April 16, 2026

S&P futures are up 0.1% Thursday morning following another round of gains in U.S. equities, with both the S&P 500 and Nasdaq closing at fresh record highs. The Nasdaq has now advanced for 11 consecutive sessions, with mega-cap tech driving the bulk of the upside, particularly as software continues to rebound sharply after recent pressure.

The broader narrative remains intact, with the path of least resistance still higher. Markets continue to be supported by ceasefire durability, systematic fund re-risking, and improving risk sentiment, including some signs of renewed retail participation. While flows remain the dominant driver, the backdrop is being reinforced by solid macro data and constructive Q1 earnings commentary, particularly from the large banks.

AI continues to be a major tailwind, with ongoing focus on compute demand, chip deals, and infrastructure investment, reinforced by upbeat guidance from TSM. This week has also seen strong rebounds in software and private credit, two areas that had been under pressure, further supporting sentiment.

Cross-asset signals are relatively neutral. Treasuries are little changed, the dollar is slightly firmer, and commodities are mixed with oil higher and precious metals modestly up. Overall, the setup reflects strong momentum but limited incremental catalysts, leaving the rally dependent on flows, earnings, and AI-driven narratives.

Company Highlights

- TSM: Raised 2026 guidance and highlighted strong AI-driven demand outlook

- JBHT: Reported a beat and pointed to strong domestic intermodal demand alongside supportive regulatory changes

- PPG: Issued a positive Q1 preannouncement and plans to implement price increases of up to 20%

- SLG: FFO came in light due to lower JV income, though leasing activity reached a record Q1 level

- QDEL: Negative preannouncement tied to weaker respiratory demand, softness in China, and Middle East-related order delays

- HIMS: Benefiting from expectations that FDA may loosen restrictions on peptides

- OGN: Supported by reported takeover interest

- F: EV unit head Doug Field departing as part of a broader reorganization

U.S. equities extended their advance Wednesday with the S&P 500 +0.80%, Nasdaq +1.59%, and Russell 2000 +0.30%, pushing the S&P above 7,000 to a fresh all-time high. However, underlying breadth was less convincing, with equal-weight indices lagging, reinforcing that leadership remains concentrated in large-cap growth and AI-linked names.

The macro backdrop continues to skew supportive, with the path of least resistance higher driven by a combination of geopolitical de-escalation, systematic inflows, and constructive early earnings sentiment. Developments in the Iran conflict continue to point toward negotiation rather than escalation, with expectations building around a ceasefire extension. This has helped anchor risk appetite and reduce tail-risk concerns.

Flows remain a key driver. Sell-side desks continue to highlight mechanical support from systematic strategies following earlier de-risking, while AI-related optimism—particularly around compute demand, infrastructure buildout, and chip partnerships—remains a major tailwind. Software strength this week has been notable, driven more by positioning and valuation than incremental fundamental catalysts.

Economic data offered incremental support but a mixed picture. The Empire Manufacturing Index surprised to the upside, while import prices came in below expectations, signaling easing external inflation pressures. However, homebuilder sentiment dropped to a seven-month low, and the Fed’s Beige Book described only modest growth alongside rising geopolitical uncertainty. Fed commentary reinforced a patient stance, with rates viewed as appropriately set for now.

Cross-asset signals were mixed. Treasury yields rose 2–3 bp, the dollar edged slightly lower, gold declined modestly, and crude oil was largely unchanged. Overall, the macro environment reflects resilient growth with moderating inflation pressures, but still elevated geopolitical uncertainty.

Sector Highlights

Sector performance underscored a continued growth-led, risk-on rotation, though with some signs of narrowing participation.

- Outperformers:

- Technology (+2.08%)

- Consumer Discretionary (+1.37%)

- Communication Services (+1.07%)

- Underperformers:

- Materials (-1.30%)

- Industrials (-1.24%)

- Utilities (-0.93%)

- Health Care (-0.72%)

- Consumer Staples (-0.41%)

Financials (+0.76%) posted modest gains despite mixed earnings reactions, while Energy and Real Estate were roughly flat. The overall pattern highlights continued leadership from AI, growth, and consumer beta exposures, with cyclicals and defensives lagging—another sign that flows remain concentrated rather than broad-based.

Company Highlights

Information Technology

- GTLB +8.4%: Collaboration with GOOGL Cloud to expand AI-driven DevSecOps

- NET +6.4%: Upgraded (Piper Sandler) on infrastructure positioning and share gains

- AVGO +4.2%: Expanded partnership with META on custom AI silicon

- CRWV +higher: $1B investment from Jane Street; added as Hedgeye long idea

- ASML -2.4%: Mixed outlook despite strong orders; guidance only modestly ahead

Communication Services

- SNAP +7.9%: Positive preannouncement and ~16% workforce reduction tied to AI efficiency

- LYV -6.3%: Found liable for monopolizing ticketing market

Consumer Discretionary

- NKE +2.8%: Insider buying from CEO Elliott Hill and director Tim Cook (~$1M each)

- AEO +9.3%: New ad campaign boosting sentiment

Financials

- MS +4.5%: Strong trading-driven earnings beat

- BAC +1.8%: Beat driven by IB fees and equities; some expense caution

- PNC (mixed): NIM pressure offset by higher FY NII guidance

- PGR (weaker): EPS miss; concerns around growth deceleration

Health Care

- AVNS +69.5%: Acquired by American Industrial Partners (~72% premium)

Industrials

- EOSE +12.0%: AI-linked energy infrastructure partnership

Eco Data Releases | Thursday April 16th, 2026

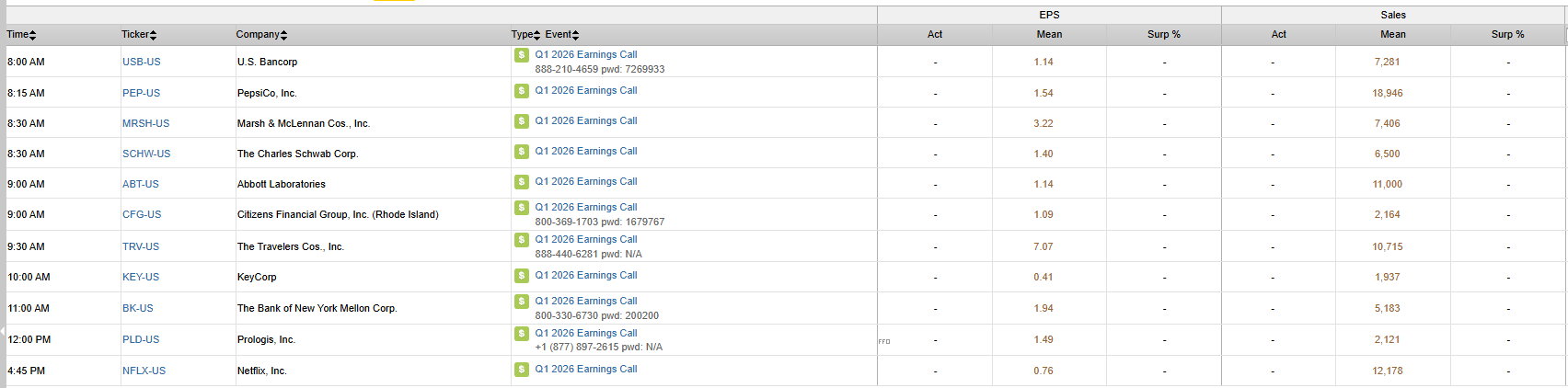

S&P 500 Constituent Earnings Announcements | Thursday April 16th, 2026

Data sourced from FactSet Research Systems Inc.