S&P futures are up 0.6% Wednesday morning after Tuesday’s risk-on session, when the Nasdaq and Russell 2000 both gained more than 1%. Momentum leadership was the key story, with semis and memory outperforming alongside high-beta, retail-favorite, and most-shorted names. Global equities are stronger, with Hong Kong and China both up more than 1% and Europe up more than 2%. Treasuries are rallying, with yields down roughly 7 bp, the dollar is off 0.6%, gold is up 3.0%, silver is up 5.1%, Bitcoin futures are up 2.3%, and WTI crude is down 7.1% after already falling nearly 4% Tuesday.

The macro setup has improved as geopolitical risk appears to be easing. Trump said he is pausing Project Freedom amid progress in talks with Iran, Rubio said the U.S. has achieved its military objectives, and Axios reported the U.S. and Iran are nearing a one-page memo to end the war. Lower oil and lower yields are helping support equities and refocus investor attention on the dominant Q1 earnings theme: AI compute demand, hyperscaler capex, and momentum-factor leadership. April nonfarm payrolls on Friday remain the next major macro catalyst.

ADP private payrolls are due this morning, with consensus looking for a 120K April gain after 62K in March. Fed officials Musalem and Goolsbee speak today. Thursday brings Challenger layoffs, productivity and unit labor costs, initial claims, construction spending, and NY Fed inflation expectations. Friday’s employment report is the week’s key release, with consensus looking for 65K nonfarm payroll gains and unemployment unchanged at 4.3%.

Information Technology

- AMD: Beat and guided Q2 well above Street expectations despite a high bar, with Data Center the key growth driver.

- GOOGL: Anthropic reportedly committed to spend $200B on Google Cloud over the next five years.

- META: Reportedly planning an advanced agentic AI assistant for consumers.

- ANET: Q1 beat, but Q2 guidance was only in line as supply constraints weighed on the setup.

- LITE: Takeaways focused on strong optical demand, supply shortages, planned capacity expansion, and a high expectations bar.

- FLEX: Big gainer after Cloud & Power Infrastructure strength supported guidance; company also plans to spin off the segment.

- SMCI: Outperformed as a gross-margin-driven beat overshadowed a revenue miss.

- ALAB: Sharply higher after a strong beat-and-raise.

- KVYO: Down sharply on CFO exit and underwhelming Q2 revenue guidance.

- SWKS: Takeaways were mostly positive, though investors focused on input-cost pressure on gross margins.

Communication Services

- MTCH: Higher on better Tinder takeaways.

- META: Agentic AI assistant headlines reinforced the broader AI product-development narrative.

Healthcare

- DVA: Post-earnings standout.

- ALC: Post-earnings laggard.

Materials

- IFF: Post-earnings standout.

Energy

- OXY: Post-earnings laggard as crude sold off sharply.

Financials

- UPST: Post-earnings laggard.

U.S. equities finished higher Tuesday in a quieter session, with the Dow +0.73%, S&P 500 +0.81%, Nasdaq +1.03%, and Russell 2000 +1.75%. The macro tone improved as the U.S.-Iran ceasefire remained intact despite Monday’s flare-up, helping ease oil and rate pressure that had weighed on risk sentiment. WTI crude fell 3.6% to $102.59 after Monday’s rally, while Treasuries firmed across the curve, with the 2-year yield down 2 bp to 3.94%, the 10-year down 1 bp to 4.42%, and the 30-year down 3 bp to 4.99%. The dollar index rose 0.1%, gold gained 0.7%, and Bitcoin futures rose 2.0% back above $82K. Economic data were mixed but still broadly consistent with a stable macro backdrop: April ISM Services remained in expansion but came in light, with new orders down sharply, employment still in contraction, and prices paid elevated at the highest level since October 2022. March JOLTS openings of 6.866M were slightly ahead of estimates but down m/m and the lowest since December, while March new home sales rose to a stronger-than-expected 682K SAAR, the highest since December.

Sector Highlights

Sector performance was broadly positive and cyclically tilted. Materials led, up 1.67%, followed by Technology +1.63% and Industrials +0.86%, helped by semis, memory, E&C, chemicals, industrial metals, building products, trucking, and logistics. Consumer Staples gained 0.51%, Healthcare rose 0.38%, Consumer Discretionary and Communication Services each added 0.30%, Energy rose 0.14%, Real Estate gained 0.11%, and Financials and Utilities were nearly flat at +0.01%. The tape favored high beta, retail favorites, most-shorted names, AI infrastructure, semis, memory, and cyclicals, while energy, managed care, software, payments, exchanges, media, grocers, and entertainment lagged.

Information Technology

- INTC +13.0%: Rallied after Bloomberg reported Apple has held early talks with Intel and others as it explores processor supply alternatives beyond TSMC, reflecting supply-chain diversification concerns.

- DOCN +39.9%: Q1 revenue, margin, and adjusted EBITDA beat consensus; Q2 guidance was ahead, and 2026/2027 guidance was raised on strong customer demand and incremental committed capacity.

- PLTR -6.9%: Fell despite a big beat-and-raise, Rule of 40 score of 145%, AIP momentum, and strong U.S. government growth. Valuation and questions around commercial deceleration remained overhangs.

- SHOP -15.6%: Q1 revenue and free cash flow beat, with strong GMV and gross-profit growth, but Q2 guidance was only in line to slightly below consensus against high expectations and crowded positioning.

- FN -8.0%: Beat FQ3 earnings and revenue, with strong telecom revenue driven by data-center interconnect, but softer Datacom revenue, elevated expectations, and full valuation weighed on shares.

- LSCC -2.6%: Q1 earnings, EBITDA, and revenue beat; Q2 guidance was ahead. The company also announced a $1.65B cash-and-stock acquisition of AMI to expand its data-center offering.

- NOW: Projected better-than-expected subscription revenue of $30B by 2030, supported by AI product momentum.

Communication Services

- PINS +6.9%: Q1 revenue and adjusted EBITDA beat, with outperformance across geographies. Analysts were most positive on U.S. and Canada reacceleration, while guidance was better than feared.

- DUOL -5.6%: Q1 revenue, EBITDA, and DAUs beat, but shares fell on MAU deceleration, weaker Q2 bookings guidance, and FY bookings guidance being moved to the low end of the prior range.

- PSKY -4.3%: Q1 EBITDA and revenue beat, and Q2 EBITDA guidance was ahead, but revenue guidance was below Street and merger-related uncertainty remained an overhang.

- IAC -8.4%: Q1 EBITDA and revenue missed expectations, and FY26 EBITDA and operating-income guidance were cut.

Consumer Discretionary

- HOG +8.1%: Q1 revenue and operating income beat, EPS was in line, and FY26 guidance was reaffirmed. Management outlined its “Back to the Bricks” plan and targeted $350M+ EBITDA for 2027.

- LTH +11.8%: Q1 revenue, comps, and adjusted EBITDA beat, and FY26 guidance was raised. Memberships were slightly below expectations, but the company remains on track to open 12–14 new clubs this year.

- POOL: Announced a CEO transition.

- Honda: Reportedly canceling an $11B EV plant in Canada amid weaker demand.

- Ford: Said it is pushing ahead on EVs despite the broader industry pullback and is targeting EV breakeven by 2029.

Consumer Staples

- ADM +3.8%: Q1 EPS beat despite a revenue miss, and FY26 EPS guidance was raised. Management cited expected improvement in crushing and ethanol from renewable volume obligations, soy-crush pricing, and increased China trade.

- Beverages: Outperformed within Staples, while grocers lagged.

Energy

- FANG -3.5%: Q1 production, adjusted EBITDA, and capex were ahead of consensus, and revised 2026 guidance was better than expected. However, investors focused on changes to shareholder-return policy, including removal of the 50% FCF payout target and suspension of variable dividends.

- Energy sector +0.14%: Lagged the broader market as crude fell sharply on reduced escalation fears around the U.S.-Iran ceasefire.

Financials

- FIS: Higher after announcing a partnership with Anthropic to develop new AI tools for banks.

- FISV -8.8%: Q1 EPS beat but revenue missed, driven by Merchant Solutions weakness and a larger-than-expected organic-growth decline. Management reaffirmed FY26 EPS and organic-revenue guidance.

- COIN -2.6%: Announced a restructuring plan including a reduction of about 700 employees, or roughly 14% of its global workforce, with AI productivity cited as one driver.

- FDS -2.2%: Lower after Anthropic announced ten ready-to-run AI agents for financial-services firms and insurers.

- Payments / exchanges / credit cards: Underperformed despite the broader risk-on tape.

Healthcare

- WGS -49.2%: Q1 revenue and EPS missed, Q2 guidance was below consensus, and FY26 guidance was lowered, driven mainly by lower exome/genome ASPs and a reduced volume outlook.

- WAT +13.5%: Q1 revenue and EPS beat, with 13% organic growth. Biosciences and Diagnostic Solutions delivered $520M of post-acquisition revenue, $40M above guidance, and FY26 guidance was raised.

- INSP -12.0%: Q1 revenue, margins, and EPS beat, but FY26 guidance was cut sharply due to worse-than-expected I5 coding and WISeR impacts.

- EW: Announced a new CFO.

- Managed care: Lagged within Healthcare.

Industrials

- STRL +52.2%: Big Q1 earnings and revenue beat, driven by E-Infrastructure Solutions strength, CEC acquisition benefits, backlog momentum, and future phase opportunities. FY EPS guidance was raised by roughly 36%.

- CMI +2.8%: Q1 EBITDA beat by 6%, and 2026 sales and margin guidance was raised across key segments. Power Systems was the standout.

- TDG +3.6%: FQ2 earnings beat, revenue was in line, and FY guidance was raised on commercial aftermarket strength, higher commercial OEM build rates, and recent acquisitions.

- ETN -2.7%: Q1 EPS beat, and the low end of FY EPS guidance was raised, but Electrical Americas margins and a 50 bp cut to FY operating-margin guidance weighed on shares.

- FERG -3.1%: Q1 organic growth, revenue, and EBITDA beat, but shares fell on a high bar, soft residential end markets, and the stock’s strong YTD run.

- HII -10.3%: Q1 earnings and revenue beat, but Ingalls was weaker, and shares fell despite reaffirmed FY26 guidance and medium-term outlook.

- LDOS -7.8%: Q1 revenue and EPS beat and FY26 guidance was raised, but shares lagged despite strength in Intelligence/Digital, Health, and Homeland.

- KBR -5.4%: Q1 revenue and EPS beat, led by Mission Technology Solutions, but 2026 guidance was maintained and the planned spin was pushed to January.

Materials

- DD +8.4%: Q1 EBITDA beat by roughly 5%, and FY EBITDA guidance was raised. Healthcare was a standout, and pricing actions were highlighted as offsetting higher input costs tied to the Middle East conflict.

- GPK +12.2%: Q1 beat and 2026 guidance was reaffirmed. Investors focused on low expectations and cost-cutting actions already helping reshape the business.

- WLK -8.8%: Q1 EBITDA missed by roughly 28%, with higher natural gas prices, plant shutdowns, softer North American residential construction, and lower ASPs weighing on results.

- Chemicals / industrial metals / containerboard: Outperformed as Materials led the market.

Eco Data Releases | Wednesday May 6th, 2026

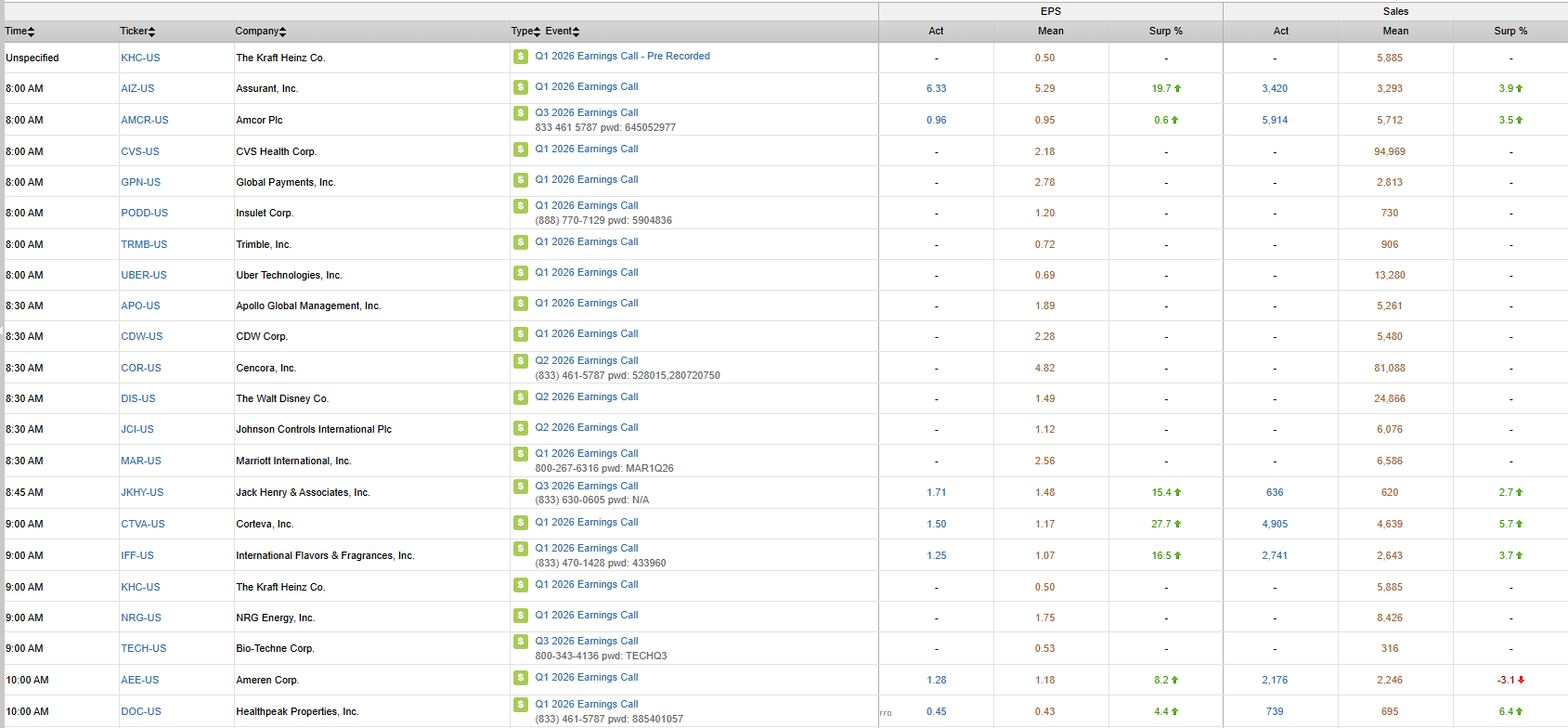

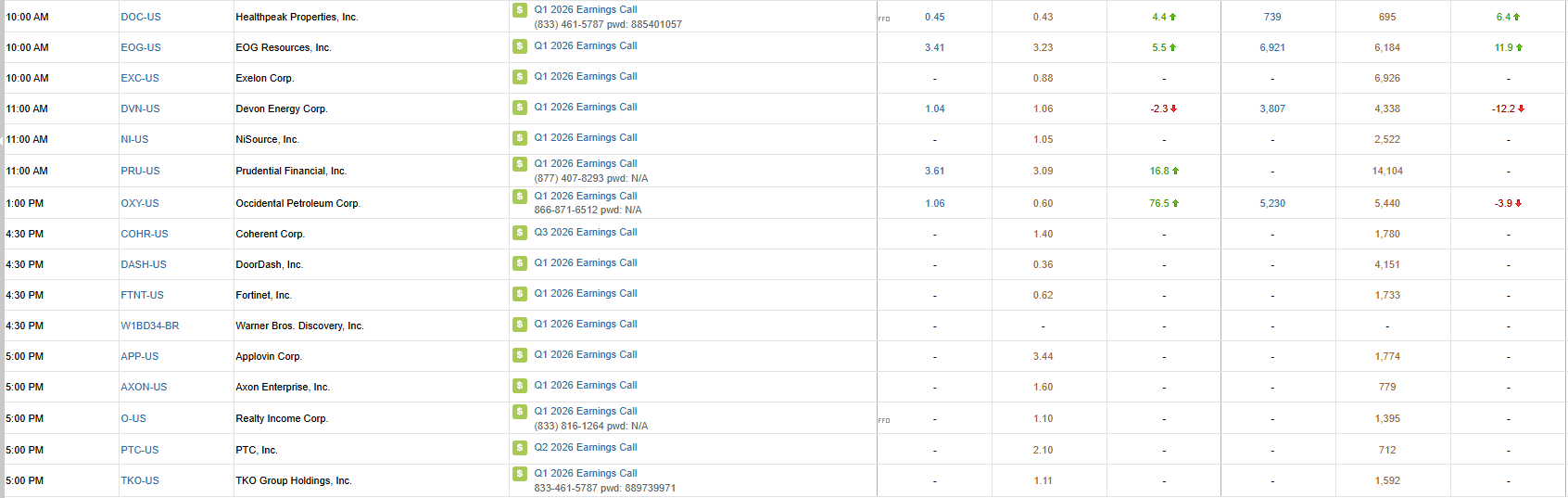

S&P 500 Constituent Earnings Announcements | Wednesday May 6th, 2026

Data sourced from FactSet Research Systems Inc.