COMMENTARY:

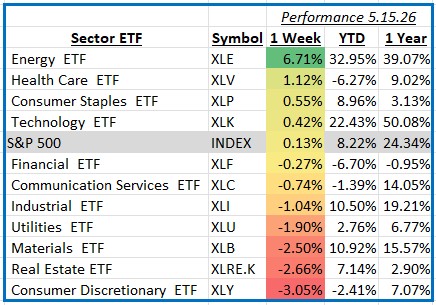

The S&P 500 finished the week essentially flat, returning just 0.13%, as a strong mid-week rally faded into Friday’s session. Markets were pulled in competing directions by several notable developments: oil prices surged amid continued disruptions to global energy supply linked to ongoing geopolitical tensions in the Middle East, while a Trump-Xi summit in China concluded without any major trade agreements, disappointing investors who had hoped for progress. On the economic data front, retail sales rose 0.5% in April — a sign of consumer resilience — though the figure came in slightly below expectations and did little to offset broader concerns about inflation and rising Treasury yields.

Energy — Top Performer (+6.7%) Energy was the clear standout sector for the week, driven by a sharp move higher in crude oil prices. Supply disruptions tied to Middle East conflict pushed oil toward and above the $100-per-barrel level, lifting sentiment broadly across the sector. Integrated energy giants Exxon Mobil and Chevron — together accounting for a substantial portion of the sector’s weight — were significant contributors to performance, benefiting from elevated commodity prices and their demonstrated ability to maintain shareholder returns even in volatile environments. Exploration and production names also gained as the supply-constrained backdrop supported price realizations.

Health Care — Strong Performer (+1.1%) Health care provided welcome stability amid the week’s choppiness, posting a solid gain as investors continued rotating into more defensive areas of the market. Eli Lilly, the sector’s largest holding, remained a key contributor, with continued enthusiasm around its GLP-1 drug franchise. Johnson & Johnson and AbbVie also lent support, benefiting from renewed interest in pharmaceutical and biotechnology names as deal activity and positive clinical news kept sentiment constructive throughout the week.

Consumer Discretionary — Laggard (−3.1%) Consumer discretionary was the week’s weakest sector, held back primarily by its two largest and most influential holdings: Amazon and Tesla. Starbucks also weighed on the group, announcing a fresh round of layoffs and restructuring charges that pressured its shares. Elevated gas prices and lingering uncertainty around consumer spending further dampened the sector’s outlook. While many of the smaller names within the group held up reasonably well, the concentrated weight of these mega-cap names overshadowed any underlying breadth.

Markets closed out a turbulent week on a cautious note, with geopolitics, inflation signals, and shifting sector dynamics all competing for investor attention. Volatility may persist in the near term as markets continue to navigate an uncertain macro backdrop.