October 16, 2025

S&P futures +0.4% in Thursday morning trading, following a mixed but mostly higher session on Wednesday that saw short baskets, non-profitable tech, large banks, dollar stores, auto suppliers, and industrial metals lead the market. Regional banks, industrial distributors, trucking, aerospace & defense, insurance, and staples lagged, while big tech was generally weaker. Asian markets were mostly higher overnight with tech strength in South Korea, Japan, and Taiwan, while Greater China was little changed. European markets opened narrowly mixed. In macro markets, Treasuries steady to slightly firmer, Dollar Index -0.2%, gold +0.9%, Bitcoin -0.4%, and WTI crude +0.4%.

The key theme this morning is AI-driven optimism, led by TSMC’s guidance raise citing an “AI megatrend.” Broader macro headlines remain quiet — U.S.–China trade tensions persist but with no major new developments, as officials delivered mixed messages Wednesday. The government shutdown continues to dominate discussion around the data vacuum, with key releases like PPI, retail sales, and jobless claims delayed. Financial press coverage remains focused on buy-the-dip activity, retail investor inflows, short squeezes, and ongoing inflation and debt-quality concerns.

Corporate updates:

- TSMC (TSM) raised its 2025 revenue guidance, citing strong AI demand and a multi-year structural tailwind from hyperscaler investment.

- Salesforce (CRM) rose after raising its long-term targets, now guiding for $60B+ revenue by 2030 at its analyst day.

- Hewlett Packard Enterprise (HPE) fell after issuing underwhelming FY26 and long-term financial targets.

- United Airlines (UAL) beat expectations and raised guidance, though analysts flagged mixed Q3 unit revenue trends and a high bar following Delta’s strong print.

- J.B. Hunt (JBHT) jumped on a Q3 beat, with results highlighting strong cost discipline and improving freight efficiency.

- Zions Bancorporation (ZION) said it would take a $60M provision and $50M charge-off tied to two commercial & industrial loans.

- Apple (AAPL) reportedly lost another key AI executive to Meta (META), extending a series of high-profile AI talent departures.

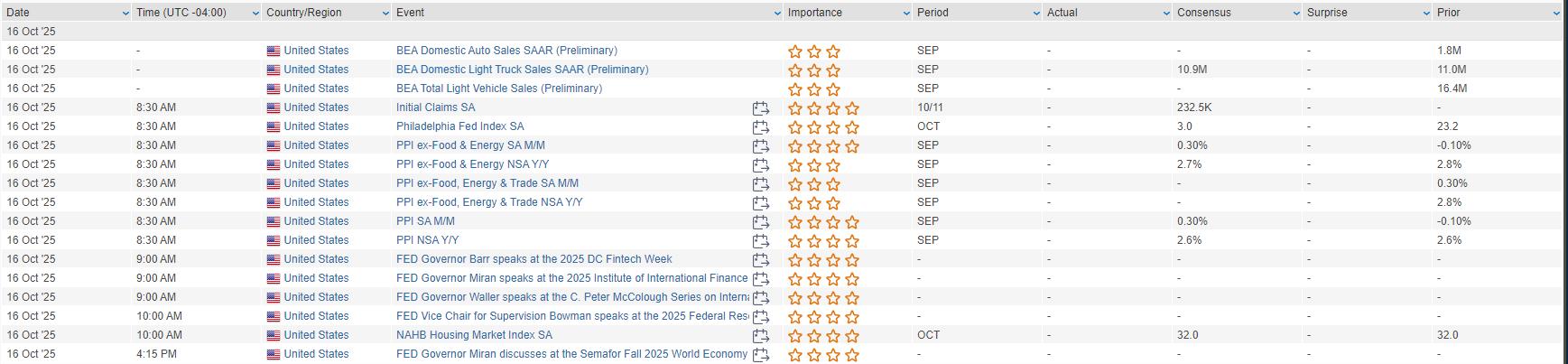

Economic data:

The Philadelphia Fed Manufacturing Index (expected +10.0 vs. +23.2 prior) and NAHB Housing Market Index (expected 33 vs. 32 prior) headline today’s calendar. Broader data flow remains limited by the shutdown.

Fed speakers:

A full slate of Fedspeak includes Waller, Barr, Miran, and Bowman. On Wednesday, Waller said AI adoption could accelerate layoffs, while Miran reiterated dovish views, stressing that U.S.–China trade risks add new headwinds to the outlook.

U.S. equities finished higher Wednesday (Dow -0.04% · S&P 500 +0.40% · Nasdaq +0.66% · Russell 2000 +0.97%), rebounding from early volatility as cyclicals and large-cap financials led gains. The S&P 500 and Nasdaq advanced modestly, while the Russell 2000 outperformed on renewed small-cap strength. Treasuries softened slightly, with front-end yields up ~3 bp. The Dollar Index -0.3%, gold +0.9% to $4,200/oz, Bitcoin -1.5%, and WTI crude -0.7%.

Markets navigated a mix of trade tensions, dovish Fed rhetoric, and strong earnings. While the U.S.–China trade standoff remains an overhang, traders are eyeing the upcoming Trump–Xi meeting for signs of de-escalation. Treasury Secretary Bessent said the U.S. won’t alter its negotiating stance despite market volatility and hinted at a potential trade truce extension if Beijing eases rare-earth restrictions.

Economic data were mixed but generally encouraging. The October Empire State Manufacturing Survey improved to its third positive reading in four months, showing gains in new orders and shipments, though prices rose further amid tariff and service-cost pressures. The Fed’s Beige Book described economic activity as “little changed” across districts, with firm wages and tariff-driven inflation persisting.

Fed commentary remained dovish-leaning. Governor Miran reiterated support for rate cuts, citing a lower neutral rate, while Governor Waller discussed AI’s productivity potential but cautioned that layoffs could rise temporarily. Markets remain priced for two additional 25 bp cuts by year-end.

Corporate dealmaking stayed active, highlighted by a $40 B AI data-center acquisition, the Hillenbrand buyout, and several privatization announcements.

Sector Highlights

Sector leadership was defensive and tech-led, with gains in real estate, utilities, communications, and semiconductors offset by weakness in materials and industrials.

- Outperformers: Real Estate (+1.50%), Utilities (+1.29%), Communication Svcs (+1.27%), Tech (+0.73%)

- Underperformers: Materials (-0.49%), Industrials (-0.47%), Energy (-0.08%), Financials (-0.08%), Healthcare (+0.03%), Consumer Disc (+0.10%), Consumer Spls (+0.15%)

Rotation into yield-sensitive sectors reflected dovish Fed sentiment, while semis and data-center names benefited from renewed AI enthusiasm and M&A activity.

Financials

- Bank of America (BAC): Q3 beat on revenue and EPS; NII/NIM higher, fees +5% on strong IB activity; raised low end of Q4 NII guidance.

- Morgan Stanley (MS): Q3 revenue beat by 10%, EPS beat by 30%; IB and trading strong, WM margins above 30%.

- PNC: Q3 beat on EPS/revenue but NII light, Q4 guide below consensus.

- Synchrony (SYF): Highlighted purchase volume growth; added $1 B buyback.

- Citizens (CFG): Q3 beat on stronger fees; expenses and NII inline.

- First Horizon (FHN): Beat on NII and EPS, but slid after M&A comments spurred concern.

- Progressive (PGR): Missed on EPS and revenue; claims ratio surged on policyholder credit expense.

- Thomson Reuters (TRI): Upgraded to Buy at GS; praised AI integration and revenue visibility.

Information Technology

- ASML: EPS and margins beat; bookings highest in 2 yrs; upbeat Q4 and FY26 outlook on AI demand.

- CRWV: Partnering with Nvidia-backed startup to build a West Texas data-center complex.

- Amphenol (APH): Upgraded to Buy at BofA; cited AI server buildout and acquisitions.

Communication Services

- GRND (Grindr): Confirmed receipt of go-private proposal.

- Papa John’s (PZZA): Jumped after Apollo’s $64/share buyout bid; multiple activists circling.

- TRUE (TrueCar): Soared after $277 M go-private deal led by founder consortium; expected to close Q4 2025/Q1 2026.

Industrials

- Hillenbrand (HI): To be acquired by Lone Star for $32/share ($3.8 B EV), a 37% premium.

- Prologis (PLD): Beat on FFO, raised FY25 guidance; highlighted record leasing volumes and data-center exposure.

- Nextracker (NXT): Announced 5 GW solar-manufacturing deal with TE; seen as expansion into domestic energy supply chain.

- Sable Offshore (SOC): Fell after CA court blocked pipeline restart at Santa Ynez project.

- Archer (ACHR): Acquired Lilium’s patent portfolio to expand IP footprint in electric aviation.

Consumer Discretionary

- Dollar Tree (DLTR): Reaffirmed near-term guidance; issued FY26 growth targets, signaling sustained value-retail momentum.

- Bunge (BG) & ADM: Rose after Trump said U.S. considering terminating China-linked ag contracts over soybean boycott.

Healthcare

- Abbott Labs (ABT): Q3 in line; narrowed FY25 EPS guide, solid med-devices growth offset by weak Nutrition.

- Alvotech (ALVO): Upgraded at MS on pipeline execution and global partnerships.

- Hims & Hers (HIMS): Surged on launch of menopause HRT offering; projected $1 B+ revenue by 2026.

Materials & Energy

- Sable Offshore (SOC): -20% after pipeline ruling.

Eco Data Releases | Thursday October 16th, 2025

S&P 500 Constituent Earnings Announcements | Thursday October 16th, 2025

Data sourced from FactSet Research Systems Inc.