February 13, 2025

S&P futures little changed Thursday morning after US equities pulled back Wednesday but closed well off session lows. Bond proxies, homebuilders, energy, aluminum, trucking, and ag chemicals lagged, while drug stores, autos, managed care, biotech, China tech, airlines, and exchanges outperformed. Asian markets were mixed, with Hong Kong giving back recent gains and Japan rising over 1%. European markets up ~1%. Treasuries firmer after Wednesday’s rate spike. Dollar index down 1%, with euro extending gains. Gold up 0.5%. Bitcoin futures down 1.6%. WTI crude down 1.5% after losing more than 2.5% in the prior session.

Markets await details on reciprocal tariffs, focusing on potential carveouts and non-tariff barrier adjustments. Broader uncertainty surrounds Trump 2.0 policies and a potential Trump-Putin meeting amid rising Ukraine ceasefire hopes, though spillover effects for US equities appear limited. Retail buying remains supportive but faces seasonal headwinds.

PPI and initial claims are on today’s economic calendar, alongside a $25B 30-year bond auction. Powell’s testimony failed to provide new insights, overshadowed by Wednesday’s hotter CPI report, which pushed the probability of a June rate cut below 50%, with markets now pricing just over 25 bp of easing for the year. Friday’s focus will be on retail sales, import/export prices, industrial production, and business inventories.

Company News

- Cisco (CSCO): Boosted by AI, Splunk synergies, and new product tailwinds.

- AppLovin (APP): Surged on a big earnings beat and strong advertising tailwinds.

- Fastly (FSLY): Pressured by margin headwinds and cash burn.

- Upwork (UPWK): Beat estimates, guided in line, but noted a still-challenging macro environment.

- Reddit (RDDT): Takeaways positive, but DAUs missed amid elevated expectations.

- Equinix (EQIX): Q4 results and 2025 guidance light.

- Robinhood (HOOD): Delivered a blowout quarter with strong January metrics.

- Dutch Bros (BROS): Rallied on strong comps.

- MGM Resorts (MGM): Helped by positive Las Vegas commentary.

- Royal Caribbean (RCL): Boosted dividend and announced a $1B buyback.

- MKS Instruments (MKSI): Beat estimates, but guidance was light.

- Albemarle (ALB): Gained on improved free cash flow outlook.

- Trade Desk (TTD): Missed expectations for the first time in over 30 quarters.

US equities closed lower on Wednesday, though stocks finished off their worst levels. The S&P 500 fell 0.16%, the Nasdaq declined 0.24%, and the Dow lost 0.18%. Underperformers included homebuilders, energy, E&Cs, aluminum, trucking, ag chemicals, hospitals, and bond proxy utilities and REITs. Big tech was mixed, with TSLA stabilizing after its MTD selloff. Outperformers included drug stores (CVS), legacy autos, managed care, biotech, copper, China tech, casinos, airlines, and exchanges. Treasuries weakened sharply, particularly in the belly of the curve, as the 10Y auction tailed. The dollar index fell 0.1%, reversing morning strength, with yen weakness dominating FX. Gold declined 0.1%, Bitcoin futures rose 2.1%, and WTI crude fell 2.7%.

The hotter-than-expected January CPI report and repricing for a more hawkish Fed rate-cut path were the biggest drivers of today’s downside. Markets are also awaiting clarity on Trump’s reciprocal tariffs, with NEC’s Hassett saying they remain a work in progress and White House press secretary Leavitt suggesting an announcement could come Thursday. House Speaker Johnson indicated the White House is considering exemptions on tariffs for autos and pharmaceuticals. Meanwhile, the GOP reconciliation bill remains in limbo as the House and Senate continue working on separate tracks. Additional headwinds include ongoing uncertainty surrounding Trump-Putin talks on Ukraine, the looming shift to January Q earnings (dominated by tech and retail), broadening earnings growth, softer guidance trends, divergent inflation expectations, Mag 7 performance, China/DAX outperformance, and higher energy prices.

January core CPI rose 0.4% m/m (vs. 0.3% consensus), its highest since April 2023, with headline CPI up 0.5% m/m. Annualized core CPI increased to 3.3% y/y, up from December’s 3.2%. Shelter costs rose 0.4%, accounting for 30% of the headline increase, while used vehicle prices also climbed, contributing to goods price acceleration. Following the report, the 2Y Treasury yield surged, with markets now pricing in a first Fed rate cut in December (delayed from September). Powell reiterated in his Senate testimony that the Fed still has work to do on inflation, while Atlanta Fed’s Bostic and Chicago’s Goolsbee both emphasized the need for caution. The 10Y auction tailed, with a $25B 30Y bond auction set for Thursday.

Company News by Sector

Technology

- Super Micro Computer (SMCI): +2.8% after management expressed confidence in filing overdue financial reports by Feb. 25, 2025, despite preliminary Q2/Q3 guidance coming in slightly below expectations.

- Confluent (CFLT): +25.1% on strong Q4 results, with upside in subscription and cloud revenue, an expanded Databricks partnership, and improved margins.

- Teradata (TDC): -20.3% after Q4 ARR and public cloud ARR missed expectations; Q1 and FY guidance were also weak, and the company announced a CFO transition.

- BlackLine (BL): -18.1% on weak Q4 EPS and FY25 guidance, citing macro volatility, customer timing issues, and FX headwinds.

Consumer Discretionary

- Upstart (UPST): +31.8% on a Q4 beat and positive 2025 guidance, with volume acceleration, updated underwriting models, and macro improvements driving upgrades.

- Lyft (LYFT): -7.9% on weak bookings due to a late-Q US pricing decline, which continued into January; Q1 guidance below expectations.

- Zillow (ZG): -10.7% despite Q4 revenue and EBITDA beats; Q1 revenue guidance was ahead, but EBITDA guidance was weak amid a more challenging housing market.

- DoorDash (DASH): +4.0% after GOV and EBITDA exceeded expectations; record MAUs and expanded merchant selection were highlights.

- General Motors (GM): +2.1% after House Speaker Johnson said the Trump administration is considering auto tariff exemptions.

- Lithia Motors (LAD): +4.6% after Q4 beats on EPS, EBITDA, and revenue, though GMs were light; analysts viewed new unit retail growth as stronger than expected.

Healthcare

- CVS Health (CVS): +15.0% on a Q4 beat, with strong prescription volumes and HC Benefits results; FY25 EPS guidance bracketed consensus.

- Gilead Sciences (GILD): +7.5% after Q4 results exceeded expectations, led by strong HIV business performance.

- Edwards Lifesciences (EW): +6.9% on solid Q4 organic growth, with TAVR and TMTT outperforming expectations.

- Biogen (BIIB): -4.3% after a Q4 beat but weak FY25 guidance, citing further declines in multiple sclerosis product revenue.

- STAAR Surgical (STAA): -24.7% on weak Q4 results, citing significant demand deterioration in China for cash-pay ICLs; company lowered FY25 outlook.

Financials

- CME Group (CME): +3.0% after a Q4 earnings and revenue beat, with strength in Market Data and ADV.

- Mercury General (MCY): +9.3% following a large Q4 EPS beat; Raymond James upgraded the stock to strong buy, highlighting subrogation potential.

Energy

- Chevron (CVX): Announced plans to cut up to 20% of its workforce by 2026, aiming for $3B in cost savings.

Industrials

- Wabtec (WAB): -9.1% on a Q4 EPS miss and weaker 2025 guidance, with organic growth and backlog expansion slowing.

- Allison Transmission (ALSN): -12.5% after Q4 revenue and EBITDA in line, but FY25 guidance came in light.

- Vertiv Holdings (VRT): -9.7% despite Q4 revenue and EPS beats; flat order growth and a lower organic sales growth outlook weighed on sentiment.

Materials & Industrials

- Martin Marietta (MLM): Cited continued softness in residential construction demand.

- Smurfit WestRock (SW): -5.1% after Q4 EBITDA and revenue missed across all segments; Q1 guidance also weak.

Consumer Staples

- Kraft Heinz (KHC): -3.3% after Q4 revenue was slightly below expectations; organic growth guidance for FY25 was weak due to expected volume declines. Shares were down 3.3% after Q4 revenue slightly missed; FY25 organic growth guide disappointed, citing volume declines.

Eco Data Releases | Thursday February 13th, 2025

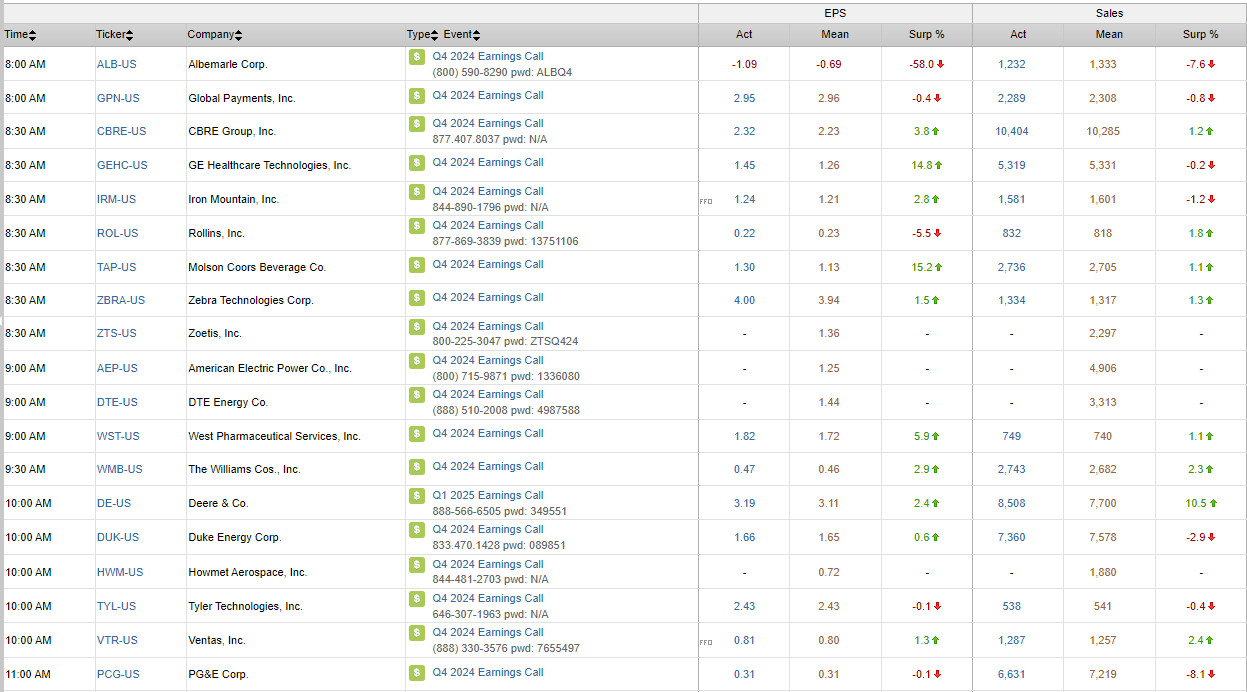

S&P 500 Constituent Earnings Announcements | Thursday February 13th, 2025

Data sourced from FactSet Research Systems Inc.