April 29, 2026

S&P futures are up modestly Wednesday morning after a mostly lower Tuesday session. The market remains in a holding pattern ahead of the first major wave of Mag 7 earnings tonight from AMZN, GOOGL, META, and MSFT. Recent weakness has been concentrated in AI-linked semis and infrastructure names after reports that OpenAI missed internal targets, while Energy continues to benefit from higher oil. Treasuries are slightly weaker, the dollar is firmer, precious metals are lower, and WTI crude is up another 3.6%.

The main focus remains the intersection of AI spending and macro risk. Investors are looking for answers on capex, capex guidance, ROI, monetization, and productivity from hyperscalers. Broader Q1 earnings trends remain strong, with blended S&P 500 earnings growth now above 15.5%, and recent reports have continued to highlight AI compute demand, consumer resilience, limited fallout from the Middle East, and capital return. At the same time, the ongoing rise in oil is reinforcing concerns that the U.S.-Iran conflict could become more prolonged, raising the risk of physical supply disruption and complicating the rate outlook.

Today’s macro calendar is busy, with durable goods orders and housing starts/building permits this morning, followed by the FOMC decision at 2:00 p.m. ET and Powell’s press conference at 2:30. Thursday brings Q1 GDP, ECI, PCE inflation, and jobless claims, while ISM manufacturing closes out the week on Friday.

Company Highlights

- V: Beat and raised; highlighted improving U.S. volume growth, resilient consumer spending, and announced a $20B buyback

- STX: Beat and raised on stronger cloud and enterprise demand

- BKNG: Q1 mixed and Q2 guidance light; flagged temporary Middle East headwinds

- SBUX: Helped by North America comp strength and a higher FY26 comp outlook

- BE: Boosted by a beat and raise

- MDLZ: Beat and highlighted broad-based geographic strength, especially in emerging markets

- TER: Sold off despite a strong beat on AI tailwinds, with investors focused on only modest upside in June guidance

- NXPI: Moved higher as June guidance came in well above expectations

- TMUS / PPG / FICO / FFIV: Among the other notable earnings gainers

- HOOD / LRN / ENPH / WERN / OI: Among the notable earnings laggards

- DIS: Reportedly decided against spinning off ESPN

- BF.B: Said it is no longer in talks to be acquired by Pernod Ricard

U.S. equities finished lower on Tuesday, though stocks recovered from their worst levels by the close. The S&P 500 fell 0.49%, the Nasdaq dropped 0.90%, the Russell 2000 lost 1.15%, and the Dow slipped 0.05%. The broader tone turned more defensive as Treasury yields moved higher, with the front end under the most pressure, while the dollar strengthened 0.2%. Gold fell 1.8%, silver dropped 2.4%, Bitcoin futures were down 0.7%, and WTI crude settled up 3.7%, finishing just shy of $100 per barrel.

The main macro concern was a renewed debate around AI spending sustainability after reports suggested OpenAI had recently missed internal user and revenue targets. Even though the company pushed back on the report, the timing mattered given how powerful the AI trade had been in recent weeks, particularly for semiconductors and data-center beneficiaries. That pressure came alongside a more challenging technical backdrop, with systematic re-risking largely exhausted, sentiment rebounding sharply, and month-end selling pressure increasingly in focus.

Energy and geopolitics also remained central to the tape. With the U.S.-Iran conflict still unresolved, crude moved back toward $100 as concerns built around physical shortages and broader energy disruption. The higher-yield backdrop partly reflected those worries, while the global policy backdrop grew a bit more restrictive after the Bank of Japan’s hawkish hold overnight. At the same time, the market is still looking ahead to a pivotal stretch of catalysts, including the FOMC decision, Q1 GDP, PCE inflation, and major Mag 7 earnings.

The economic data itself was mixed but generally resilient. Conference Board consumer confidence beat and reached its highest level since December, with both current conditions and expectations improving and inflation expectations cooling slightly. Housing data was softer, with both the Case-Shiller 20-city and FHFA house price indexes easing, while Richmond Fed manufacturing improved but missed expectations. Overall, the data still pointed to a relatively solid macro backdrop, even as energy costs and rates added pressure.

Sector Highlights

Sector performance showed a clear rotation away from the recent AI and growth leadership and toward more defensive and commodity-linked groups. Energy (+1.65%) led on the back of higher crude, while Real Estate (+0.99%), Consumer Staples (+0.99%), Health Care (+0.24%), Financials (+0.14%), and Utilities (+0.13%) also outperformed. The weakest groups were Technology (-1.29%), Materials (-1.07%), Industrials (-0.88%), and Consumer Discretionary (-0.68%). The pattern reinforced a market taking some money off the table in higher-beta growth after a strong run, while favoring defensives, energy, and selected value-oriented groups.

Information Technology

- SANM +14.6%: Fiscal Q2 revenue and EPS beat, driven by strength from ZT Systems; full-year guidance came in ahead of consensus and the company authorized a $600M buyback

- CVLT +10.6%: FQ4 revenue and EPS beat, with analysts encouraged by accelerating recurring revenue trends and a smooth CFO transition

- DT +1.1%: Starboard confirmed a top-five stake and argued the company is well positioned to benefit from enterprise AI adoption

- CLS -14.4%: Q1 EPS beat and guidance was raised, but the stock sold off against a very high bar after strong recent gains

- GLW -8.9%: Revenue beat, but free cash flow came in light and Q2 guidance was largely in line

- AMKR -5.7%: Beat on revenue, EPS, and gross margin, though the stock fell on elevated expectations and margin dilution concerns tied to Arizona ramp-up costs

- ORCL -4.1%: Weighed down with other OpenAI-linked names after the report on OpenAI missing internal growth targets

Communication Services

- SPOT -12.4%: Q1 operating income beat, but weaker advertising trends and a light Q2 operating income guide weighed on the shares

Consumer Discretionary

- PII +8.9%: Q1 revenue was slightly better and EBITDA/EPS beat by a wide margin; the company highlighted share gains and reaffirmed full-year guidance

- LGIH +8.0%: Big Q1 EPS beat, helped by higher average selling prices and better margins; raised full-year gross margin guidance

- GM +1.3%: Q1 EBIT beat by more than 40% and full-year EBIT guidance moved higher, helped in part by a tariff-related Supreme Court decision

- BBBY: Counted among the notable earnings gainers on the day

- LC: Also among the session’s earnings gainers

Consumer Staples

- KO +3.9%: Q1 EPS and revenue beat, with organic growth ahead of expectations and full-year EPS growth guidance raised

Health Care

- CNC +14.0%: Q1 adjusted EPS and revenue beat, helped by better Medicaid cost management and Medicare Advantage performance; raised full-year guidance

- OMCL +20.9%: Q1 EPS and revenue beat, with both product and service revenue ahead of consensus; raised FY26 adjusted EBITDA guidance

- AXGN +6.6%: Revenue beat and full-year revenue guidance came in above the Street

- ERAS -48.3%: Plunged after disclosing a patient death tied to ERAS-015, following a patent-related drop the prior day

- QGEN -10.7%: Negative Q1 revenue preannouncement tied to reduced immigration and softer U.S. life sciences demand

- ZBH -10.6%: Earnings and revenue beat, but investors focused on weaker knees results and a still-soft full-year revenue outlook

Industrials

- HRI +7.5%: Q1 revenue and EBITDA beat, with stronger equipment sales and signs of utilization stabilization; maintained full-year outlook

- NUE +4.7%: Q1 revenue beat by 7% and EBITDA came in 14% ahead; record steel-mill volumes and better pricing helped margins

- UPS -4.0%: Q1 revenue, operating profit, and EPS beat, but domestic margin remained soft and full-year guidance was only reaffirmed

- AWI -4.5%: Revenue was in line, but EBITDA and EPS missed as margin pressure persisted

- PNR -10.2%: EPS beat on stronger margins, but Q2 guidance was light and the full-year sales outlook was cut

- WSO -4.1%: Revenue and EPS beat, though investors focused on tariff uncertainty and volume outlook concerns

Energy

- SEI +5.4%: Q1 revenue and adjusted EBITDA beat; announced a 10-year hyperscaler contract for 600MW beginning in late 2026

Eco Data Releases | Wednesday April 29th, 2026

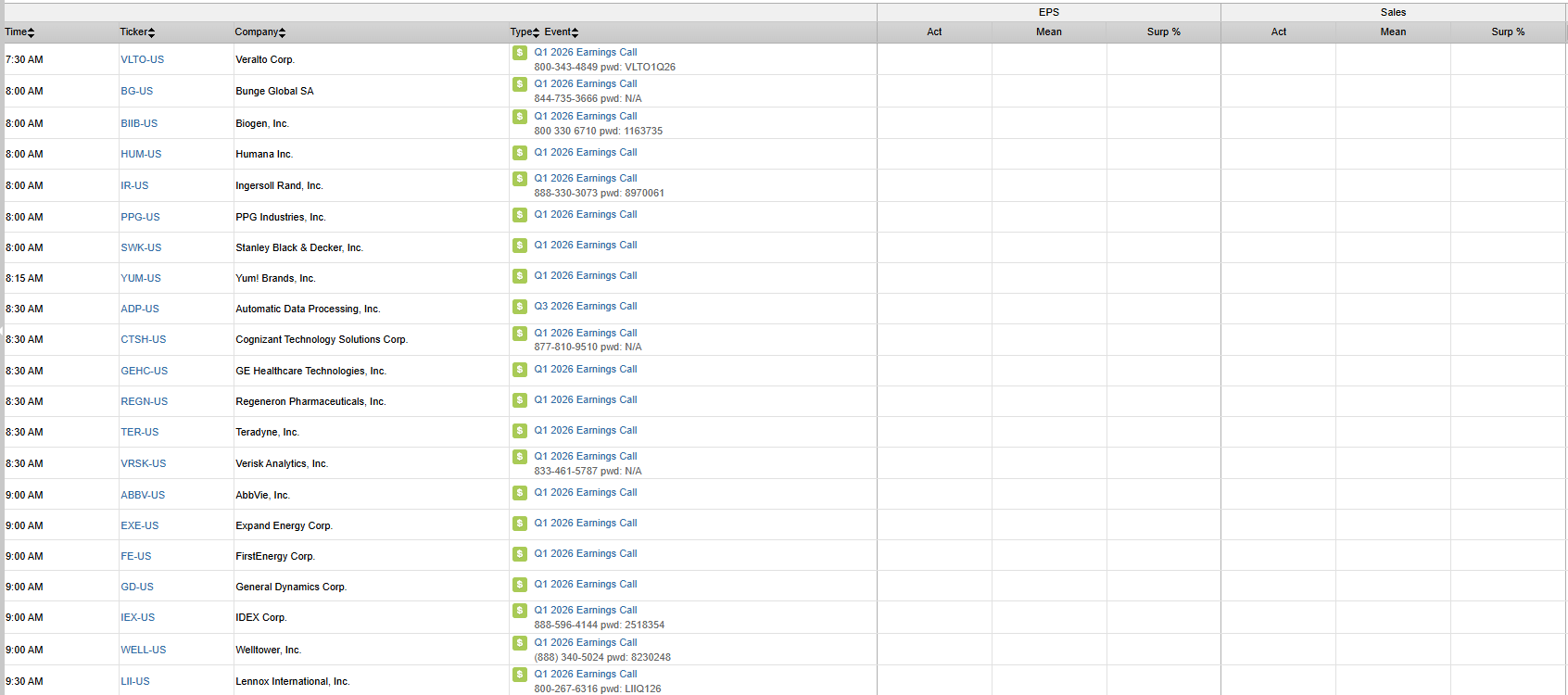

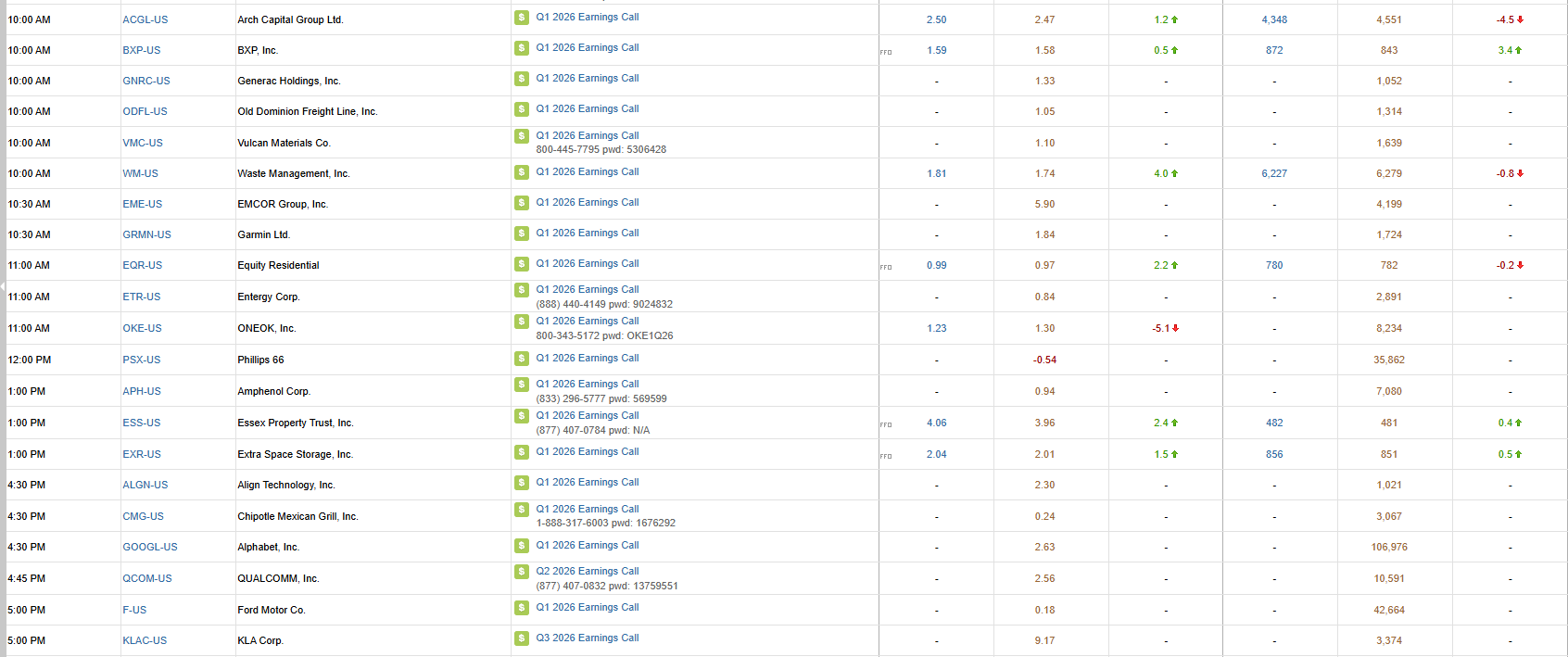

S&P 500 Constituent Earnings Announcements | Wednesday April 29th, 2026

Data sourced from FactSet Research Systems Inc.