and revenue, raising fresh questions about AI-spending sustainability

- DT: Starboard reportedly has taken a stake in the AI software company

- ERAS: Under pressure after a death disclosure tied to the ERAS-0015 trial

- BHP / SANM / NUE / UHS / LC / BBBY: Among the more notable post-close or early earnings gainers

- NVS / AMKR / RMBS / QGEN / NOV: Among the more notable laggards following earnings

U.S. equities finished mostly higher Monday, with the S&P 500 up 0.12%, Nasdaq up 0.20%, and Russell 2000 up 0.04%, while the Dow slipped 0.13%. Stocks ended near session highs, though gains were restrained ahead of a pivotal week featuring 180 S&P 500 earnings reports and five Mag 7 companies. Treasury yields moved modestly higher with a touch of curve steepening, the dollar eased 0.1%, gold fell 1.0%, silver declined 1.8%, and WTI crude rose 2.0%, extending last week’s sharp advance.

The broader macro tone remained relatively steady despite continued Iran-related headline noise. Weekend hopes for face-to-face talks ultimately went nowhere, but the market largely shrugged off the disappointment and continued to assume that negotiations will persist and that any resolution is more likely to be long, uneven, and diplomatic rather than a return to a hot war. That has allowed investors to keep looking through geopolitics for now, even as energy-market complacency remains a concern.

Outside geopolitics, the core market narrative remains supportive. With more than a quarter of the S&P 500 having reported, Q1 EPS growth is running near 15%, reinforcing confidence in the earnings backdrop. Other ongoing bullish pillars include surging AI compute and infrastructure demand, a still-solid economic backdrop, resilient consumer trends, and an ongoing industrial cyclical recovery. At the same time, investors remain alert to war-related input cost pressures, elevated capex requirements, and the risk that higher energy prices eventually weigh more materially on growth and margins.

Economic data was limited. The Dallas Fed manufacturing index fell to -2.3 from -0.2 and missed expectations, though production and new orders improved. Treasury supply was also in focus, with both the 2-year and 5-year auctions tailing, including an 11th straight tail in the 5-year. Attention now turns to a much busier stretch featuring consumer confidence, durable goods, Q1 GDP, March PCE, ISM manufacturing, and Wednesday’s April FOMC decision.

Sector Highlights

Sector performance reflected a modestly constructive but selective tape, with leadership concentrated in Communication Services (+0.94%), Financials (+0.65%), and Technology (+0.46%). On the downside, Consumer Staples (-1.18%), Real Estate (-0.84%), Consumer Discretionary (-0.76%), and Health Care (-0.54%) were the weakest groups, while Materials, Energy, Industrials, and Utilities also lagged. The pattern pointed to a market still favoring selective large-cap growth, financials, and AI-linked exposures, while more defensive and rate-sensitive sectors underperformed.

Information Technology

- MSFT: Announced changes to its OpenAI partnership and will no longer pay a revenue share to OpenAI after 2030; licensing will also no longer be exclusive

- QCOM: Will work with OpenAI to develop smartphone processors

- ADBE -2.5%: Downgraded to neutral at Mizuho on intensifying competition in prosumer and small business segments

- POET -47.4%: Cancelled all purchase orders received from Marvell’s Celestial AI due to confidentiality violations

- SKYT -5.2%: Received a second FTC request tied to its proposed merger with IONQ

- CRWD +1.5%: Upgraded to outperform at Mizuho on AI security opportunity and product breadth

Communication Services

- VZ +1.5%: Q1 earnings beat, free cash flow was strong, and the midpoint of full-year EPS guidance was raised, though revenue was a bit light

- META: China blocked its proposed acquisition of AI firm Manus following a security review, though Meta said it expects the issue to be resolved

- SNAP +7.1%: Upgraded to buy at Rothschild & Co Redburn on improving revenue diversity and cost control

Consumer Discretionary

- DPZ -8.8%: Q1 revenue, comps, and EPS missed, with both U.S. and international same-store sales below expectations

- PTON +2.5%: Partnering with Spotify to launch “Fitness with Spotify,” giving premium users access to Peloton classes

- JOBY +6.4%: Completed New York City’s first point-to-point electric air taxi demonstration flights

Health Care

- OGN +17.0%: To be acquired by Sun Pharmaceutical in an $11.75B transaction

- ORKA +10.7%: Reported positive Phase 2a psoriasis data for ORKA-001

- ERAS -10.9%: Disclosed patent-infringement claims from Revolution Medicines

Industrials

- FLS +5.7%: Rose on news that Starboard Value has built a significant stake and is pushing for margin improvement

- SWK +4.2%: Approved a $500M buyback

- GEV -2.5%: Downgraded to neutral at BNP Paribas on concern that growth momentum may be challenged given turbine capacity is largely contracted through 2030

Eco Data Releases | Tuesday April 28th, 2026

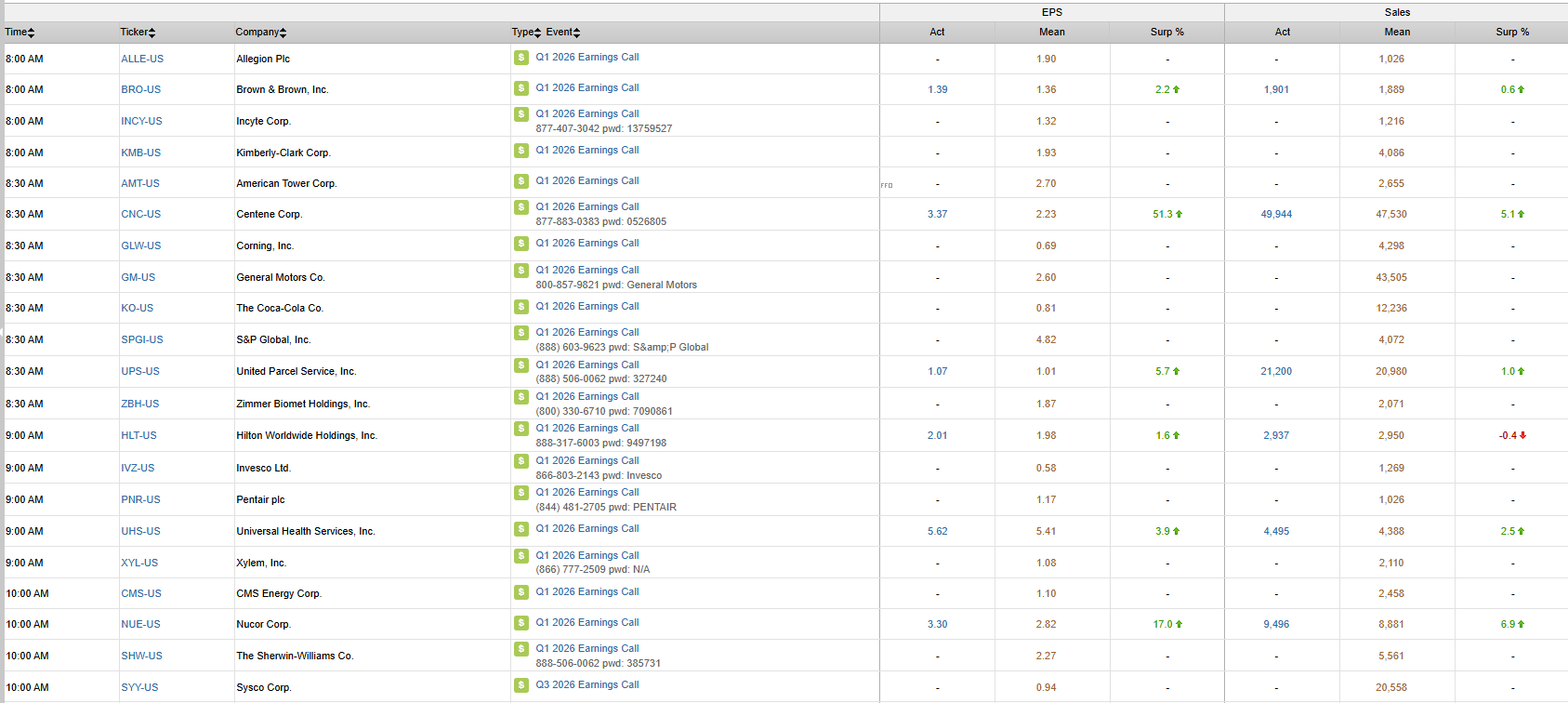

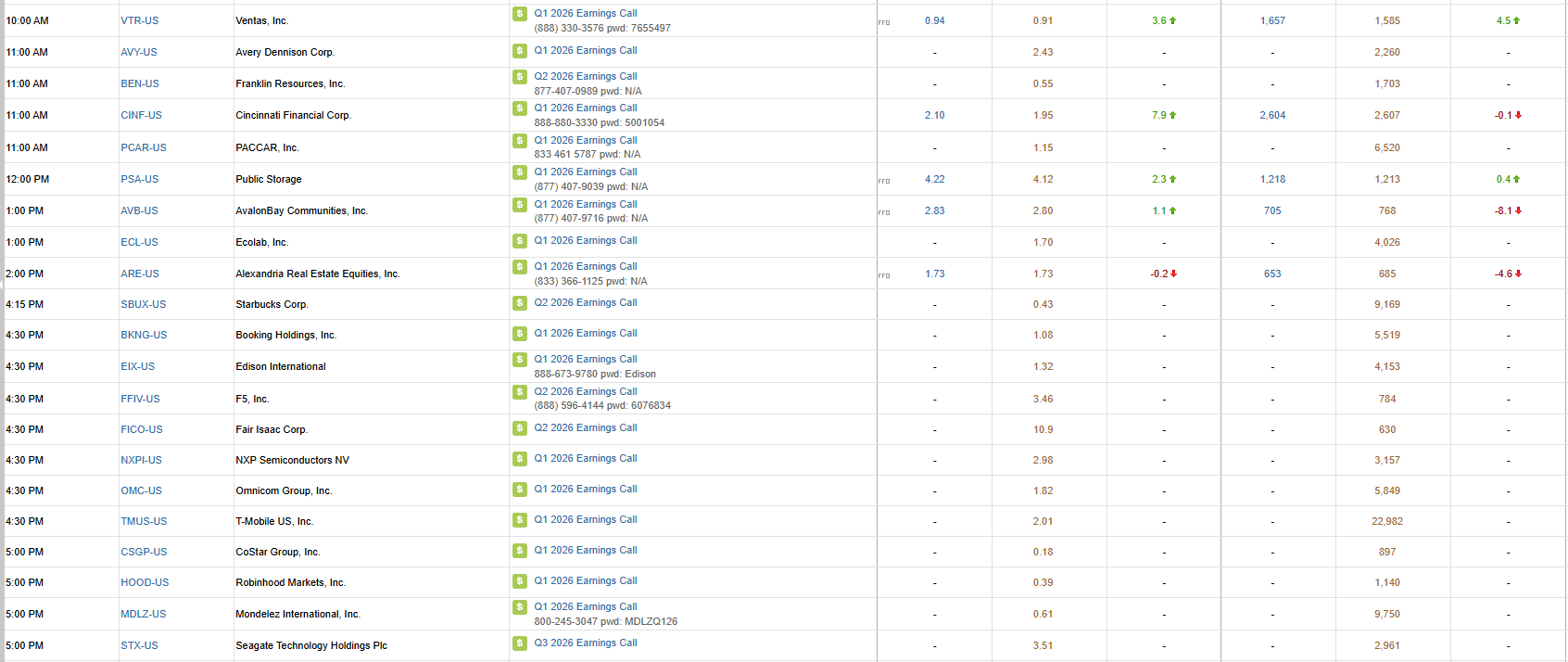

S&P 500 Constituent Earnings Announcements | Tuesday April 28th, 2026

Data sourced from FactSet Research Systems Inc.