April 21, 2026

S&P futures are up 0.3% Tuesday morning after a mixed start to the week. While the Nasdaq ended lower Monday and snapped its 13-session winning streak, the broader tape was better beneath the surface, with six of eleven S&P sectors higher and the equal-weight index outperforming. Overseas markets were mostly firmer overnight, led by additional tech-driven strength in South Korea and Taiwan, while European equities are also higher. Treasuries are slightly weaker, the dollar is modestly firmer, gold is down, and WTI crude is off 0.8%.

The near-term tone is supported by a combination of renewed de-escalation hopes, AI enthusiasm, and a still-constructive earnings backdrop. Markets continue to lean toward the view that another round of U.S.-Iran talks in Pakistan can keep the ceasefire framework intact, with an extension seen as the easiest path to reduced geopolitical stress. Outside of geopolitics, attention is back on tech and AI after Apple’s CEO transition announcement and Amazon’s expanded Anthropic investment, while the rally in South Korea’s Kospi continues to reinforce the broader AI trade. Earnings sentiment remains generally upbeat, though investors increasingly see next week’s Mag 7 reports as the more important test.

This morning’s key catalysts are Trump’s CNBC appearance at 8:30, March retail sales and pending home sales, and Kevin Warsh’s Fed chair confirmation hearing at 10:00. Markets will be focused on whether Warsh pushes aggressively for lower rates, as well as his views on Fed independence, balance sheet policy, and the Powell investigation. The rest of the week includes jobless claims and flash PMIs on Thursday, followed by final University of Michigan sentiment and inflation expectations on Friday.

Company Highlights

- AAPL: Tim Cook will step down as CEO on September 1 and be succeeded by John Ternus, current SVP of Hardware Engineering

- AMZN / Anthropic: Amazon will invest up to another $25B in Anthropic, which in turn committed to spend more than $100B on AWS over the next decade

- ACGL: Increased its buyback authorization by $3B

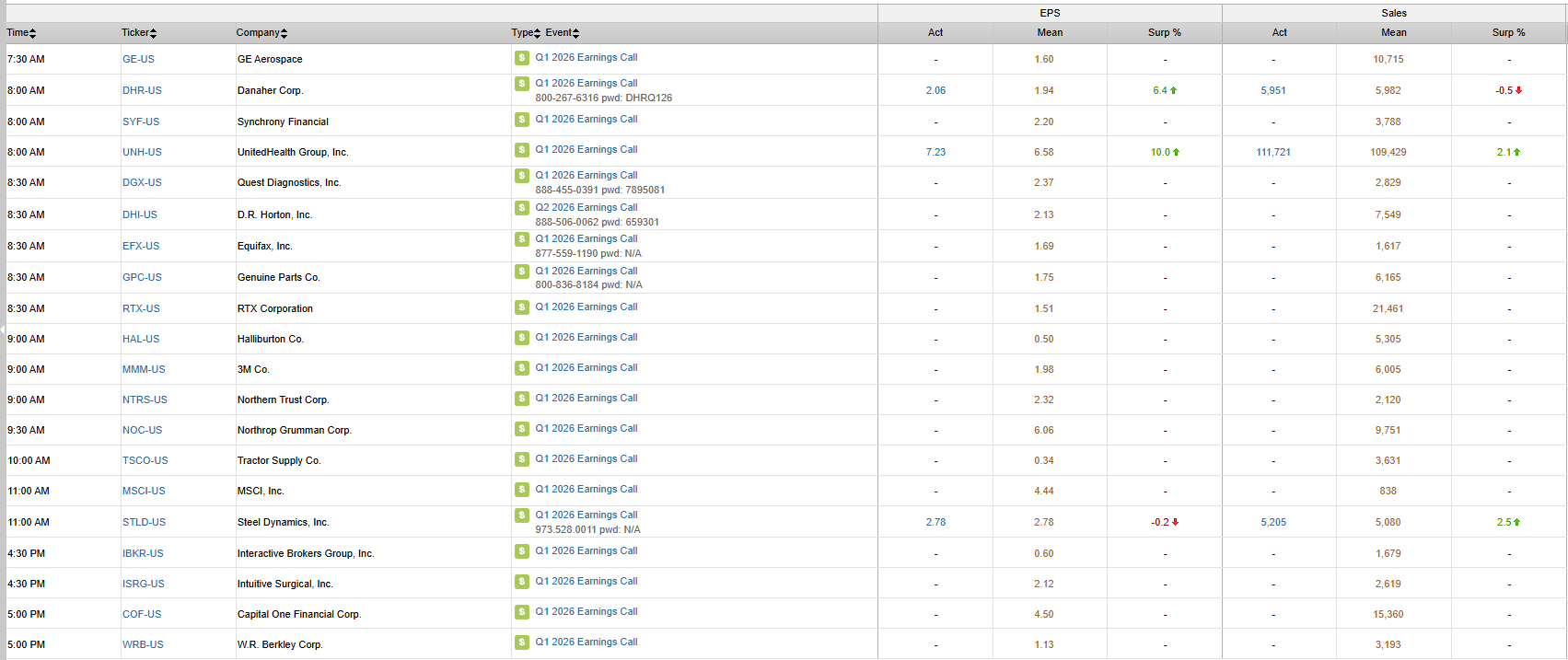

- STLD: Q1 results were largely in line; management highlighted improving steel market conditions

- ZION: Missed on NIM, NII, and expenses, though maintained 2026 guidance trends

- AGNC: Tangible book value fell 6%, worse than expected, though core EPS beat and April spread trends have improved

- SNAP: Announced the departure of its CFO

- ALK: Issued upbeat Q2 RASM guidance, but flagged a $600M fuel headwind that implies a much larger loss than expected

U.S. equities were mostly lower Monday, though stocks finished well off their worst levels after opening the week with a more defensive tone. The S&P 500 fell 0.24%, the Nasdaq declined 0.26%, while the Russell 2000 gained 0.58%, with equal-weight S&P outperforming the cap-weighted index by roughly 55 bp. The Nasdaq’s 13-session winning streak ended, while Treasuries were little changed to slightly weaker, the dollar eased 0.1%, gold fell 1.0%, silver dropped 2.2%, and WTI crude rose 5.9%.

The softer tone reflected a weekend increase in Middle East tensions, though the market’s reaction remained relatively contained. Investors continue to frame the conflict through a broader de-escalation lens, even with headline volatility still elevated. That muted response also reflects confidence that systematic strategy re-risking still has room to run, a dynamic that has been a major support for equities in recent weeks.

Beyond geopolitics, the broader macro narrative remains constructive. Street commentary continues to emphasize a solid economic backdrop, a good start to Q1 earnings season, resilient consumer trends highlighted by the banks, continued AI compute and capex enthusiasm, support from tax refunds, lower effective energy intensity, and a pickup in M&A activity. With no U.S. economic data released Monday and the Fed in blackout, attention now shifts to Tuesday’s retail sales, pending home sales, and Kevin Warsh’s confirmation hearing, followed later in the week by jobless claims, flash PMIs, and final University of Michigan sentiment and inflation expectations.

Sector Highlights

Sector performance reflected a rotation away from the prior narrow large-cap leadership and toward more cyclical and value-oriented groups. Materials (+0.57%), Financials (+0.34%), Real Estate (+0.27%), Energy (+0.21%), and Industrials (+0.18%) led the session, while Communication Services (-1.41%), Health Care (-0.93%), Utilities (-0.91%), and Consumer Discretionary (-0.65%) lagged. Technology was little changed overall, though software held up better than many higher-profile growth groups. The pattern suggested a modest defensive shift at the index level, but also a more balanced tape beneath the surface, with cyclicals, banks, insurers, and small caps showing relative resilience.

Information Technology

- MRVL +5.8%: Reportedly in talks with GOOGL to develop two new chips aimed at running AI models more efficiently

- OKTA +4.9%: Upgraded to overweight at Barclays on improving vendor spending trends and exposure to faster-growing identity segments

- FRMI -17.6%: Pressured by the immediate departure of co-founder and CEO Toby Neugebauer, alongside the CFO’s resignation

Communication Services

- META: Reuters reported plans to cut roughly 10% of its workforce next month, with further reductions later this year

- GOOGL: Also in focus for reported custom chip talks with MRVL

- CRM: Marc Benioff pushed back against AI-related concerns and said the company plans to unveil a new AI platform by year-end

Consumer Discretionary

- CAR +23.3%: CNBC reported major holders had not sold shares despite the recent rally

- ULTA +3.4%: Upgraded to buy at Jefferies on improved confidence in revenue durability and a better beauty backdrop

- AAL -4.2%: Said it is not engaged in, or interested in, merger discussions with UAL

- ABNB: FT reported the company is adding hotels to its platform to support growth

Consumer Staples

- BF.B: Reports said the controlling family sees a merger with Pernod Ricard as a better fit despite talk of a $15B all-cash bid from Sazerac

- CALM -1.9%: Fell on reports the DOJ is preparing an antitrust lawsuit against major U.S. egg producers

Health Care

- BIIB +3.4%: Acquired exclusive rights to felzartamab in Greater China and was upgraded to overweight at Wells Fargo

- LLY: Agreed to acquire Kelonia Therapeutics for $7B in cash

- ATAI and DFTX: Rose sharply on an executive order aimed at accelerating regulatory development of psychedelics for mental health

Financials

- OWL: Agreed to acquire SILA in a $2.4B all-cash deal

- APO: Taking a $1.25B strategic minority stake in McKesson’s MSS segment

- SILA +19.1%: Rose on the takeover announcement

Industrials

- QXO: Acquiring BLD for $17B

- BRC: Acquiring Honeywell’s Productivity Solutions and Services business for $1.4B in cash

- ASTS -5.3%: Reported the loss of BlueBird 7 after a launch-orbit issue

- CLF -2.1%: Maintained guidance, though management said the Middle East situation is complicating talks with POSCO

- BLD: In focus on the QXO acquisition

Eco Data Releases | Tuesday April 21st, 2026

S&P 500 Constituent Earnings Announcements | Tuesday April 21st, 2026

Data sourced from FactSet Research Systems Inc.