October 23, 2025

U.S. equity futures little changed Thursday after Wednesday’s selloff driven by a sharp unwind in momentum trades — most-shorted, retail favorites, AI, quantum computing, nuclear, and rare-earth names all under pressure. Semis, managed care, biotech, industrial metals, builders, airlines, banks, and telecom also lagged, while defensives outperformed. Overnight, Asian markets were mixed (Japan, South Korea, and Taiwan weighed by tech; Greater China higher), and Europe traded up ~0.2%. Treasuries weaker (yields +2–4 bp), Dollar +0.2%, Gold +1.7%, Bitcoin +1.6%, WTI +4.9% on Russian-sanctions headlines.

The oil rally dominated macro sentiment after the White House imposed major sanctions on Lukoil and Rosneft, stoking inflationary fears and lifting yields. The move coincided with progress on a potential U.S.–India trade pact. Meanwhile, trade-headline volatility persisted — Trump said he expects to reach a deal with China on trade and soybeans, offsetting earlier reports that the U.S. may restrict software-related exports in response to Beijing’s rare-earths limits.

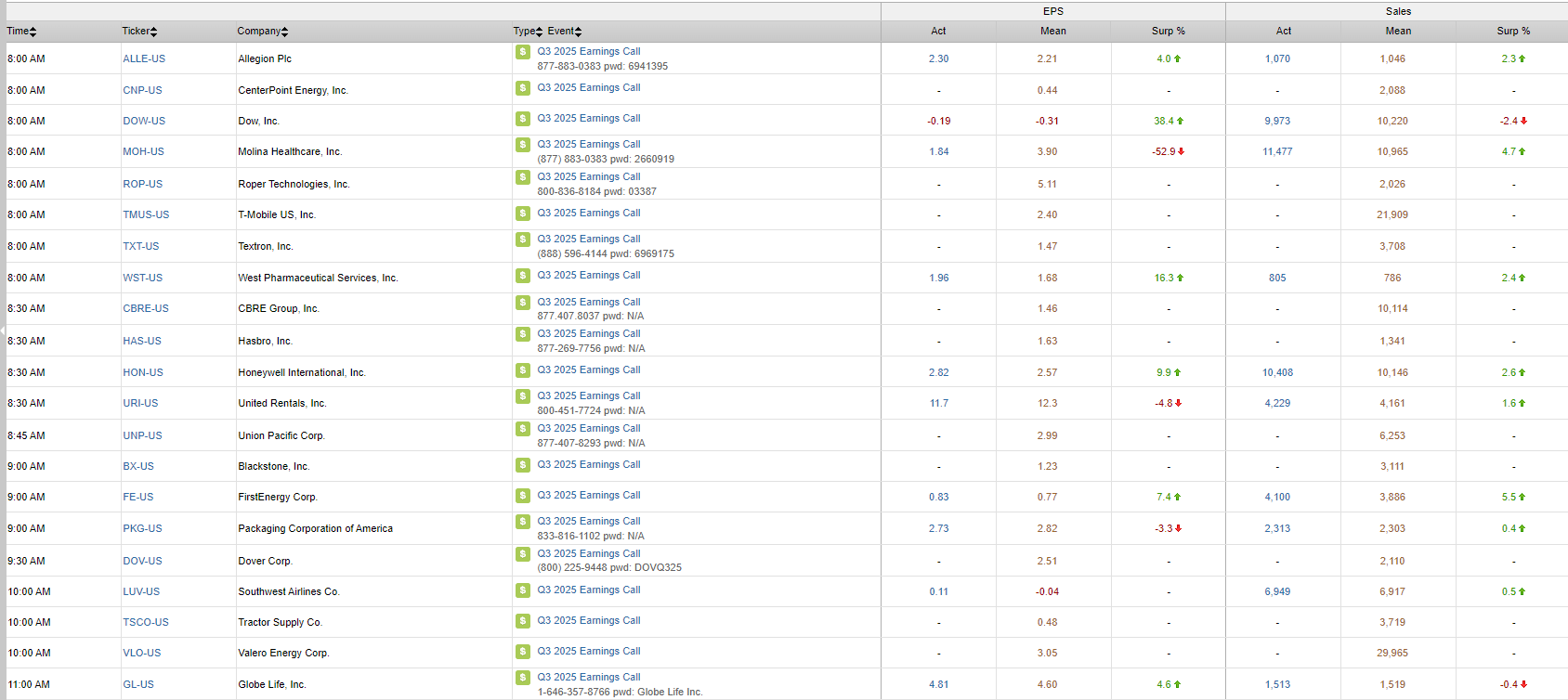

Earnings remained active, with mixed results. High-profile disappointments included TSLA, IBM, SAP, URI, and MOH, though overall Q3 beat rates remain strong. The momentum unwind continued to draw attention given heavy retail participation, but broader market implications remain unclear.

Corporate highlights:

- TSLA – Record deliveries drove revenue beat, but margins compressed.

- SAP – Guided FY cloud revenue to low end of range, though pipeline commentary upbeat.

- IBM – Weaker cloud software growth weighed on results.

- LRCX – Beat and raised, but cited slower China growth in 2026 and GM pressure.

- ORLY – Beat and raised FY outlook.

- LUV – Q3 ahead, reiterated EBIT guide.

- LVS – Beat, boosted capital return program.

- PKG – Missed, guided lower on Greif acquisition costs.

- WH – Cut FY guidance on softer RevPAR.

- URI – Missed on EBITDA; fleet productivity slowing.

- KNX – Guidance light on excess capacity.

- HXL – Cut FY guide citing tariffs and inflation.

- MOH – Down sharply on cost pressures.

- MEDP – Up strongly after broad beats.

Macro calendar:

September existing home sales due today; Friday’s delayed October CPI remains the week’s key event (Street: headline +0.4% m/m, +3.1% y/y; core +0.3% m/m, +3.1% y/y). Also on deck: flash PMIs, Michigan sentiment, and new-home sales. No Fedspeak ahead of the Oct 29 FOMC, with markets still pricing ~50 bp of additional easing this year

U.S. equities finished lower Wednesday (Dow (-0.71%) · S&P 500 (-0.53%) · Nasdaq (-0.93%) · Russell 2000 (-1.45%)) in a broad-based pullback that extended the prior session’s momentum unwind. The S&P 500 slipped modestly, closing off worst levels but seeing weakness across cyclicals, small caps, and higher-beta trades. Semiconductors, industrial metals, construction, and China-sensitive names led the declines, while energy and defensives outperformed. The Dow Jones Industrial Average fell 0.7%, the Nasdaq Composite 0.9%, and the Russell 2000 1.5%, marking one of small-caps’ worst sessions in a month.

Macro sentiment turned cautious as traders digested fresh U.S.–China trade headlines, mixed corporate earnings, and ongoing weakness in popular momentum trades. Reuters reported the White House is preparing new export restrictions on software-related goods to China—covering laptops, jet engines, and other technologies—representing a potential escalation ahead of the late-October Trump–Xi meeting at the APEC summit. The leak reversed optimism from earlier in the week that had suggested the administration might soften tariff enforcement and expand exemptions. Markets also took note of Trump’s renewed tariff threats (raising Chinese goods tariffs to 155% absent a deal by Nov 1) and the possibility of new limits on aircraft component exports, reintroducing trade-policy risk after several days of relative calm.

The macro tape also reflected shifting cross-asset positioning. A two-day collapse in precious metals continued early in the session (gold –1.1%, following Tuesday’s –6% plunge), though prices later stabilized as geopolitical tension over Ukraine re-introduced a modest risk-premium bid. Bitcoin futures –3.4%, extending declines from Tuesday’s rotation out of debasement trades, while the U.S. Dollar Index held flat after recent strength. Treasuries were little changed, the 10-year yield steady around 4.17%, with the 20-year auction drawing solid demand and stopping through by 1.2 bp—though foreign participation came in slightly below average.

In commodities, WTI crude +2.2%, rebounding after the U.S. authorized Ukraine’s use of Western-supplied long-range missiles against Russian forces, heightening geopolitical risk in energy markets. The move came amid EIA data showing a weekly crude draw and news of Saudi Arabia’s crude exports rising to a six-month high in August. Industrial metals were broadly weaker as traders continued to trim cyclical exposure.

Economic data remained light. The Architectural Billings Index slipped to 43.3 (from 47.2 in August), signaling another month of contraction in construction activity, though new project inquiries held roughly flat at 50.1. Attention now turns to Thursday’s existing home sales report and state-level jobless claims, which will feed into the Street’s national estimate. The main macro event remains Friday’s delayed October CPI—expected at +0.4% m/m and +3.1% y/y on the headline, +0.3% m/m and +3.1% y/y on core—followed by flash PMIs, University of Michigan sentiment, and September new-home sales. No Fedspeak is scheduled ahead of the Oct 29 FOMC meeting, where the Fed is widely expected to cut 25 bp; the market continues to price roughly 50 bp of additional easing into year-end.

Political coverage added to macro noise, with reports indicating the government shutdown is likely to extend into November as bipartisan negotiations remain stalled. Senate votes on the GOP’s stopgap funding bill again failed to make progress, and media coverage suggested the potential for the longest shutdown in U.S. history, with federal workers set to miss a paycheck by Oct 24.

Sector Performance

The Energy sector (+1.3%) led gains, supported by the oil rally and geopolitical tailwinds. Consumer Staples (+0.6%), Health Care (+0.6%), and Real Estate (+0.4%) saw modest outperformance on rotation into defensives. Industrials (-1.3%), Consumer Discretionary (-1.0%), Communication Services (-0.9%), and Technology (-0.8%) lagged on growth and cyclical exposure, while Financials (-0.6%) fell amid lingering credit concerns despite stable regional-bank earnings. The momentum unwind hit small caps and speculative trades hardest, underscoring the narrowing breadth beneath headline indexes.

Information Technology

- Texas Instruments (TXN -5.6%) – Q3 beat on revenue and EPS, but Q4 guidance ~2.5% below consensus; EPS miss > 10%; GM guide (55%) well below Street. Cited slower-than-normal cyclical recovery, macro uncertainty, and tariff caution.

- Vicor (VICR +30.3%) – Big EPS/GM beat, record licensing revenue; management said IP licensing could double within two years. Multiple upgrades followed.

- GE Vernova (GEV -1.6%) – Rev/EBITDA/FCF beat; wind revised lower, electrification raised; demand for grid equipment remains strong.

- Amphenol (APH) – Reported robust end-market demand, especially in IT datacom and industrial applications.

Communication Services

- Netflix (NFLX -10.1%) – Q3 in line; operating income missed on Brazil tax dispute; Q4 revenue guidance slightly better but implied limited acceleration; analysts flagged high valuation and a 40% YTD gain setting a high bar.

- Alphabet (GOOGL) – Higher earlier on report Anthropic seeking expanded cloud capacity; later faded with broader tech weakness.

Consumer Discretionary

- Hilton (HLT +3.4%) – Q3 EPS/revenue beat; raised FY guidance midpoints; optimistic on U.S. travel demand.

- Mattel (MAT -2.8%) – Missed on EPS/revenue; cited delayed retail orders rather than soft demand; said Q4 off to stronger start.

- DraftKings (DKNG +3.2%) – Announced acquisition of prediction-market platform Railbird to launch “DraftKings Predictions.”

- Winnebago (WGO +28.5%) – FQ4 sales/EBITDA beat; FY26 sales guide light but EPS ahead; emphasized margin and efficiency initiatives.

Consumer Staples

- Defensive retailers/grocers outperformed as investors rotated into lower-beta exposure.

Financials

- Capital One (COF +1.5%) – Beat on EPS, NII/NIM, and fee income; provision/NCOs below Street; released $760M in reserves; announced $16B buyback.

- Western Alliance (WAL) – PPNR beat; deposit growth strong; reiterated NCO guide, easing recent credit worries.

- PrimaLend bankruptcy kept subprime-auto lenders under scrutiny; Carvana (CVNA -8.2%) dropped on renewed short-seller comments.

Health Care

- Boston Scientific (BSX +4.0%) – Q3 EPS/revenue/margins beat; strong Watchman and Endoscopy segments; raised FY25 EPS and revenue growth outlook.

- Intuitive Surgical (ISRG +13.9%) – Q3 beat with >20% revenue/EPS growth for second straight quarter; raised 2025 procedure and margin guidance.

- Alkermes (ALKS) – To acquire Avadel (AVDL +3.7%) for up to $20/sh in cash; transaction expected immediately accretive.

- Thermo Fisher (TMO) – Strong organic growth and margins; cited strength in biotech instrumentation and diagnostics.

Industrials

- Underperformed overall as construction, electricals, and multis weakened.

- Teledyne (TDY -5.2%) – Beat but guided Q4 EPS midpoint below consensus; flagged backlog visibility issues amid shutdown uncertainty.

Energy

- Sector (+1.3%) led as oil rallied >2%. EIA data showing inventory draw and reports of increased Saudi exports added support.

- Halliburton (HAL +11.6%) – Q3 beat; highlighted $100M per-quarter cost savings and stable North American demand.

Materials

- Industrial metals weak; copper/aluminum under pressure.

- Packaging and waste outperformed: Crown Holdings (CCK) beat and raised FY25 EPS/FCF guide.

Real Estate

- Waste and logistics names firm; broader RE flat.

- Architectural Billings Index (43.3) highlighted softer construction pipeline.

Utilities

- Slight decline; investors favored staples and health care for defensiveness.

Eco Data Releases | Tuesday October 23rd, 2025

S&P 500 Constituent Earnings Announcements | Tuesday October 23rd, 2025

Data sourced from FactSet Research Systems Inc.