ETF Insights | January 1, 2025 | Consumer Discretionary Sector

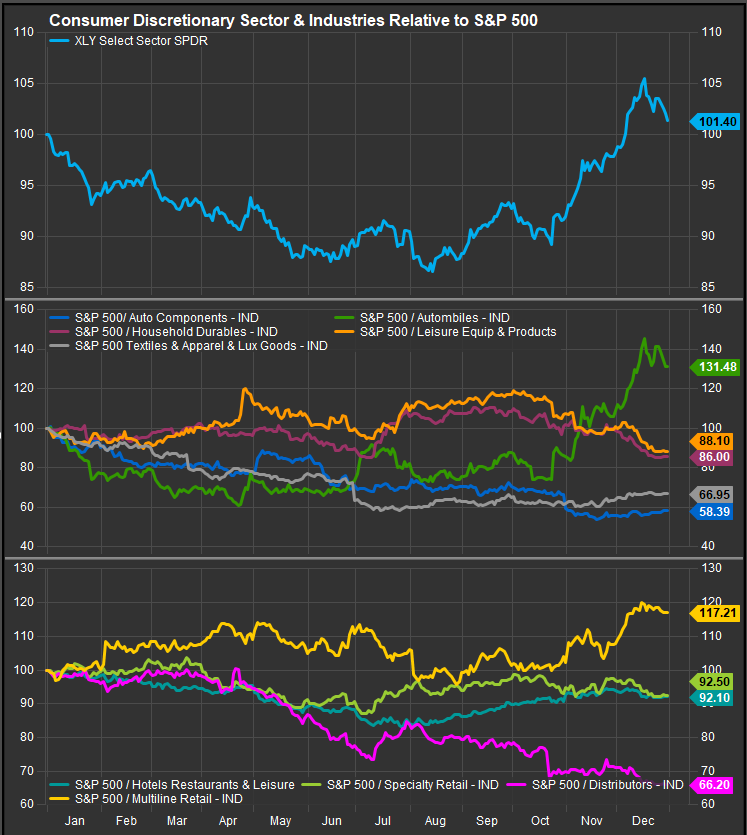

S&P 500 Discretionary Sector Price Action & Performance

The Discretionary Sector reached overbought conditions on the in mid-December with the RSI study (chart below, bottom panel) moving above the 80 level. Selling into year-end has alleviated that condition and presents a challenge to the buyer. We expect the bull trend to persist and for near-term weakness to be accumulated. A recent 52-wk relative high vs. the S&P 500 is a confirmation of the bull trend.

S&P 500 Discretionary Sector: Industry & Sub-Industry Performance Trends

Industry performance within the discretionary sector is all about Mag7 constituents AMZN and TSLA. Both stocks have been on a tear in the past 3 months and have boosted Multi-line Retail and Automobile industries respectively. Distributors, Textiles & Apparel and Auto components are the weakest areas of the sector. Each of these industries lagged the S&P 500 by >30%. Household Durables have gone from positive to negative as interest rates have backed up and start 2025 as a key potential pivot for the sector.

S&P 500 Discretionary Sector Breadth

Internal strength has deteriorated for the Discretionary sector in December with the % of stocks above their 50-day moving average falling from near 70% to below 40%. Strength in AMZN and TSLA accounts for almost all of the positive performance within the sector. With the S&P 500 index near “wash out” levels in aggregate, we’d expect outperformance on a bullish pivot.

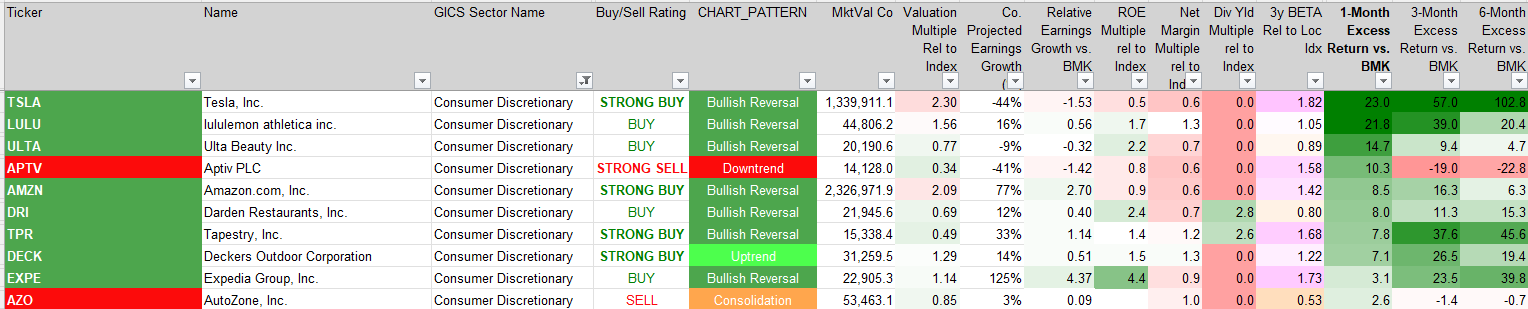

S&P 500 Discretionary Sector Top 10 Stock Performers

TSLA, LULU, ULTA and APTV all logged double-digit gains in December. Of the best performing stocks AMZN and EXPE fit the fundamental profile of continuing outperformance as they are growing earnings >2x the S&P 500

S&P 500 Discretionary Sector Bottom 10 Stock Performers

A number of housing stocks are showing up here as rapidly rising rates have scotched the outperformance trend there.

S&P 500 Discretionary Sector Fundamentals

The chart below shows S&P 500 Discretionary Sector FCF yield, and Dividend Yield as well as projected earnings over the next 3 years, valuation and trailing margins. Forward EPS estimates for the sector have been rising steadily throughout 2024 with the LTM earnings multiple at 27x tracking the broad market.

Economic and Policy Developments

Despite inflationary pressures, the US consumer showed signs of resilience. Reports highlighted steady holiday-season spending, driven by a robust labor market and sustained disposable income. Data on November pending home sales, which rose 2.2% month-over-month, indicated some stabilization in housing, indirectly supporting discretionary purchases tied to home improvement and furnishings.

However, headwinds persisted. Higher credit card defaults, which reached their highest level since 2010, raised concerns about consumer financial health. The Federal Reserve’s recent interest rate cuts provided some relief, but borrowing costs remained elevated, dampening large-ticket discretionary purchases such as vehicles and appliances.

Uncertainty surrounding trade policy under “Trump 2.0” raised potential risks for the discretionary sector. Reports of possible tariffs on European luxury goods and consumer electronics could disrupt global supply chains and impact pricing. At the same time, deregulation efforts anticipated under the new administration were seen as a tailwind for consumer-driven businesses, particularly in retail and automotive industries.

The holiday season remained pivotal, with e-commerce continuing to capture a larger share of retail sales. Amazon reported record-setting sales, while other online retailers also benefited from strong consumer demand. In contrast, traditional brick-and-mortar retailers struggled, with several downgrades reflecting concerns about declining foot traffic and competitive pressures from digital-first platforms.

Automotive stocks presented a mixed picture. Tesla maintained its leadership in the EV market, while traditional automakers like Ford and GM faced challenges from pricing competition and rising material costs. Meanwhile, travel-related discretionary stocks, including airlines and cruise operators, were supported by strong holiday travel demand but faced potential risks from rising fuel costs.

2025 Outlook

The S&P 500 Consumer Discretionary sector is poised for a cautiously optimistic 2025, underpinned by sustained consumer resilience and tailwinds from deregulation. E-commerce and EV markets are expected to maintain strong growth, supported by technological innovation and shifting consumer preferences. Amazon, Tesla, and other category leaders will likely remain key drivers of sector performance.

However, challenges remain. High interest rates and elevated credit card defaults could weigh on consumer spending, particularly for big-ticket items. Trade policy uncertainty and potential tariffs could disrupt global supply chains and increase costs for luxury and electronics companies. Additionally, slowing global demand, as evidenced by weak manufacturing data and uneven growth in China and Europe, could temper the sector’s momentum.

The outlook for the Consumer Discretionary sector will depend heavily on the trajectory of US economic growth and consumer confidence. Continued strength in the labor market and moderation in inflation could provide a supportive backdrop, while policy developments and global economic trends will present both opportunities and risks for sector performance.

In Conclusion

The average stock had a rough month in December, but oversold conditions for many stocks and the presence of Mega Cap. stalwarts AMZN and TSLA offer an attractive setup heading into 2025. We start 2025 with an overweight position of + 3.15% for the Discretionary sector in our Elev8 Sector Rotation Model Portfolio.

Data sourced from Factset Research Systems Inc.