April 22, 2026

S&P futures are up 0.6% Wednesday morning after Tuesday’s selloff left stocks near session lows. The rebound is being helped by a ceasefire extension, which supports the broader de-escalation narrative, though the continued U.S. blockade is still keeping concerns alive around physical energy disruption, especially in refined products. Cross-asset tone is constructive: Treasury yields are down 2–4 bp, the dollar is slightly weaker, gold and silver are higher, Bitcoin is stronger, and WTI crude is up modestly.

Outside geopolitics, the main market themes remain familiar: AI and data-center capex strength, resilient consumer demand, higher memory costs, fuel-price pressure, and pricing power. Software is also staying in focus after its recent rebound, with Adobe adding support through a new $25B buyback. High-profile M&A continues to help sentiment, including reports that SpaceX has secured an option to acquire AI coding startup Cursor.

No U.S. economic data are due today. The main item on the calendar is the $13B 20-year Treasury auction at 1 p.m. ET. Attention then shifts to jobless claims and flash PMIs on Thursday, followed by final University of Michigan sentiment and inflation expectations on Friday.

Company Highlights

- ABB: Reported a triple-digit increase in data-center orders and raised guidance

- ISRG: Beat and raised procedure growth guidance

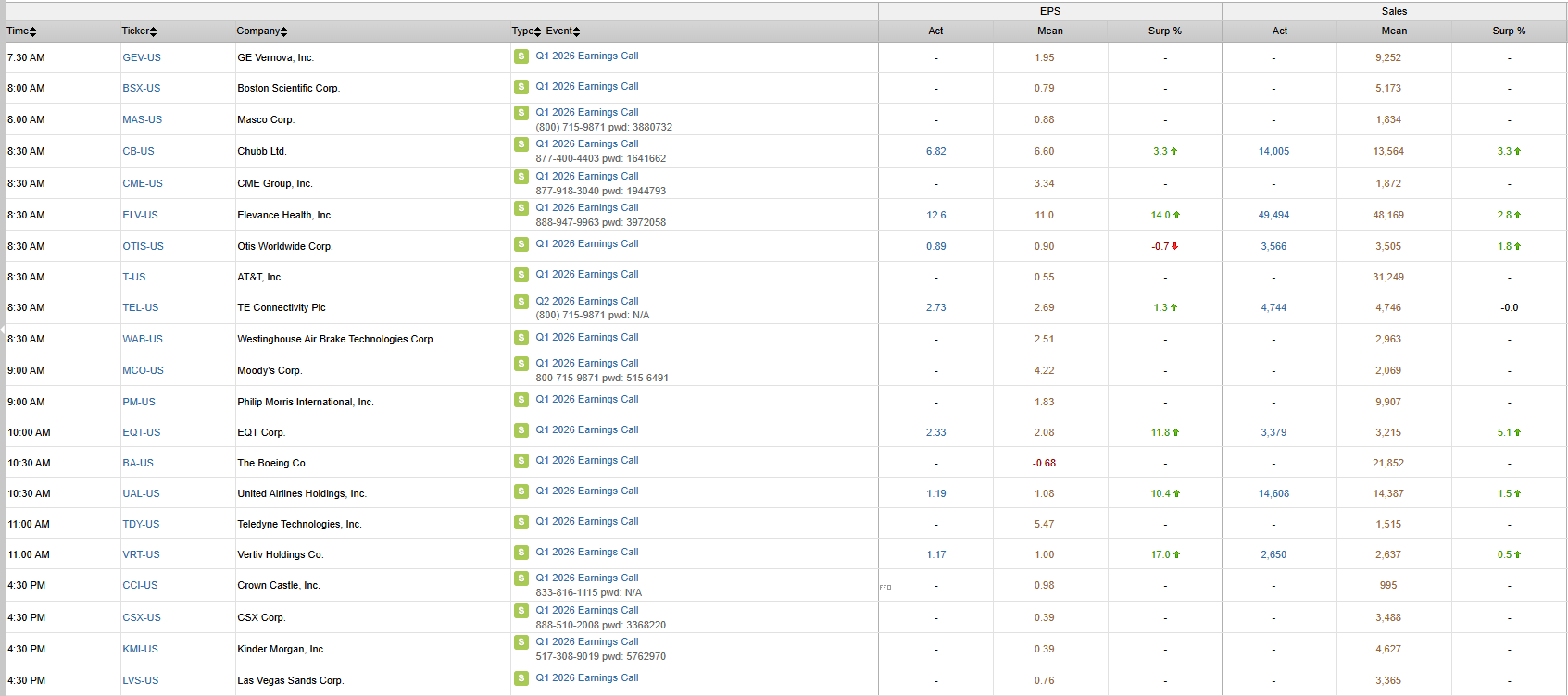

- COF: Missed on NII and provision

- UAL: Issued a light Q2 guide and lowered full-year guidance on fuel pressure, though demand trends remained solid

- MANH: Beat and raised; Street encouraged by RPO strength and bookings momentum

- WFRD: Q2 guide was light due to Middle East disruption, though second-half outlook remained intact

- SON: Lowered 2026 EPS guidance on weaker demand and inflation pressure

- CALX: Under pressure on a weaker Q2 EPS guide tied to higher memory costs

- ADBE: Announced a new $25B buyback program

- TFX: Boosted by a privatization report

- SpaceX / Cursor: SpaceX reportedly secured an option to acquire Cursor for $60B

U.S. equities declined Tuesday, with the Dow down 0.59%, the S&P 500 down 0.63%, the Nasdaq down 0.59%, and the Russell 2000 down 1.00%, as stocks finished near session lows. The move came alongside a more defensive cross-asset backdrop: Treasury yields rose sharply, with the 2-year up 8 bp and the 10-year up 6 bp, the dollar strengthened 0.5%, gold fell 2.3%, silver dropped 4.4%, and WTI crude rose 2.6%, extending gains after the latest Iran headlines.

The main macro driver was a renewed setback in the market’s de-escalation narrative around Iran. Reports that Vice President Vance had called off his trip to Pakistan for a second round of talks with Tehran reversed earlier optimism and revived concern that the market may have moved too quickly toward pricing in a smooth geopolitical resolution. That mattered because much of the recent upside had been built on the assumption that investors could move past geopolitics and refocus on growth, AI, and earnings. Tuesday’s reversal suggested that assumption is still vulnerable.

Even so, the broader macro backdrop remained firmer than the equity close alone would suggest. March retail sales rose 1.7% m/m, ahead of the 1.4% consensus, while control-group sales increased 0.7%, well above the 0.2% forecast. Pending home sales also beat expectations, and ADP’s preliminary four-week job-creation measure accelerated again, pointing to continued support from consumption and labor trends. Kevin Warsh’s confirmation hearing was largely uneventful from a market standpoint, with little incremental policy signal beyond support for Fed independence. Overall, the day reflected a market pressured by geopolitics and higher yields, but still operating against a backdrop of resilient consumption, steady labor conditions, and generally constructive earnings season commentary.

Sector Highlights

Sector performance reflected a clear risk-off and rate-sensitive rotation, with economically sensitive growth areas and defensives both under pressure, while energy was the standout beneficiary of higher oil. Energy (+1.31%) was the only sector to post a meaningful gain, while Technology (-0.23%), Consumer Staples (-0.47%), Consumer Discretionary (-0.49%), and Financials (-0.63%) held up relatively better than the broader market. The weakest groups were Real Estate (-1.94%), Utilities (-1.75%), Industrials (-1.39%), Communication Services (-1.24%), Materials (-1.23%), and Health Care (-1.01%). The pattern pointed to pressure from rising yields, renewed geopolitical uncertainty, and broad negative breadth, even as software and selected semis showed relative resilience beneath the surface.

Information Technology

- AAPL: Announced that Tim Cook will step down as CEO on 1-Sep and be succeeded by Hardware Engineering SVP John Ternus

- CRWD +3.8%: Upgraded to overweight at KeyBanc, with the firm citing AI-driven cybersecurity demand and the breadth of the Falcon platform

- VICR +9.5%: Q1 earnings and revenue beat, though management said it expects to remain capacity constrained for a substantial period

- MRVL / GOOGL: The Information reported the two are in talks to develop custom chips designed to run AI models more efficiently

Communication Services

- AMZN: Will invest up to another $25B in Anthropic, with Anthropic committing to spend more than $100B over the next decade on AWS technology

- SNAP -6.0%: Fell after announcing the departure of CFO Derek Andersen

- CRM: Marc Benioff pushed back against AI fears and said the company plans to unveil a new AI platform by year-end

Consumer Discretionary

- TSCO -11.7%: Revenue, comps, and EPS missed as weakness in the Companion Animal segment weighed on results

- LCID +5.3%: Rose after Uber disclosed an 11.5% passive stake, making it the company’s second-largest shareholder

- ALK -4.8%: Q2 outlook was hurt by a $600M fuel headwind and higher-than-expected costs, prompting suspension of 2026 guidance

Health Care

- UNH +7.0%: Beat and raised guidance, with better-than-expected medical cost trends and improved Optum results

- DGX +4.5%: Q1 earnings and revenue beat, helped by strong organic requisition-volume growth; guidance was raised

- MRK -3.9%: Fell after a Phase 3 renal cell carcinoma study with Eisai failed to meet dual primary endpoints

- LLY -1.8%: Weakened alongside other GLP-1 names after UNH commentary highlighted uncertainty around obesity drug coverage models

Financials

- SYF: Beat and announced a $6.5B buyback, though expenses were higher and guidance was maintained

- ZION: Missed on NIM, NII, and expenses, though management maintained 2026 guidance trends

- PRU -6.0%: Pressured by reports of suspected financial fraud at Prudential Gibraltar and the possibility of an extended sales pause

- MSCI: Highlighted strong performance in its Index and Analytics businesses

Industrials

- NOC -7.0%: Revenue and EPS beat, but free cash flow was significantly weaker than expected despite reaffirmed guidance

- GE -5.6%: Q1 results beat and the company said it is trending toward the high end of guidance, but the stock fell with the broader A&D group

- DHI +5.8%: Better gross margins, order performance, and Q3 guide were the key positives

- STLD: Q1 was largely in line, with management talking up improving steel market conditions

- HAL +4.0%: Q1 beat with strength in Completion & Production and Drilling & Evaluation, alongside positive commentary on North America and the Middle East

Eco Data Releases | Wednesday April 22nd, 2026

No constituents report today.

S&P 500 Constituent Earnings Announcements | Wednesday April 22nd, 2026

Data sourced from FactSet Research Systems Inc.