S&P futures are up 0.1% Thursday morning after U.S. equities finished mostly lower Wednesday. The broader setup remains cautious, with Asian markets weaker overnight, Europe down roughly 0.3%, Treasuries slightly firmer after Wednesday’s selloff, the dollar off 0.1%, gold and silver rebounding, Bitcoin futures modestly higher, and WTI crude up another 1.4% after Wednesday’s 7% rally.

Markets are digesting a heavy slate of big tech earnings that broadly reinforced the AI compute-demand and capex story, though investors remain focused on ROI, monetization, sustainability, and whether the AI trade has already pulled forward too much upside. Macro overhangs also remain in place, including higher oil, upward pressure on yields, Middle East stalemate risk, monetary-policy complications, fading CTA re-risking support, and expected month-end equity selling. Today’s data calendar is busy, with Q1 GDP expected to show 2.2% growth after 0.5% in Q4, March core PCE inflation expected at +0.3% m/m and +3.2% y/y, initial claims expected to edge down to 212K from 214K, and April Chicago PMI expected to tick up to 53.0 from 52.8. Friday’s ISM manufacturing report is expected to rise to 53.1 from 52.7.

Information Technology

- GOOGL: Best of the Mag 7 prints, helped by 63% Google Cloud growth, near-doubling of Google Cloud backlog, 19% Search growth, and a large operating-income beat.

- AMZN: Standout print, supported by a fifth straight quarter of AWS acceleration, AWS margin upside, strong advertising growth, and better-than-feared Q2 operating-income guidance.

- MSFT: Lower despite better Azure growth and guidance, as another capex ramp did little to ease investor concerns around AI spending intensity.

- META: Laggard after an underwhelming Q2 revenue guide and higher FY capex outlook.

- KLAC: Latest semicap equipment name to trade lower on earnings.

- QCOM: Guided weaker on handset headwinds, though shares were supported by commentary around a data-center entry.

- TTMI / VIAV / PI: Notable earnings gainers.

Communication Services

- META: Underperformed on Q2 revenue guidance and higher capex expectations.

- GOOGL: Outperformed within large-cap internet on strong Search and Cloud results.

Consumer Discretionary

- CVNA: Higher after an EBITDA beat and upbeat outlook commentary.

- ORLY: Boosted by much stronger-than-expected 8%+ comp growth.

- F: Beat and raised guidance, with moving pieces including a larger tariff refund, Ford Blue strength, and higher raw-material costs.

- CMG: Helped by Q1 comp acceleration and improved trends in April.

- EBAY: GMV accelerated, though some commentary pointed to a high bar.

- MAT: Notable earnings gainer.

- MGM: Earnings laggard.

Consumer Staples

- SFM: Notable earnings gainer.

Financials

- AFL / ALL / IVH: Earnings laggards.

- Payments: Continued to outperform relative to broader Financials, while banks were among Wednesday’s laggards.

Real Estate

- EQIX: Takeaways and commentary were positive, but shares were hit by a headline miss.

- SBAC: Earnings laggard.

Industrials

- FLS: Core EPS missed and FY organic-sales guidance was lowered, with management citing Middle East impact.

- Machinery / multis: Among broader market laggards.

Materials

- FMC: Notable earnings gainer.

- Metals: Among Wednesday’s laggards as cyclical and input-cost concerns weighed on the group.

U.S. equities finished mostly lower Wednesday, though the major averages closed off session lows, with the Dow down 0.57%, the S&P 500 down 0.04%, the Nasdaq up 0.04%, and the Russell 2000 down 0.60%. The broader macro backdrop was dominated by a sharp repricing in oil, rates, and geopolitical risk. WTI crude surged 7.8% to $107.75/barrel amid renewed concern that the U.S.-Iran conflict could be prolonged and potentially disrupt physical crude supply. The move in oil added another inflation complication for investors, while Treasury yields moved higher across the curve: the 2-year rose 9 bp to 3.93%, the 10-year rose 6 bp to 4.41%, and the 30-year rose 5 bp to 4.98% after briefly touching 5%. The dollar index rose 0.3%, while gold, silver, and Bitcoin futures all declined. Economic data were generally firm, with March durable-goods orders up 0.8% m/m and core capital-goods orders up a much stronger 3.3%, while housing starts beat expectations and permits came in slightly light.

The April FOMC meeting was largely in line with expectations, with the Fed holding rates steady. However, the details pointed to growing internal division. Governor Miran dissented in favor of a 25 bp cut, while three other members objected to keeping the easing bias in the statement. The statement was little changed beyond acknowledging higher energy prices and continued Middle East uncertainty. Chair Powell’s press conference focused partly on his decision to remain a Fed governor after his chairmanship ends, but the market takeaway was that the Fed is facing a more complicated policy backdrop: firm economic data, renewed energy-driven inflation risk, and less consensus around the timing or need for future easing.

Sector Highlights

Sector performance reflected the crosscurrents from higher oil, higher yields, and mixed earnings. Energy was the clear leader, up 2.35%, as crude’s rally supported the group. Technology rose 0.18%, helped by strength in semiconductors, memory, networking, and AI/data-center beneficiaries. Consumer Discretionary gained 0.10% and Financials rose 0.09%, supported by selective earnings strength in restaurants, payments, and exchanges. On the downside, Utilities fell 1.23%, Materials declined 1.10%, Healthcare lost 0.69%, Real Estate fell 0.64%, Industrials declined 0.62%, Consumer Staples slipped 0.24%, and Communication Services eased 0.14%. The tape favored energy leverage, AI infrastructure, capital return, and companies with resilient demand, while rate-sensitive groups, cost-exposed cyclicals, and companies facing margin pressure lagged.

Information Technology

- STX +11.1%: Beat fiscal Q3 revenue and EPS estimates and guided Q4 well above consensus, helped by accelerating hyperscaler HDD demand tied to AI-driven data creation and data-retention needs. Gross-margin expansion was also a key positive.

- NXPI +25.5%: Reported Q1 upside and issued Q2 guidance well above consensus. Analysts highlighted improving bookings, better visibility, signs of a cyclical upturn, auto strength tied to software-defined vehicles, and emerging data-center tailwinds.

- APH +3.2%: Beat Q1 earnings and revenue expectations, with strong organic growth across most end markets, especially IT datacom. Q2 guidance also came in above the Street.

- VRNS +7.3%: Beat on revenue, billings, ARR, deferred revenue, and operating income while raising FY26 guidance. Analysts cited new-logo momentum, share gains in AI-related customer budgets, and management commentary that macro headwinds remain limited.

- TER -19.4%: Fell despite a Q1 beat, as Q2 guidance was only modestly above consensus and failed to clear a high bar after the stock’s strong YTD rally. Investors also focused on some weakness in Product Test.

- ENPH -9.1%: Declined despite Q1 EPS upside, as Q2 guidance pointed to continued near-term softness, a U.S. demand reset, and ongoing channel correction.

Communication Services

- TMUS +6.1%: Beat Q1 revenue and adjusted EBITDA expectations. Postpaid account additions of 217K topped consensus, postpaid ARPA grew 3.9%, and the company raised its 2026 postpaid account-addition outlook.

- DIS: Reportedly decided against spinning out ESPN, removing a potential structural catalyst but preserving the current media portfolio.

- Universal Music Group: Said it plans to sell half its Spotify equity stake and increase buybacks, adding a capital-return angle to the story.

Consumer Discretionary

- SBUX +8.5%: Beat fiscal Q2 expectations on comps, margins, and EPS. The key highlight was a 7.1% U.S. comp gain, more than 250 bp above consensus, while management raised FY comp guidance.

- EAT +14.5%: Rose after largely in-line fiscal Q3 revenue and EBITDA, along with a higher low end of EPS guidance. Investors focused on better traffic trends in February and March, new products, and low expectations heading into the print.

- YUM +2.2%: Beat Q1 revenue, comp, and EPS expectations, helped by strength at Taco Bell and better-than-feared Pizza Hut results. KFC’s unit-development outlook was unchanged despite Middle East conflict concerns.

- ETSY +10.1%: Reported better Q1 GMS, stronger-than-expected Q2 GMS guidance, and raised FY GMS guidance to low-single-digit growth from a prior expectation for only slight growth.

- BKNG: Posted mixed Q1 results and light Q2 guidance, with management citing temporary Middle East conflict headwinds.

- PAG +6.3%: Beat Q1 revenue and EPS expectations, helped by PTL income, solid same-store automotive trends, and optimism around Class 8 orders as a potential signal of freight-cycle improvement.

Consumer Staples

- COCO +29.7%: Beat Q1 EPS, EBITDA, and revenue expectations and raised FY26 revenue and EBITDA guidance. Management cited strong retail growth, improving private-label shipments, and pricing benefits.

- MDLZ +4.3%: Beat Q1 revenue and EPS expectations, with strength in emerging markets, signs of developed-market stabilization, broad-based volume improvement, and better execution.

- BF.B -10.3%: Fell after terminating discussions with Pernod Ricard regarding a potential combination, with the companies unable to reach mutually agreeable terms.

Energy

- Energy sector +2.35%: Led the market as WTI crude surged nearly 8% on escalating U.S.-Iran risk and concern around crude-supply disruption. The group’s outperformance was primarily macro-driven rather than company-specific.

Financials

- V +8.3%: Beat fiscal Q2 expectations, raised FY guidance, and announced a $20B buyback. Management highlighted resilient consumer spending, improving U.S. volume trends, commercial acceleration, value-added services strength, and potential benefits from agentic commerce.

- PYPL +2.6%: Rose after reports that Venmo will be separated into its own standalone unit as part of a broader reorganization into three distinct business segments.

- SOFI -15.4%: Declined despite revenue and EBITDA upside, as investors focused on weaker non-interest income, softer technology product and loan-platform fees, and rising personal-loan charge-offs.

- HOOD -13.2%: Fell after Q1 revenue missed expectations, with softer options, crypto, and equities trading activity, along with weaker funded-customer and ARPU metrics.

- FICO +3.3%: Beat fiscal Q2 earnings and revenue expectations, raised FY guidance, and highlighted strength in B2B Scores from higher mortgage origination and better pricing.

Healthcare

- HUM: Outperformed after a Q1 beat driven by medical-loss-ratio strength.

- GEHC -13.2%: Missed Q1 EPS and EBIT expectations despite better revenue and cut FY26 EPS, EBIT, and FCF margin guidance. Management cited inflationary pressure from chips, oil, freight, and logistics.

- REGN -6.2%: Fell despite a Q2 revenue and EPS beat, as investors focused on mixed franchise performance, including softer Eylea HD results, while FY26 spending guidance was unchanged.

Industrials

- GD +8.0%: Beat Q1 earnings, revenue, and operating-margin expectations across all divisions and raised FY EPS guidance. Analysts highlighted Aerospace strength from Gulfstream deliveries and Marine strength from submarine volumes and margins.

- GNRC +16.5%: Beat EPS expectations by a wide margin and raised FY guidance, helped by stronger margins, a growing data-center customer backlog, the Enercon acquisition, and C&I strength.

- ADP +8.0%: Beat fiscal Q3 revenue and earnings expectations and raised FY guidance, supported by broad-based strength in Employer Services and PEO Services.

- WERN +5.8%: Rose after an EPS beat, with margin improvement helped by better utilization, cost performance, and safety/insurance improvement, despite a revenue miss.

- IR -4.6%: Declined despite Q1 revenue and EPS upside, as organic growth, gross margin, and free cash flow missed expectations, with analysts noting that M&A remains the main growth driver.

- ODFL: Missed revenue expectations due to lower tonnage per day, though cost mitigation and pricing helped cushion the impact.

- IEX +5.8%: Beat Q1 EPS, organic growth, and revenue expectations, with record orders and raised FY26 guidance.

- LII +4.5%: Beat Q1 revenue, EBIT, and EPS expectations and reaffirmed FY guidance, supported by commercial strength, improving price/mix, and stabilizing end markets.

Materials

- OI -15.5%: Fell after Q1 revenue beat but EBITDA missed by roughly 9%, while FY guidance was lowered due to higher energy costs from the Middle East conflict and pricing pressure in Europe.

- PPG: Listed among notable decliners as the broader Materials sector lagged amid higher input-cost concerns and cyclical pressure.

- VMC: Listed among earnings gainers, though the broader Materials sector still underperformed.

Utilities

- Utilities sector -1.23%: Was the weakest group as higher Treasury yields pressured rate-sensitive, dividend-oriented equities.

Real Estate

- Real Estate sector -0.64%: Lagged as the move higher in Treasury yields weighed on rate-sensitive real estate equities and raised financing-cost concerns.

Eco Data Releases | Thursday April 30th, 2026

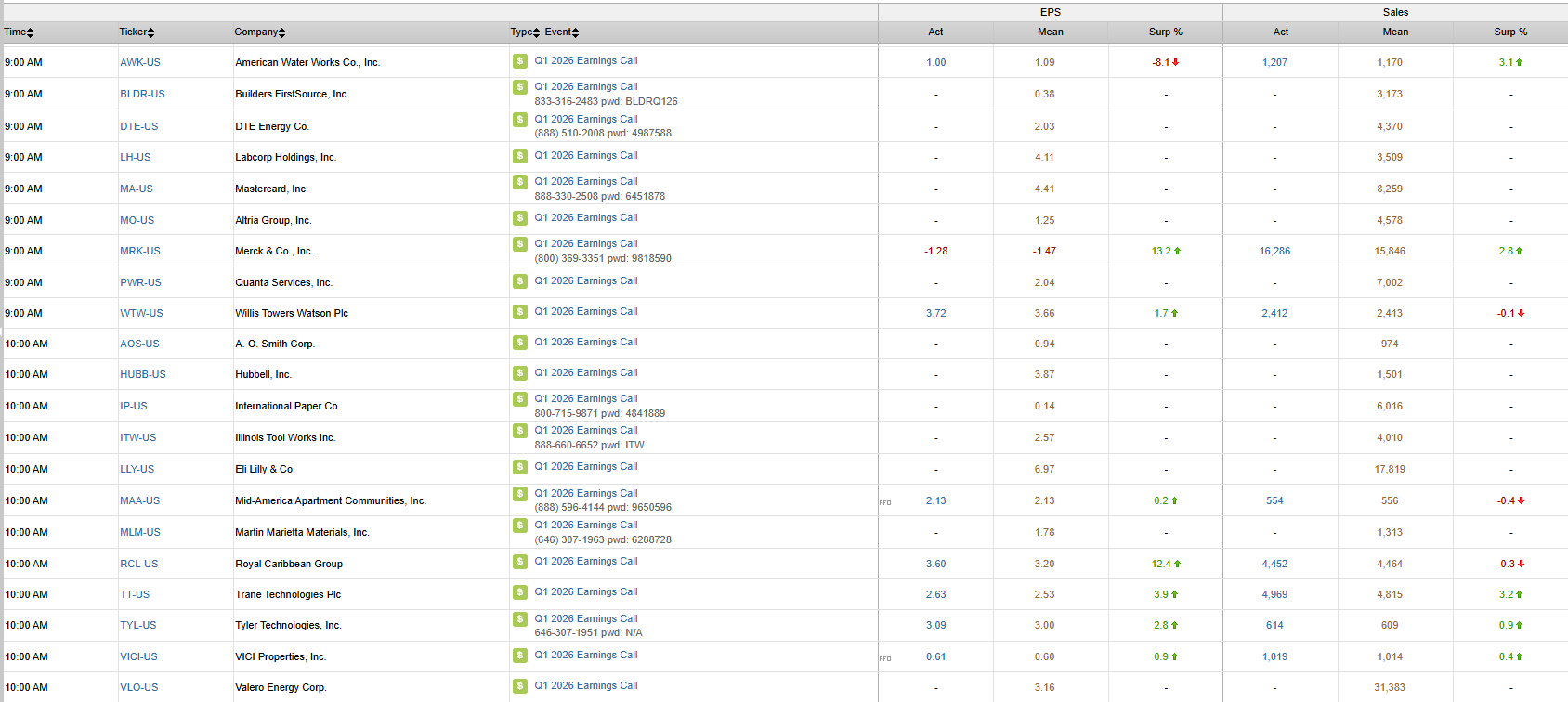

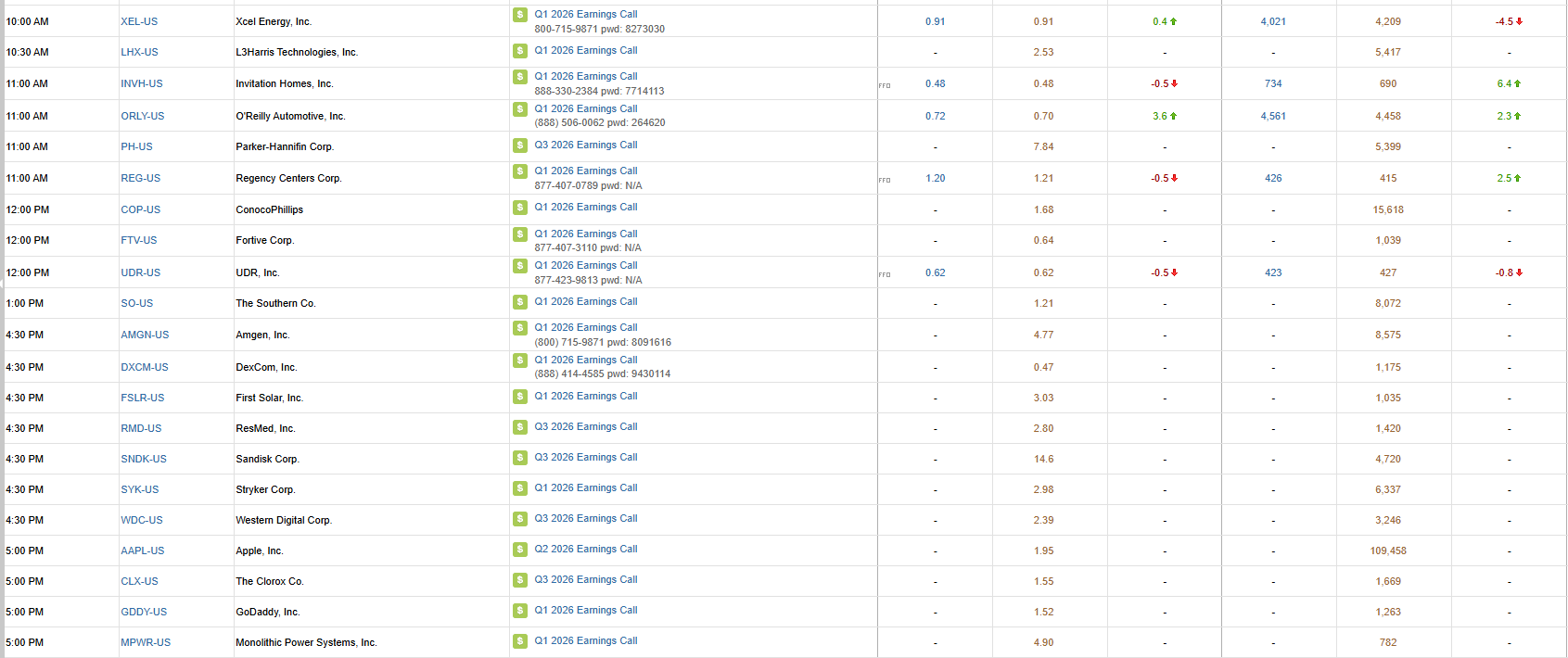

S&P 500 Constituent Earnings Announcements | Thursday April 30th, 2026

Data sourced from FactSet Research Systems Inc.