COMMENTARY:

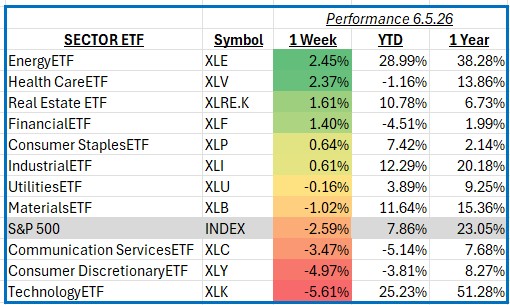

The S&P 500 Index declined 2.59% for the week ending June 5, 2026, as investors grappled with renewed concerns about economic growth and the outlook for interest rates. Market volatility increased throughout the week as investors evaluated mixed economic data and shifting expectations surrounding Federal Reserve policy. While employment data suggested the labor market remains relatively resilient, softer indicators from consumer spending and business activity raised concerns about the pace of economic growth. As a result, investors favored more defensive sectors while reducing exposure to higher-growth areas of the market.

Energy was the strongest-performing sector, gaining 2.5% for the week. Rising crude oil prices, supported by tightening global supply expectations and improving demand forecasts, provided a favorable backdrop for energy companies. Integrated oil producers and exploration firms led the sector higher as investors responded to improving earnings and cash flow prospects. The largest contributors to performance included Exxon Mobil, Chevron, and ConocoPhillips, which benefited from higher commodity prices and their ability to generate strong shareholder returns through dividends and share repurchases.

Health Care was another standout performer, advancing 2.4% during the week. Investors sought the relative stability and defensive characteristics often associated with the sector amid broader market weakness. Large pharmaceutical and managed-care companies attracted investor interest as earnings expectations remained steady despite growing economic uncertainty. Eli Lilly, UnitedHealth Group, and Johnson & Johnson were among the strongest contributors, supported by continued demand for medical treatments, favorable product outlooks, and resilient revenue growth expectations.

Technology was the weakest sector, falling 5.6% for the week. The decline reflected a broad pullback in growth-oriented stocks as investors reassessed valuations and reduced risk exposure. Semiconductor manufacturers and artificial intelligence-related companies were particularly affected following a period of strong performance earlier in the year. Major contributors to the sector’s weakness included NVIDIA, Microsoft, Apple, and Broadcom, as investors locked in gains and rotated toward more defensive sectors.

Consumer Discretionary also lagged, declining 5.0% during the week. Concerns surrounding consumer spending trends and the potential impact of slower economic growth weighed on the sector. Companies tied to retail spending, e-commerce, and discretionary purchases generally underperformed. Amazon and Tesla were among the largest detractors, while several consumer-focused businesses faced pressure as investors tempered expectations for future earnings growth.

Overall, this week’s market action reflected a shift toward defensive positioning as investors balanced economic uncertainty against generally healthy corporate fundamentals. Looking ahead, upcoming inflation reports, labor market data, and Federal Reserve commentary will remain key drivers of market sentiment.