October 29, 2025

S&P futures +0.2% in Wednesday morning trading, following a Tuesday gain led by Big Tech, especially NVDA and MSFT. Despite the S&P finishing higher, over 75% of stocks declined and 8 of 11 sectors were lower. Asian markets rose (Japan, South Korea strong), Europe mixed. Treasuries weaker (yields +1–2 bp), Dollar +0.3%, Gold +1.1%, Bitcoin +0.1%, WTI −0.3%.

Markets are entering the most eventful stretch of the week: the FOMC decision this afternoon (expected 25 bp cut to 3.75–4.0% and potential QT end), Mag 7 earnings today and Thursday after the close, and the Trump–Xi meeting Thursday—where Trump confirmed plans to reduce fentanyl-linked tariffs on Chinese goods. AI enthusiasm remains a key driver following NVIDIA’s $500B+ Blackwell/Rubin backlog, ongoing partnership announcements, and positive earnings from select AI suppliers. Still, the rally remains narrow, and recent white-collar layoff headlines are drawing scrutiny around AI-driven productivity themes.

On the macro front, the Fed decision dominates today’s calendar; no major data until Chicago PMI Friday.

Corporate highlights:

- NVDA + on momentum and Trump comments about discussing chips with Xi.

- MSFT +2% after expanding OpenAI partnership (valued at ~$135B).

- TER, STX, BE, FLS, BKNG among post-close gainers on strong earnings.

- V flat on in-line results and guidance, noted resilient consumer spending.

- MDLZ, CSGP, VRNS, LRN, CZR among notable laggards.

- TMO near a ~$10B deal for Clario.

- RYI to acquire ZEUS in an all-stock merger

U.S. equities finished mostly higher on Tuesday (Dow +0.34% | S&P 500 +0.23% | Nasdaq +0.80% | Russell 2000 −0.55%) but faded into the close, with market breadth negative — the equal-weight S&P 500 (RSP) lagged the cap-weighted index by more than 110 bp. Gains were led by mega-cap tech, particularly NVIDIA, while small caps and cyclicals underperformed. Treasuries firmed across the curve (yields down 1–2 bp) as the 7-year auction tailed by 0.8 bp following solid 2- and 5-year demand on Monday. The Dollar Index slipped 0.1%, gold fell 0.9% (back below $4,000/oz), WTI crude dropped 1.9%, and Bitcoin declined 1.0%.

Macro data painted a resilient picture: October consumer confidence printed 94.6 (vs. 94.2 expected) with a stronger labor-market differential; Richmond Fed Manufacturing Index came in at −4 (better than −9.5 consensus), signaling improvement in shipments and new orders. Both Case-Shiller and FHFA home price indices rose in August. ADP announced it will begin publishing weekly preliminary jobs data, showing an average gain of 14K jobs per week through mid-October.

Markets remain in a holding pattern ahead of key catalysts: Wednesday’s FOMC decision (25 bp rate cut to 3.75–4.00% widely expected and possible end to QT), Mag 7 earnings (Wednesday and Thursday post-close), and the Trump–Xi summit on Thursday, where further tariff de-escalation headlines are anticipated.

Sector Highlights

Leadership was concentrated in Technology (+1.64%) and Consumer Discretionary (+0.31%), supported by NVDA, MSFT, CLS, CFLT, PYPL, and W. Most other sectors ended lower, with defensives and interest-rate sensitives weakest — Real Estate (−2.22%), Utilities (−1.66%), and Consumer Staples (−0.95%) lagged. Energy (−1.05%), Industrials (−0.73%), and Financials (−0.64%) also declined, while Materials (+0.14%) posted a slight gain. Overall, market leadership remained narrowly concentrated in large-cap tech and AI beneficiaries ahead of the week’s key FOMC and earnings catalysts.

Information Technology

- NVIDIA (NVDA) +5.0% – Jumped on GTC conference updates, including partnerships with Palantir, Uber, and CrowdStrike; CEO Huang dismissed AI bubble concerns.

- Microsoft (MSFT) +2.0% – Announced expanded OpenAI partnership, converting to a ~27% stake (~$135B valuation) as part of the nonprofit recapitalization; OpenAI committed to spend $250B on Azure services.

- Celestica (CLS) +8.2% – Beat and raised, guided FY26 EPS above Street; highlighted strong AI datacenter demand.

- Confluent (CFLT) +7.6% – Beat on subscription revenue, raised FY25 guidance; noted strong large-customer growth.

- PayPal (PYPL) +3.9% – Announced ChatGPT instant checkout integration; beat and raised FY EPS, initiated dividend.

- Skyworks (SWKS) & Qorvo (QRVO) – Confirmed $22B merger to form a new RF and connectivity platform.

- Corning (GLW) −3.3% – Beat estimates but Optical sales missed; sentiment pressured after 90% YTD rally.

- Rambus (RMBS) −8.7% – Q4 guidance underwhelmed after 115% YTD surge; analysts flagged stretched expectations.

Communication Services

- Nokia (NOK) +22.8% – Announced $1B equity investment from NVIDIA (2.9% stake) to accelerate 5G/6G RAN development and AI networking solutions.

- Alphabet (GOOGL) – Traded higher earlier in the session ahead of upcoming Mag 7 earnings; strength linked to OpenAI ecosystem news.

Consumer Discretionary

- Wayfair (W) +23.2% – Q3 beat on EPS, EBITDA, and revenue; best profitability since 2021; ad intensity improved 170 bp Y/Y.

- Royal Caribbean (RCL) −8.5% – EPS beat overshadowed by weak Q4 yield guidance; analysts flagged slowing onboard spend.

- VF Corp (VFC) −12.2% – FQ2 beat but cut Q3 revenue guidance; Vans remains weak despite TNF/Timberland growth.

- D.R. Horton (DHI) −3.2% – Missed EPS; guided for elevated incentives amid affordability pressures.

Consumer Staples

- Sysco (SYY) −2.7% – Margins and revenue in line; volume growth muted amid capacity investments.

- Kenvue (KVUE) −3.8% – Fell after Texas AG lawsuit alleging Tylenol marketing without adequate risk disclosure.

Financials

- Financials lagged broadly as regional banks and insurers weighed on index-level performance.

- PayPal (PYPL) stood out within FinTech space on OpenAI integration and solid results.

Health Care

- Regeneron (REGN) +11.8% – Q3 beat; Dupixent and Eylea both above forecasts; FDA response letter limited to syringe manufacturing issue.

- Managed care firms modestly higher, led by UnitedHealth (UNH).

Industrials

- UPS (UPS) +8.0% – Q3 beat on yield/margin strength; U.S. Domestic margins +100 bp Y/Y; strong cost discipline.

- Waste Management (WM) −4.5% – Missed estimates, trimmed FY25 revenue outlook; cited weaker healthcare solutions segment.

Materials

- Sherwin-Williams (SHW) +5.5% – Q3 beat; Paint Stores Group and Consumer Brands above expectations; raised FY revenue guide.

- ATI (ATI) +7.4% – Beat and raised FY guidance; strong free cash flow and efficiency gains.

- Olin (OLN) −12.5% – Weak Q4 guide tied to inventory cuts and Winchester margin pressure.

Energy

- Sector declined alongside crude (WTI −1.9%); no major earnings drivers in focus.

Utilities

- Group fell (−1.7%) amid ongoing curve flattening and defensive rotation out of rate-sensitive names.

Real Estate

- REITs slumped (−2.2%) as higher real yields and weak breadth weighed on property-linked sectors.

Eco Data Releases | Wednesday October 29th, 2025

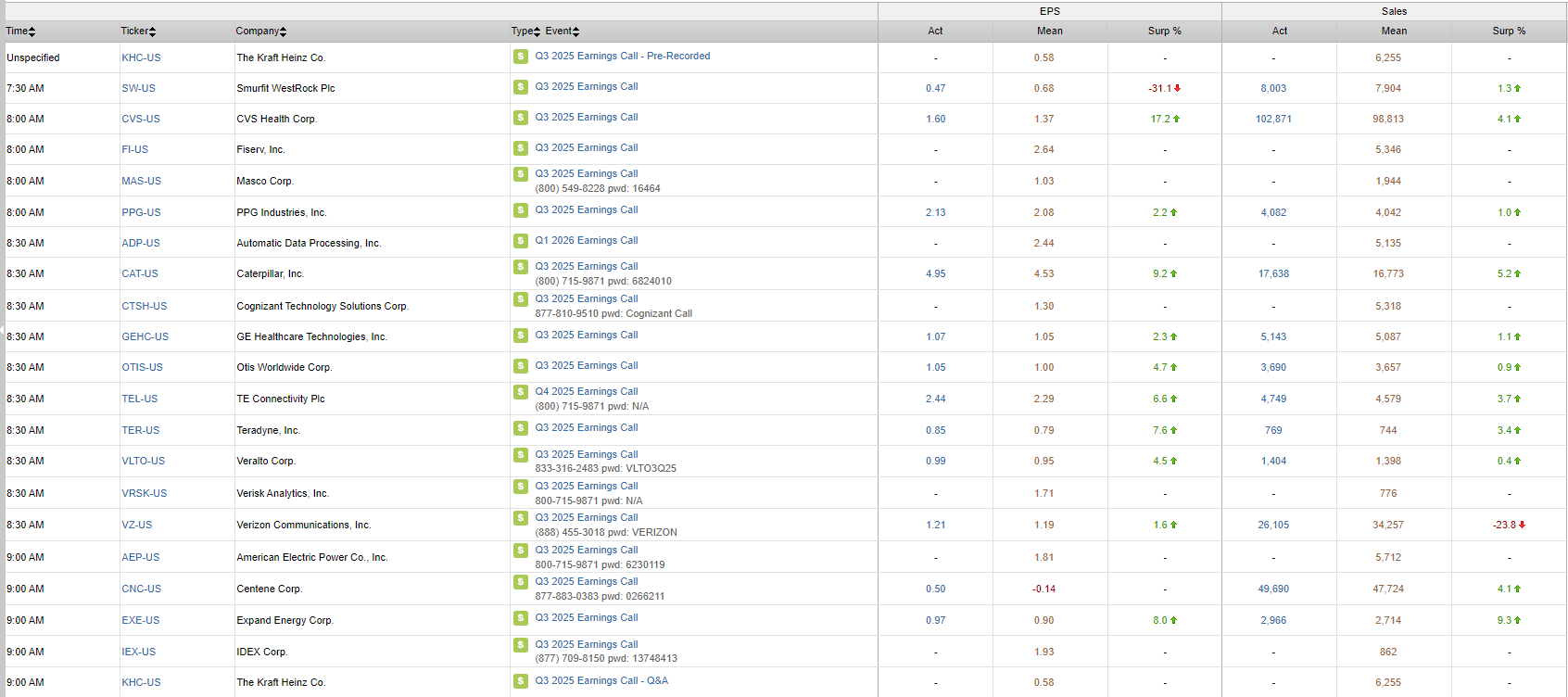

S&P 500 Constituent Earnings Announcements | Wednesday October 29th, 2025

Data sourced from FactSet Research Systems Inc.