ETF Insights | January 1, 2025 | Energy Sector

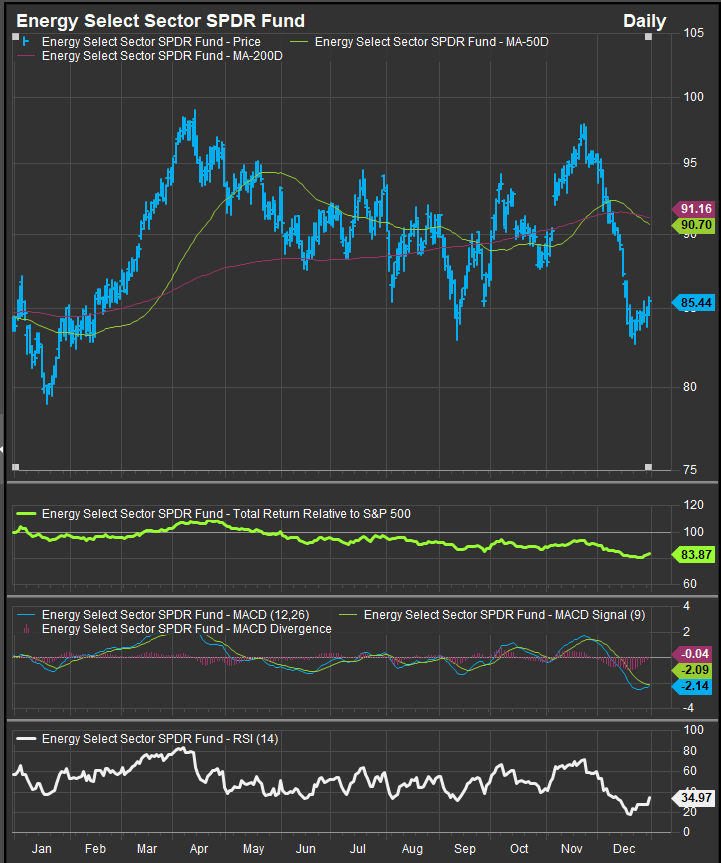

S&P 500 Energy Sector Price Action & Performance

The S&P 500 Energy Sector starts 2025 on an oversold condition after prices declined 10.5% in December. Energy stocks couldn’t overcome weak crude prices and a general lack of interest in commodities related equities. Materials and Industrial sectors also lagged in December. The 12-month price chart below shows the Energy Sector near lows for the period. Oscillator work is a bright spot, with the MACD study (chart, panel 3) about to trigger a tactical buy signal while the RSI study ticks up from a near-term oversold condition. Over the past 6 months the sector has lagged the broad market by >12%.

With prices near the bottom of the year’s trading range, we are expecting some upside reversion to take place, especially if rates stay high and squeeze investors out of Growth exposures.

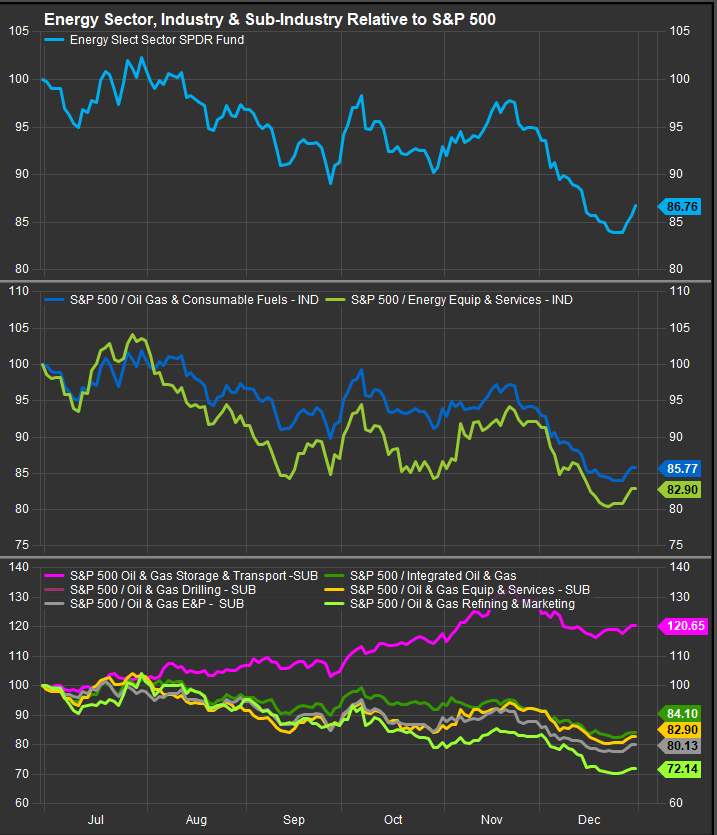

S&P 500 Energy Sector: Industry & Sub-Industry Performance Trends

The only standout theme within the energy sector is the Oil & Gas Storage and Transport Sub-Industry. This group of stocks, which includes MLP’s, pays out high dividends and has been the sole beneficiary of supply disruptions from global hostilities in Russia/Ukraine and the Middle East.

S&P 500 Energy Sector Breadth

As one would expect given the poor performance, market internals for the Energy Sector are among the weakest of the category. As of December 19, only 4% of Energy Sector stocks were above their 50-day moving averages. And while >50% of S&P 500 constituents are above their 200-day moving averages, only 29% of Energy Sector stocks can boast the same. We haven’t seen wash out conditions like this since 2023, and generally these breadth readings occur at market bottoms.

S&P 500 Energy Sector Top 10 Stock Performers

As we mentioned, Storage and Transport stocks have been standouts and names like WMB and KMI are members of that industry. Yes, only 2 Energy stocks printed positive returns in December. It has been a fallow year for Energy sector performance

S&P 500 Energy Sector Bottom 10 Stock Performers

Many double-digit drawdowns in December have us expecting an oversold bounce as we enter January. We note some of the best long-term performers like TPL, OKE and TRGP have been sold aggressively. These are names we are most interested in accumulating.

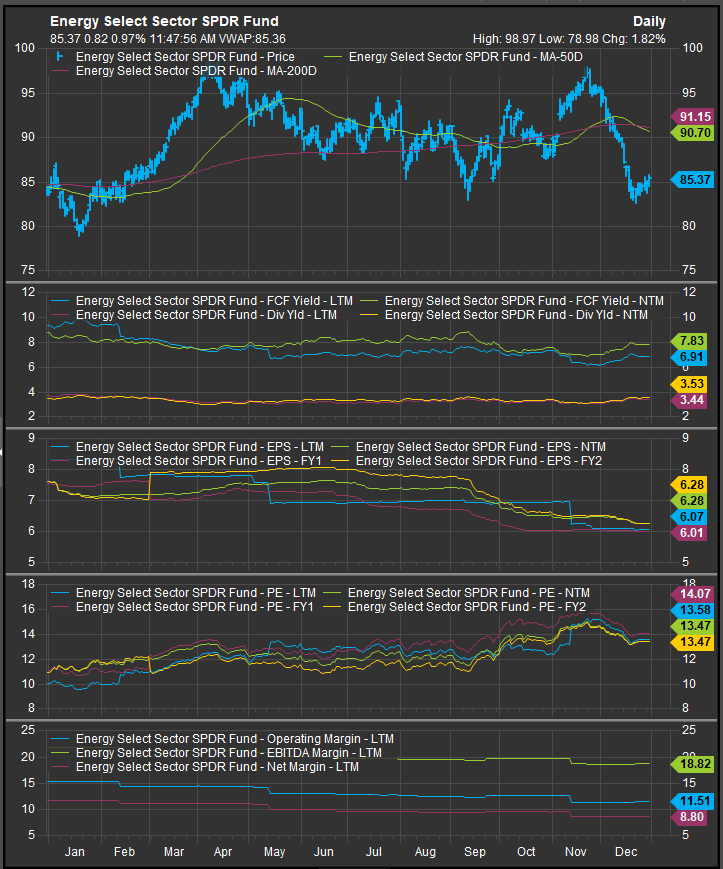

S&P 500 Energy Sector Fundamentals

The chart below shows S&P 500 Energy Sector FCF yield and Dividend Yield as well as projected earnings over the next 3 years, valuation and trailing margins. Cash flows and Dividend Yields have ticked higher as 2024 comes to a close, though that can be attributed to near-term selling. Unlike the broad S&P 500 index, where earnings are expected to grow around 10% per annum over the next several years, the Energy Sector earnings growth estimates are paltry. Despite this, valuation has expanded, though the sector currently trades at a 50% discount to the S&P 500’s aggregate valuation.

Economic & Macro Developments

Oil Supply and Demand Dynamics:

The Energy Information Administration (EIA) and industry reports highlighted stable US oil production levels in December 2024, with international supply concerns emerging from OPEC+ production targets and potential geopolitical disruptions. Domestically, Baker Hughes’ weekly rig count data reflected 589 active US rigs as of December 27, unchanged from the previous week but down 33 rigs year-over-year. Gulf of Mexico production remained strong, further contributing to domestic supply stability.

Global Demand Signals:

Optimism around China’s economic reopening and its potential impact on global oil demand was tempered by a sharp decline in the country’s industrial profits in December. This underscored the challenges to a robust demand recovery. However, a report from the Chinese government targeting record CNY3 trillion in special treasury bond issuance for 2025 provided some indirect support to energy markets, signaling potential fiscal stimulus that could boost broader economic activity and energy demand.

Policy Developments:

US trade and tariff policies under the anticipated “Trump 2.0” administration added uncertainty to energy markets. Reports of potential new tariffs could disrupt global trade flows, particularly for liquefied natural gas (LNG) exports and crude oil shipments. On the infrastructure front, Chevron and Alcoa announced a long-term gas supply deal in Western Australia, while Energy Transfer secured an LNG supply agreement with Chevron, underscoring continued strength in LNG markets and highlighting the sector’s growth potential.

Inflation and the Fed’s Stance:

Persistent inflationary pressures and the Federal Reserve’s easing cycle influenced interest rates, which indirectly impacted energy prices. Rising rates could increase the cost of capital for producers and infrastructure investments, posing challenges for future energy sector projects. However, the Fed’s stance on managing inflation while supporting economic growth remains a key factor for energy market stability heading into 2025

2025 Outlook

The S&P 500 Energy sector is likely to act as a haven if rising rates shake investors out of big Growth stocks in 2025. Absent that, structural headwinds are apparent as continued hot wars in oil producing regions were not able to move prices higher. Ukraine’s pipeline deal with Russia just ended as continued hostilities between the two sides scuttled any chance of renewal. This could be a catalyst for higher prices moving forward.

WTI crude prices are expected to maintain strength in the range of $75-$85 per barrel, barring major supply shocks. Natural gas markets could benefit from higher global demand, particularly in Europe and Asia, though domestic production increases may cap price spikes.

Energy equities, particularly those with robust balance sheets and exposure to LNG and renewable investments, are likely to attract investor attention. Companies like Chevron (CVX-US), Occidental Petroleum (OXY-US), and Exxon Mobil (XOM-US) are positioned well due to their diversified portfolios and strong cash flow generation. Emerging opportunities in carbon capture and renewable projects may also provide a longer-term growth avenue for the sector. In the meantime, Oil Storage and Transport stocks along with MLP’s have been the best performing areas of the sector. Low valuations and high dividend payouts have made those stocks attractive in this cycle.

In Conclusion

The best thing going for the S&P 500 Energy sector as it enters 2025 is that it ended 2024 unloved with prices at oversold conditions. If rising rates and outsized expectations lead to disappointing corporate earnings we could see rotation into laggard sectors and we would expect the Energy Sector to benefit in that scenario. We start 2025 with our Elev8 Sector Rotation Model overweight the Energy Sector by +0.88% relative to the S&P 500 benchmark weight.

Data sourced from Factset Research Systems Inc.