COMMANTARY:

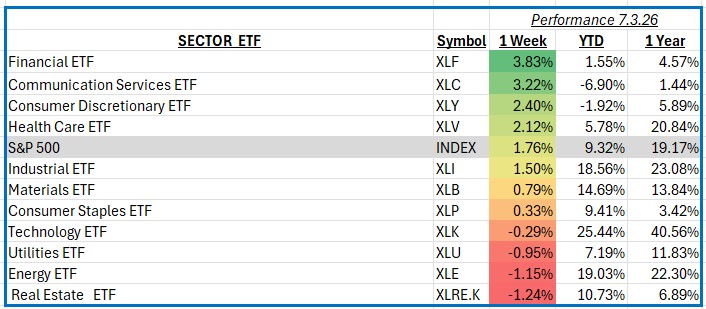

The S&P 500 advanced 1.76% during the shortened trading week, extending its recent rally as investors celebrated another round of encouraging economic data ahead of the Fourth of July holiday. Much like the fireworks that light up Independence Day, markets were fueled by renewed optimism surrounding resilient economic growth, moderating inflation, and increasing expectations that the Federal Reserve could begin lowering interest rates later this year. Investors also welcomed a stronger-than-expected employment report, which reinforced confidence that the U.S. economy continues to expand without showing significant signs of overheating. Together, these developments provided a patriotic backdrop for equities, with broad participation across many sectors.

Financials delivered the strongest performance of the week, gaining 3.8% as falling Treasury yields, healthy economic data, and optimism surrounding capital markets activity lifted investor sentiment. Large banks benefited from expectations for improved lending conditions and continued strength in consumer credit, while investment banking firms advanced on hopes for stronger dealmaking and underwriting activity. Leading contributors included JPMorgan Chase, Goldman Sachs, Visa, Mastercard, and Berkshire Hathaway, all of which posted solid gains as investors favored high-quality financial franchises with diverse revenue streams.

Communication Services also enjoyed a strong week, rising 3.2% as investors continued rotating into companies benefiting from digital advertising, artificial intelligence, and online engagement trends. Mega-cap technology and media companies once again led performance, supported by strong earnings expectations and continued enthusiasm for AI-driven investment spending. The sector’s biggest contributors included Meta Platforms, Alphabet, and Netflix, while improving sentiment toward digital advertising and cloud-based services further supported gains across the broader group.

Real Estate was among the week’s weakest performers, declining 1.2% as investors rotated toward more economically sensitive sectors despite modest declines in interest rates. Office and commercial property companies remained under pressure amid ongoing concerns surrounding occupancy levels and refinancing costs, while several residential real estate firms also traded lower. The largest detractors included Prologis, American Tower, Equinix, and Welltower, reflecting continued caution toward property-related businesses.

Energy also finished lower, falling 1.2% after crude oil prices softened on concerns that global supply could outpace demand despite healthy U.S. economic data. Investors also weighed the potential impact of steady production levels from major oil-producing nations. Integrated energy producers and exploration companies led the decline, with Exxon Mobil, Chevron, ConocoPhillips, and EOG Resources among the largest negative contributors as commodity prices weakened throughout the week.

As Americans celebrated Independence Day, investors also had reasons to celebrate another constructive week for markets. While leadership continued to rotate among sectors, resilient economic fundamentals and growing confidence in the outlook for monetary policy provided a solid foundation heading into the second half of the year.