October 22, 2025

Futures flat in Wednesday morning trading after U.S. equities ended mixed Tuesday, with the S&P 500 finishing near unchanged. Beneath the surface, momentum trades lost steam following a sharp selloff in precious metals. Big tech was mixed—AMZN outperformed on robotics headlines while GOOGL lagged amid AI competition concerns. Asian markets were mostly lower overnight, led by mining weakness in Australia, while Europe opened down ~0.4%. Treasuries little changed, Dollar +0.1%, Gold -0.4% after Tuesday’s 6% plunge, Bitcoin -2.5%, WTI crude +1.6%.

Macro focus centers on earnings, AI demand, and global trade optimism. Corporate results were mixed: underwhelming prints from NFLX and TXN but strong credit metrics from COF and WAL, easing regional-bank concerns. Reports that Anthropic is in talks with GOOGL for additional cloud capacity reinforced AI demand strength. Tuesday’s precious metals rout remains viewed as a technical pullback, not a shift in the “debasement” trade. Markets also shrugged off Trump’s China comments, with investors still expecting some de-escalation headlines from the upcoming Trump–Xi APEC meeting. Abroad, UK inflation cooled, Japan readied new stimulus, and U.S.–India trade talks gained traction.

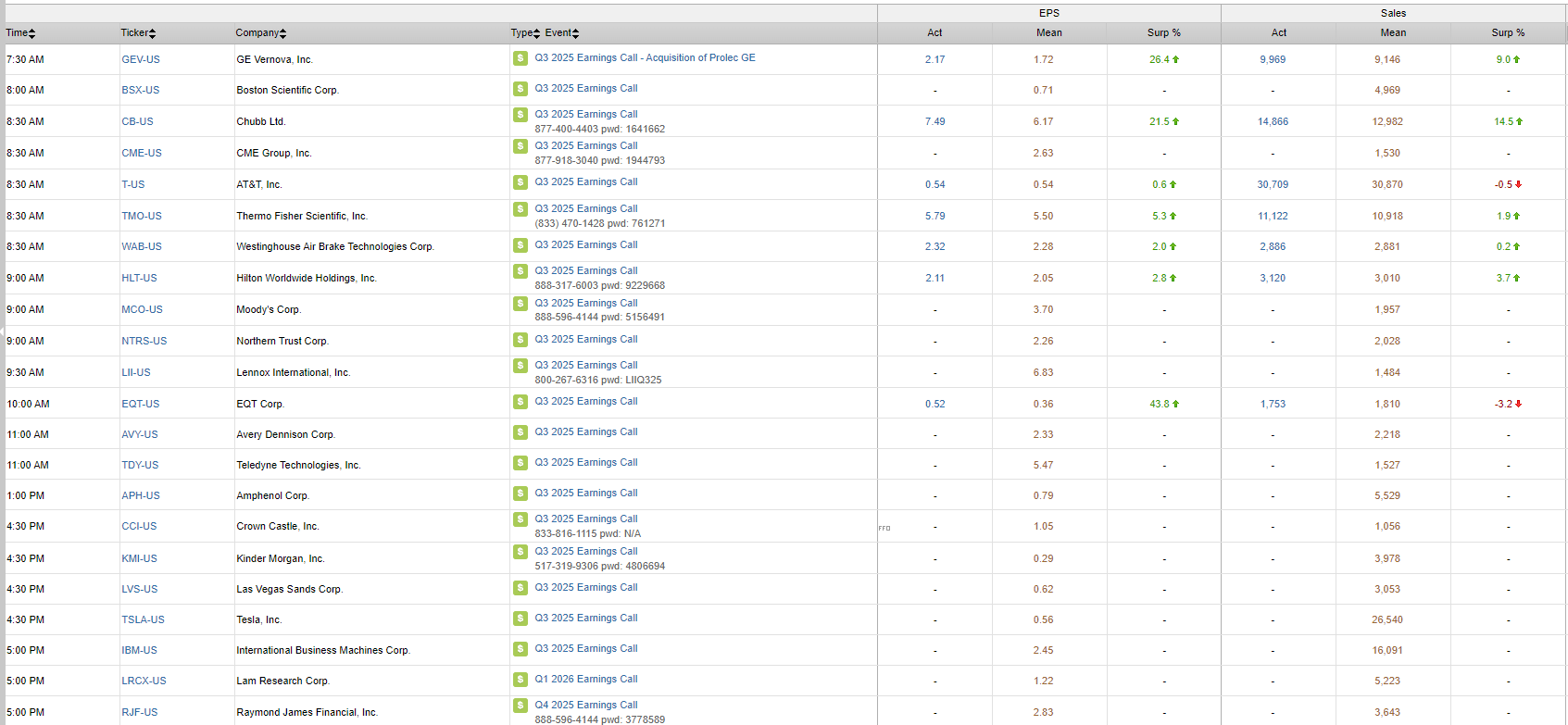

Corporate highlights:

- NFLX fell on lackluster Q3 results and soft Q4 guidance.

- TXN missed expectations, guiding to slower semiconductor recovery.

- ISRG beat on stronger procedure growth and system placements.

- COF beat, released reserves, and announced a $16B buyback.

- CB beat on better underwriting and lower catastrophe losses.

- WAL posted PPNR beat, strong deposit growth, reiterated NCO guide.

- WCN beat on margins; maintained FY guide.

- MAT missed on delayed retail orders but cited improving Q4 start.

- GOOGL up on report of new cloud deal with Anthropic.

- DKNG higher after acquiring predictions platform Railbird.

Macro calendar:

The Architectural Billings Index fell to 43.3 in September (from 47.2). No major U.S. data today. Thursday brings existing home sales and state-level jobless claims, while Friday’s delayed October CPI is the key event (headline +0.4% m/m, +3.1% y/y; core +0.3% m/m, +3.1% y/y expected). No Fedspeak ahead of the Oct 29 FOMC meeting, where another 25 bp cut is anticipated; markets continue to price in ~50 bp of total easing this year.

U.S. equities finished mixed Tuesday (Dow +0.47% · S&P 500 (0.00%) · Nasdaq (0.16%) · Russell 2000 +0.49%) in a quiet session that followed Monday’s strong rally, which had lifted all major indexes more than 1%. The Dow Jones Industrial Average closed at a record high, while the S&P 500 was little changed and the Nasdaq gave back modest ground. Breadth was uneven, with industrial cyclicals, defense, and consumer discretionary leading while utilities, materials, and staples lagged.

Investor sentiment remained constructive but cautious amid a light macro calendar and a growing focus on earnings. Roughly 85% of S&P 500 companies that have reported so far this quarter have topped EPS estimates, reinforcing the narrative of resilient corporate fundamentals and consumer demand. Meanwhile, the regional banking space continued to stabilize following recent credit-related volatility, with Zions’ (ZION) upbeat results easing fears about broader underwriting risks.

Macro headlines were relatively sparse. Reports pointed to some renewed uncertainty over a potential Trump–Xi meeting at next week’s APEC summit after Trump suggested it “may not happen.” Still, trade tensions were largely absent from markets, which continue to price in a benign policy backdrop. Commodity markets saw notable action, however, with gold plunging 5.7%—its worst day since 2013—amid technical selling and stretched positioning. Silver tumbled 7.2%, though Bitcoin rebounded 1%, helping to temper pressure on the “debasement trade.”

In fixed income, Treasuries firmed modestly, with the long end down roughly 3 bp, while the Dollar Index rose 0.4%. Crude oil gained 0.5%, reversing early losses. On the policy front, there was no Fedspeak ahead of the October 29 FOMC meeting, where another 25 bp cut remains widely expected. Friday’s delayed September CPI report will be the week’s key data point (headline +0.4% m/m, +3.1% y/y expected).

Sector Highlights

Outperformers: Consumer Discretionary (+1.32%), Industrials (+0.88%), Healthcare (+0.21%)

Underperformers: Utilities (-0.99%), Communication Services (-0.85%), Materials (-0.70%), Real Estate (-0.36%), Consumer Staples (-0.33%), Energy (-0.20%), Technology (-0.15%), Financials (-0.13%)

Information Technology

- GOOGL (-2.4%) – Fell after OpenAI unveiled “ChatGPT Atlas,” a new AI-powered web browser seen as a direct competitive threat to Chrome.

- CGNX (+2.0%) – Rose on Bloomberg report that Engaged Capital took a stake and urged cost cuts that could double valuation within two years.

- TXN – Reported after the close; investors watching for semiconductor order book trends given sector volatility.

Communication Services

- AMZN (+2.6%) – New York Times reported the company plans to automate up to 75% of its operations, potentially avoiding 160K new hires by 2027; seen as a long-term margin and productivity positive.

- WBD (+11.0%) – Jumped after CNBC reported the company has formally begun a sale process and is in talks with multiple potential bidders, including Netflix and Comcast.

- NFLX – Set to report post-close; expectations high after recent subscriber reacceleration.

Industrials

- RTX (+7.7%) – Posted broad-based Q3 beat and raised FY25 guidance; record backlog and strong aftermarket bookings supported results.

- GE (beat) – Raised FY guidance on engine aftermarket strength and resilient aerospace demand.

- LMT (-3.2%) – Delivered solid Q3 but lowered FCF guide and signaled softer Q4 implied by new EPS range; some concern about future charges.

- FLR (+ activist interest) – Higher after Starboard disclosed a stake.

- FUN (+17.7%) – Surged as activist Jana Partners and other investors took a ~9% stake and pushed for strategic alternatives, including a potential sale.

Materials

- CLF (-17.2%) – Downgraded to Underweight at Wells Fargo; analysts called Monday’s 21% rally on rare-earth and MOU headlines overdone without further detail.

- CCK (+5.5%) – Beat and raised FY25 guidance on European segment strength and better-than-expected FCF.

Energy

- HAL (+11.6%) – Beat on both revenue and EPS, driven by steady North American demand and cost-savings initiatives; highlighted $100M quarterly benefit from efficiencies.

Consumer Discretionary

- GM (+14.9%) – Strong beat across EPS, EBIT, and revenue; North America volumes ahead of plan; raised FY25 guidance and trimmed tariff impact forecast.

- MAT – Reported after the close with focus on holiday inventory management and pricing discipline.

- ADIDAS – Lifted FY earnings forecast amid robust retro sneaker demand (Bloomberg).

Consumer Staples

- KO (+4.1%) – Delivered earnings and revenue beats; organic growth above consensus driven by North America and EMEA; raised FCF guidance.

- PM (-3.8%) – Beat Q3 EPS but lowered OCI guide on higher Zyn promo spend; analysts flagged soft Americas margins and pricing pressure.

Health Care

- DHR (+6.0%) – Beat on EPS and revenue with respiratory and bioprocessing strength; maintained FY EPS guide and spoke positively on policy backdrop.

- HOLX (+2.9%) – Agreed to be acquired by Blackstone and TPG for $76 per share plus CVRs worth up to $3 per share, valuing deal at $18.3B EV.

- PCRX (-4.3%) – Dropped after news a Chinese firm filed an ANDA for a generic of Exparel; company vowed to defend IP.

Financials

- ZION (+1.4%) – Management said recent $50M fraud-related charge-off was isolated; credit metrics stable, criticized loans declining for second straight quarter.

- NDAQ (+1.7%) – Beat Q3 expectations on better Market Services and FinTech segments; slightly raised 2025 expense guide.

Utilities & Real Estate

- Sectors lagged on the day amid a renewed risk-on tone and higher growth expectations.

Eco Data Releases | Tuesday October 21st, 2025

S&P 500 Constituent Earnings Announcements | Tuesday October 21st, 2025

Data sourced from FactSet Research Systems Inc.