Value has taken leadership from Growth in 2026, but the shift looks more like a valuation reset than the end of the Growth-led bull market that began in 2023. The market is not abandoning secular growth. It is becoming more selective about which Growth exposures deserve premium multiples, which companies have visible AI earnings leverage, and which businesses are most vulnerable to higher rates, pricing pressure and capex intensity.

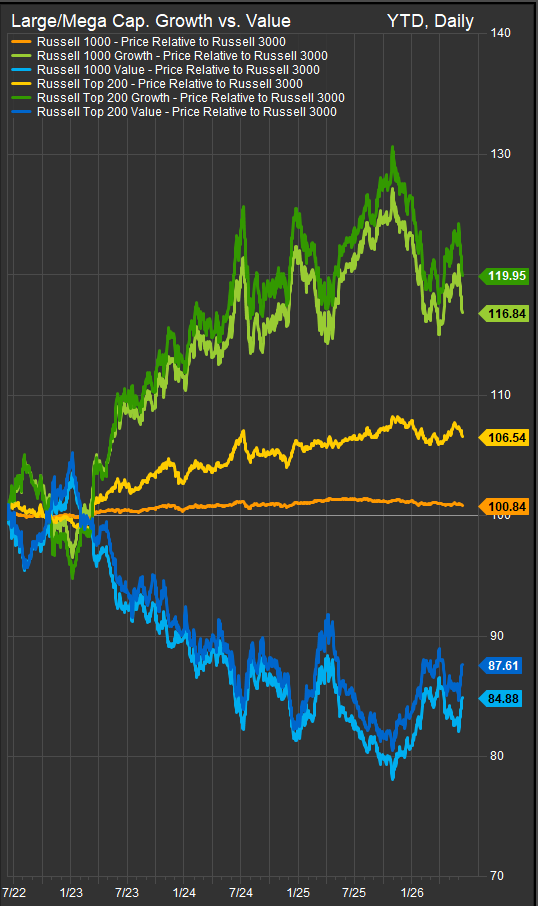

Large-cap Value benchmarks such as IWD and VTV have outperformed large-cap Growth benchmarks such as IWF and VUG year-to-date. That marks a clear reversal from the 2023–2025 tape, when mega-cap technology, semiconductors and AI infrastructure dominated market leadership. However, the rotation does not mean the AI trade is finished. It means the market is separating AI infrastructure winners from AI monetization stories that still need to prove margin durability.

Chart: Large cap. Growth benchmarks are retracing back to levels where previous leadership pivots have taken place.

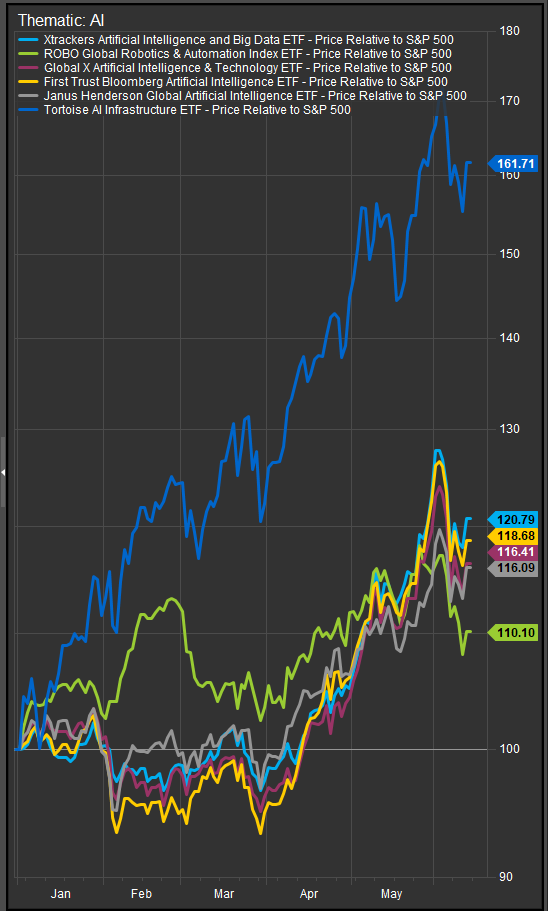

The cleanest distinction is between the physical AI buildout and the application layer. Investors continue to reward companies tied to compute, memory, storage, data centers, power delivery, cooling and networking. TCAI is a useful proxy for this part of the market because it owns AI infrastructure beneficiaries rather than simply software or platform companies. Holdings such as Micron, Dell, Seagate, Western Digital, Vertiv, Ciena and Quanta Services capture the bottlenecks that remain central to the AI capex cycle.

Chart: Most AI exposures remain in performance uptrends.

Chart: Watch TCAI price action near the 50-day moving average. $45 is a key level for the buyer to defend in the context of the uptrend.

Semiconductor ETFs such as SMH and SOXX also remain core AI infrastructure vehicles through Nvidia, Broadcom, AMD, Taiwan Semiconductor, Marvell and ASML. Broader Technology ETFs such as XLK, VGT and IYW still offer exposure to the mega-cap platform layer, including Microsoft, Apple, Nvidia and Broadcom. But the market is increasingly distinguishing between companies selling scarce AI capacity and companies trying to monetize AI services in an increasingly competitive pricing environment.

That distinction helps explain Growth’s relative weakness. Adobe remains exposed to AI-enabled creative tools, but investor concern has shifted toward freemium strategy, AI-first competition and pressure on ARR. Oracle has strong AI contract demand, but its heavy capex and funding needs have turned the debate toward return on invested capital. OpenAI and Anthropic pricing competition adds to the concern that AI adoption may accelerate while industry margins come under pressure.

The Fed outlook is central to the style debate. If inflation remains sticky and policy stays restrictive, Value can continue to lead because it offers nearer-term earnings, dividends, financial-sector leverage to rates and nominal-growth exposure. If inflation cools and the Fed regains room to sound less hawkish, Growth should recover some leadership, particularly in high-quality technology, semiconductors and AI infrastructure.

Chart: Rising real yields have been a headwind to Growth. Looking for reversal lower as the series approaches longer-term highs.

The conclusion is that Growth leadership is being repriced, not abandoned.

Chart: Semiconductors are retracing some outperformance vs. the broad market, but cyclical risk appetite is generally firming. We think this sets up an eventual “buy the dip” scenario for AI exposures.

Value is outperforming because the macro backdrop has become more favorable for near-term cash flows: firmer rates, better bank momentum, IPO activity, inflation optionality in Energy/Materials, and more investor interest in dividends and current earnings. But Growth still has several structural supports:

- AI capex is still expanding.

The market is still funding semiconductors, memory, data centers, power, cooling and networking. That supports names like NVDA, AVGO, MU, DELL, VRT, CIEN, PWR, and ETFs like TCAI, SMH, SOXX, VGT and XLK. - The problem is not AI demand; it is AI monetization.

OpenAI/Anthropic pricing pressure, Adobe’s AI competition concerns and Oracle’s capex debate are pressuring parts of software and platform Growth. But those concerns do not invalidate the infrastructure side of AI. They actually reinforce the need for cheaper compute, more chips, more storage and more power. - Mega-cap Growth still has balance-sheet and earnings quality.

Companies like MSFT, NVDA, AVGO, GOOGL, META and AMZN still have scale, cash flow, pricing power or infrastructure leverage that many classic cyclicals lack. That keeps institutional capital anchored in Growth, even when leadership narrows. - The Fed backdrop is not clearly hostile enough to end Growth.

The Friday brief noted markets had reduced expected 2026 rate hikes after improved Iran headlines, even though the June FOMC remains important given inflation risk. A mildly restrictive Fed can pressure Growth multiples, but it does not necessarily end a Growth cycle if earnings growth remains strong. - Value is leading partly because it was under-owned and cheaper.

Financials, Industrials, Energy and Materials are benefiting from a catch-up trade. That is different from saying Growth fundamentals have rolled over. Value can lead for a period while Growth remains in a secular uptrend.

Investors should not read Value’s 2026 outperformance as the end of AI or the end of Growth. They should read it as a market demanding more precision. For now, leadership favors current earnings, cash-flow visibility, infrastructure scarcity and inflation resilience.

Sources

- Friday morning StreetAccount news brief, including Iran de-escalation optimism, SpaceX IPO demand, Adobe’s AI competition concerns, Nasdaq-100 changes, jobless claims, CPI/PPI details, oil-market dynamics and the latest market-implied Fed path.

- iShares Russell 1000 Value ETF / IWD and iShares Russell 1000 Growth ETF / IWF performance data, used as large-cap Value and Growth benchmark proxies. IWD showed materially stronger YTD NAV total return than IWF in the latest available iShares data.

- Reuters Fed outlook reporting, including expectations that the Fed may stay restrictive through 2026 as inflation and labor-market resilience complicate the rate-cut case.

- Federal Reserve March 2026 Summary of Economic Projections, for the official Fed framework on 2026 policy-rate and inflation expectations.

- Tortoise AI Infrastructure ETF / TCAI fund materials, used as a proxy for AI infrastructure exposure.

Disclaimer: This material is for informational and educational purposes only and should not be considered investment advice, a recommendation to buy or sell any security, or a solicitation to engage in any investment strategy. ETF and benchmark performance figures are based on source data believed to be reliable but have not been independently verified. Past performance is not indicative of future results. Style investing, thematic ETFs and sector exposures may involve concentration risk, valuation risk, factor rotation risk, interest-rate sensitivity, geopolitical risk and sensitivity to changes in earnings expectations, inflation, Federal Reserve policy and investor sentiment. Investors should consult their own financial, tax and legal advisers before making investment decisions.