This week’s headlines continue to frame the market around AI compute strength, AI infrastructure investment, Iran/Hormuz uncertainty, higher long-term yields, and a Fed that is less comfortable signaling rate cuts while inflation remains above target.

The latest FactSet Returns and Flow data through 5/28 show a market that is still risk-positive, but increasingly selective. This is not a uniform sector rotation. The most dynamic signals are concentrated in a handful of places: Technology leadership is broadening from semiconductors into software, Industrials and Utilities are benefiting from AI’s power and infrastructure spillover, Real Estate is seeing a tactical bid, Energy is losing some performance momentum despite continued flow support, and Consumer/Financial/Materials-sensitive themes remain inconsistent or weak.

The message for sector investors is straightforward: follow the themes where flows and performance are confirming each other, but be careful where near-term flows look more like tactical trading than durable sponsorship.

Technology: Leadership Is Still Strong, but It Is Becoming More Concentrated

The strongest sector signal remains Information Technology, but the composition of that leadership matters. Semiconductors remain the clearest AI infrastructure winner, with roughly $9.8 billion of YTD inflows, $2.4 billion over one month, and $1.0 billion over one week. Performance still supports the flow story: the semiconductor theme was up roughly 20% over one month and nearly 7% over one week.

The more important shift is that software is now confirming. Software ETFs have attracted roughly $6.9 billion YTD, $2.3 billion over one month, and more than $500 million over one week, with one-month performance around 15%. That tells us investors are not only buying chips. They are increasingly buying the enterprise software, cybersecurity, cloud and workflow layers where AI adoption can translate into revenue growth, operating leverage and productivity gains.

This week’s headlines support that evolution. Nvidia’s results reinforced the AI compute-demand narrative, while Anthropic, OpenAI, AMD, Google and SpaceX-related headlines point to continued capital formation around AI infrastructure and AI scale.

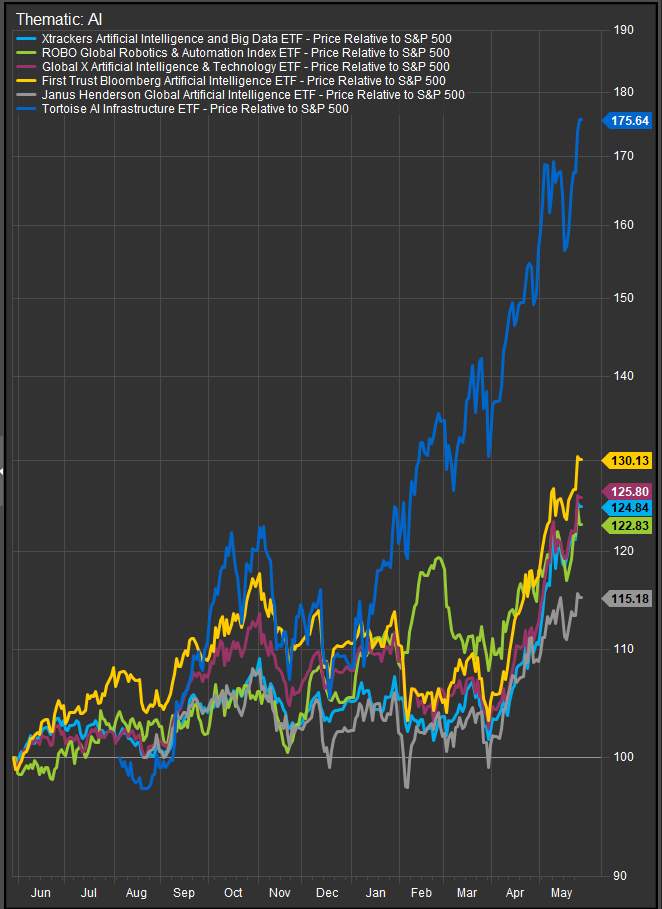

The Tortoise AI Infrastructure Fund (TCAI) is a good illustration of the enthusiasm around AI datacenter and power generation buildouts with many long-term partnerships announced recently.

Sector implication: Technology remains an overweight, but the preferred exposure is AI infrastructure plus monetizable software. Semiconductors, semiconductor equipment, networking, cybersecurity, cloud infrastructure and enterprise software look better supported than broad speculative technology. The risk is not that AI demand has disappeared. The risk is crowding, especially where investors are treating every AI-linked stock as the same trade.

Industrials and Utilities: AI Is Becoming a Power-and-Infrastructure Trade

The most constructive change outside Technology is the continued flow into themes that map to Industrials and selective Utilities. Electrification has attracted roughly $5.1 billion YTD and $1.4 billion over one month. Infrastructure has attracted roughly $3.2 billion YTD and about $750 million over one month, even though recent performance has been modest. Robotics & AI remains positive across YTD, one-month and one-week windows.

Clean Energy is also showing a near-term improvement: only modest YTD inflows, but roughly $414 million over one month, with strong recent performance. Uranium/nuclear-related exposure also remains supported, helped by the market’s search for reliable power sources tied to AI load growth.

That is the flow version of the AI infrastructure story. AI needs chips, but it also needs power, cooling, grid capacity, electrical equipment, substations, backup generation, data-center construction and industrial automation. This week’s headlines also noted that energy and infrastructure announcements boosted companies tied to AI power and data-center demand.

Sector implication: Industrials remain one of the best-positioned sectors, but the trade is not generic cyclicality. The dynamic areas are electrical equipment, grid infrastructure, automation, engineering and construction, data-center suppliers, cooling, power systems and defense-adjacent technology. Utilities can participate, but selectively. The opportunity is in power scarcity and data-center load growth, not in generic bond-proxy utility exposure, especially while long yields remain under pressure.

Real Estate: A Tactical Reversal, Not Yet a Strategic Turn

One of the more notable changes in the thematic data is the rebound in REIT flows. REIT ETFs have attracted roughly $1.2 billion YTD, but nearly all of that has arrived over the latest one-month window. One-week inflows were also strong, close to $500 million.

That looks like a tactical rate-stabilization trade. Investors appear willing to test rate-sensitive exposure after a period of underperformance. But this is not yet a clean strategic overweight. This week’s headlines highlighted continued pressure on long bonds, with concerns tied to inflation, fiscal deficits, geopolitics and a more hawkish policy mix.

Sector implication: Real Estate is improving tactically, but the bar for a durable sector rotation remains high. Traditional office, retail and highly levered REITs still face refinancing and cap-rate pressure. The better opportunity remains data-center real estate, infrastructure-linked REITs and power-adjacent assets where AI demand can offset some of the rate headwind.

Energy: Flows Are Holding, but Performance Is Cooling

Energy is still useful, but the signal has become more tactical. Legacy Energy ETFs have roughly $1.6 billion of YTD inflows and remain positive over one month and one week. MLPs also retain positive YTD and one-month inflows. But performance has cooled: Legacy Energy was down roughly 4% over one month and 6% over one week, while MLPs also weakened over the latest week.

That divergence matters. Investors still want Energy as an inflation and geopolitical hedge, but price action is becoming more sensitive to Iran/Hormuz headlines. The latest headlines show why: there has been some diplomatic progress, but uranium demands, tight inventories and concerns that Middle East flows may not normalize quickly keep the risk premium alive.

Sector implication: Energy remains a tactical overweight, not an unconditional one. Integrated oil, E&P, oil services, LNG, midstream and MLPs can still hedge inflation and supply disruption, but investors should be prepared for volatility if peace-deal headlines reduce the crude-risk premium.

Consumer Discretionary: Short-Term Bounces Do Not Yet Change the Sector View

The thematic data show some near-term improvement in Housing & Autos and Travel, but the signal is not durable enough to justify a broad Consumer Discretionary upgrade. Housing & Autos had positive one-week flows, but one-month performance remains negative. Travel saw positive near-term flows and strong short-term performance, but the macro backdrop remains fragile.

This week’s headlines captured the bifurcation: Visa, Mastercard, TJX, Ross Stores and Home Depot supported the consumer-resilience narrative, while Walmart, Target and Chewy highlighted pressure from higher fuel costs, softening sentiment, fading tax-refund support and a more stretched lower-end consumer.

Sector implication: Consumer Discretionary remains selective at best. Off-price retail, premium brands and companies using AI to improve inventory, fulfillment and personalization can work. But autos, housing-linked retail, restaurants, lower-income retail and fuel-sensitive travel remain exposed to rates, gasoline and affordability pressure.

Financials and Materials: The Flow Data Are Not Confirming Broad Leadership

Two areas stand out as weak or inconsistent: Finance/Fintech and Natural Resources.

Finance/Fintech has roughly $1.2 billion of YTD outflows and nearly $300 million of one-month outflows, even though one-week flows improved slightly. That suggests investors are not yet ready to underwrite a broad Financials leadership trade through thematic ETFs. Higher rates may help banks and insurers, but fintech, consumer finance and credit-sensitive models remain vulnerable to funding pressure and weaker consumer conditions.

Natural Resources is the clearest persistent bear trend, with roughly $5.1 billion of YTD outflows, $1.3 billion of one-month outflows, and continued one-week outflows. This is important because it shows investors are not buying the entire commodity complex. They prefer targeted Energy and infrastructure exposure over broad resources.

Sector implication: Financials should remain selective, with preference for quality banks, insurers, exchanges and asset managers rather than fintech beta. Materials should not be treated as a broad inflation hedge; the cleaner inflation exposure remains Energy, while the better structural Materials exposure is limited to specific electrification, copper and infrastructure-linked niches.

What Changed Most This Week

The biggest positive change is the broadening of AI flows from chips into software, electrification and infrastructure. That supports Technology and Industrials more than the rest of the market.

The biggest tactical change is the REIT rebound, but that looks rate-sensitive and conditional rather than durable.

The biggest caution flag is the cooling in Energy performance despite positive flows, which suggests investors still want the hedge but are becoming more sensitive to geopolitical de-escalation.

The biggest negative confirmation is the continued weakness in Natural Resources, Finance/Fintech and Low Vol, which says investors are not simply hiding in defensives or buying generic inflation exposure. They are choosing more precise exposures: AI, power, infrastructure, dividends and targeted Energy.

Bottom Line

This week’s Thematic Thursday message is not about all 11 sectors. It is about where the thematic tape is changing.

The data argue for maintaining leadership exposure in Technology, especially semiconductors and software; adding selectively to Industrials tied to electrification, grid, automation and data-center infrastructure; using Utilities only where power-demand visibility is clear; treating Real Estate as a tactical, data-center-led opportunity rather than a broad rate-sensitive rotation; and keeping Energy as a tactical inflation hedge, not a buy-at-any-price trade.

The weak or unstable flow signals argue against broad upgrades to Consumer Discretionary, Financials or Materials. There are pockets that can work, but the flows are not yet confirming durable sector leadership.

For U.S. sector investors, the playbook remains: own the sectors where thematic flows are tied to earnings visibility, capex leverage and pricing power. Avoid areas where the investment case still depends on lower rates, stronger low-end consumers or a looser liquidity backdrop.

Data note: Theme-level figures are based on FactSet Returns and Flow data through 5/28. The file labels near-term flows as “1M”; this article refers to that window as MTD/1M. Theme flows are summed across ETFs, and returns are AUM-weighted where AUM data are available.

Disclaimer: This commentary is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security, ETF, thematic strategy, sector, or investment product. Views are based on current market conditions, ETF flow and performance data, and third-party news sources that may change without notice. Thematic positioning comments are not tailored to any investor’s objectives, risk tolerance, or financial situation. Investors should conduct their own research and consult a qualified financial professional before making investment decisions. Past performance is not indicative of future results