S&P futures are up 0.1% Thursday morning after Wednesday’s broad rally, when all major U.S. indexes gained more than 1% and semis again led the tape. Big tech also finished higher, while internets, tech components, banks, machinery, electricals/multis, homebuilders, rails, cruise lines, airlines, apparel, and drug stores also outperformed. Global risk tone remains constructive, with Japan up more than 5.5% after returning from holiday and Hong Kong and South Korea up roughly 1.5%. Treasuries are firmer, with yields down about 2 bp after Wednesday’s larger rally, the dollar is slightly lower, gold is up 1.1%, Bitcoin futures are off 0.5%, and WTI crude is down another 2.6% after falling 7% Wednesday.

Today brings Challenger layoffs, productivity and unit labor costs, initial claims, construction spending, and NY Fed inflation expectations. Fed speakers include Kashkari, Hammack, and Williams. Friday’s employment report and University of Michigan sentiment/inflation expectations remain the key macro events, with consensus looking for roughly 65K April payroll gains and unemployment unchanged at 4.3%.

The macro setup remains centered on Iran de-escalation hopes, lower oil, and lower yields. Markets are waiting for Iran’s response to the latest U.S. proposal, and the lack of fresh escalation is being treated as a positive. The geopolitical reprieve is allowing investors to refocus on the strongest equity themes of recent weeks: AI compute demand, hyperscaler capex, semis, and strong Q1 earnings. However, scrutiny is building around how much of the AI tailwind is already priced into semis, along with rising AI-related input costs, including memory and token costs.

Information Technology

- ARM: Results and guidance were slightly better, but the stock faced a high bar after recent investor enthusiasm around AI and CPU demand.

- APP: Beat on gaming strength, with positive Street commentary around a more recent consumer ramp.

- COHR: Beat and raised guidance on data-center and communications strength, though supply constraints and elevated expectations remain in focus.

- FTNT: Strong gainer after a beat-and-raise, with AI, secured networking, and margin strength all viewed positively.

- FSLY: Big decliner as elevated expectations and a Network Services miss weighed on the stock.

Communication Services

- DASH: Higher on better Q2 GOV guidance and commentary that consumer demand remains strong.

- SNAP: Lower after ad revenue growth decelerated, with some Middle East impact, and the company said it no longer plans to launch its Perplexity partnership.

- ZG: Q2 EBITDA guidance came in light, pressured by legal costs and higher spending.

Consumer Discretionary

- FLUT: FY EBITDA guidance cut was better than feared.

- BROS: Beat and raised, though investors focused on Q2 comp-growth deceleration.

- WHR: Missed, sharply cut guidance, suspended its dividend, and cited a consumer-confidence hit from the Iran conflict.

Materials

- ALB: EBITDA came in ahead, with takeaways focused on strong price realization.

- CF: Beat expectations, helped by disruption in global nitrogen markets.

Industrials

- WTS: Beat on better sales and margins while maintaining guidance despite a dynamic macro backdrop.

- BLBD: Strong gainer after a beat-and-raise, with positive commentary around the Micro Bird acquisition and order intake.

U.S. equities finished higher Wednesday, ending near best levels, with the Dow +1.24%, S&P 500 +1.46%, Nasdaq +2.02%, and Russell 2000 +1.47%. The S&P 500 and Nasdaq both posted fresh record closes as geopolitical de-escalation hopes drove a sharp cross-asset risk-on move. Reports suggested the U.S. and Iran are working on a 14-point MOU that could frame the next round of talks, though Iran’s early response remained cautious and Trump continued to warn of renewed military action if no agreement is reached. Oil collapsed as de-escalation hopes built, with WTI crude down 7.1% to $95.06, while Treasuries rallied and yields fell 5–8 bp across the curve. The 2-year yield declined 7 bp to 3.87%, the 10-year fell 7 bp to 4.35%, and the 30-year declined 5 bp to 4.94%. The dollar index fell 0.4%, gold surged 3.0%, silver rose 5.1%, and Bitcoin futures slipped 0.2% after earlier gains. ADP private payrolls rose 109K in April, above the 99K consensus and the strongest reading since January 2025. Treasury’s quarterly refunding announcement was in line with expectations, with no change in auction sizes and $125B of refunding planned across 3-year, 10-year, and 30-year securities.

Sector Highlights

Sector performance was strongly risk-on but highly thematic. Industrials led, up 2.60%, followed by Technology +2.56%, Communication Services +2.05%, and Materials +1.88%, helped by AI infrastructure, semis, electricals, machinery, internets, and cyclicals. Consumer Discretionary rose 1.37%, Real Estate gained 1.35%, Financials added 0.50%, Staples rose 0.09%, and Healthcare edged up 0.08%. Energy was the clear laggard, down 4.07%, as crude prices plunged, while Utilities fell 1.45% as defensive yield proxies underperformed.

Information Technology

- AMD +18.6%: Q1 beat and Q2 guidance came in much stronger than expected, with Datacenter the key driver. Server CPU revenue rose 50% y/y in Q1, with guidance for more than 70% y/y growth, while the company doubled its 2030 server CPU TAM estimate to more than $120B.

- NVDA: Led big tech higher and announced a partnership with Corning tied to AI infrastructure. Nvidia also bought $500M of Corning shares.

- GLW +12.0%: Announced a partnership with Nvidia to expand U.S. manufacturing of optical connectivity solutions for AI data centers.

- FLEX +39.7%: Fiscal Q4 beat and FY27 guidance was well above consensus, driven by momentum in Cloud & Power Infrastructure. The company expects CPI revenue growth of 65–75% in FY27 and 80%+ in FY28 and plans to spin off the segment.

- SMCI +24.5%: Fiscal Q3 revenue missed, but EPS beat on stronger gross margins. Revenue was hurt by customer site-readiness delays and component shortages, while Q4 revenue guidance came in above expectations.

- ANET -13.6%: Q1 beat, but Q2 guidance was largely in line and supply constraints were a key headwind. Fundamentals remain tied to AI customer momentum, but the beat-and-guide failed to clear a high bar.

- SWKS -10.5%: FQ2 revenue and EPS beat, helped by Apple iPhone 17 strength, but margin scrutiny remained due to supply constraints and rising input costs.

- CDW -20.3%: Q1 earnings were in line and revenue beat, but margins missed, Government business declined, and Cloud customer spending slowed.

- KVYO -32.3%: Q1 beat and FY26 revenue-growth guidance was raised, but investors focused on a CFO transition, gross-margin pressure from carrier fees, and an underwhelming Q2 revenue guide.

Communication Services

- DIS +7.5%: Fiscal Q2 earnings and revenue beat, with better Entertainment results, SVOD monetization and volume growth, and strength in Experiences from admissions, food/beverage, and merchandise. FY adjusted EPS guidance was ahead of consensus.

- LYV +6.7%: Q1 revenue and operating income beat, with Concerts, Ticketing, and Sponsorships/Ads all ahead. Management said amphitheater demand remains robust and global touring supply is expanding.

- NYT +8.3%: Q1 earnings, revenue, and operating margin beat, helped by Subscription and Advertising strength, digital-only subscriber gains, and digital ARPU growth.

- META: Reportedly planning an advanced agentic AI assistant for consumers, reinforcing the broader AI product-development narrative.

- CPNG -13.8%: Q1 adjusted EBITDA missed as product-commerce growth slowed and customer-compensation costs weighed on results. Q2 guidance was below consensus.

Consumer Discretionary

- UBER +8.5%: Q1 revenue slightly missed, but bookings and adjusted EBITDA beat, led by Mobility. Mobility growth accelerated to 20%, Delivery was also healthy, and Q2 guidance came in ahead of consensus.

- JOBY +21.2%: Q1 EPS and revenue beat, though R&D expense was higher than expected. Analysts highlighted progress toward Type Certification and solid Blade performance.

- MAR: Notable post-earnings gainer.

- QSR: Notable post-earnings laggard.

- CART -8.1%: Q1 revenue, GTV, and EPS were in line, while adjusted EBITDA beat on stronger ad revenue. Order growth was slightly light and Q2 EBITDA guidance was modestly below consensus.

Consumer Staples

- KHC +2.4%: Q1 organic sales decline was much less than feared, gross margin and operating margin were better, EPS beat, and FY guidance was unchanged. Low expectations and elevated short interest helped the reaction.

Energy

- DVN -8.6%: Q1 was mostly in line, with lower capex offset by weaker commodity realizations and slightly higher operating costs. Oil production beat on Delaware Basin strength, though total production was slightly light.

- OXY: Post-earnings laggard as crude prices sold off sharply.

- Energy sector -4.07%: The weakest sector by far as WTI fell more than 7% on de-escalation hopes around the U.S.-Iran conflict.

Financials

- UPST -7.9%: Q1 revenue beat, but EBITDA missed. Investors focused on margin pressure tied to front-loaded investments, seasonality, and mix shift, though volumes remained strong.

- Financial data: Underperformed, while broader Financials were positive but lagged the market’s AI- and cyclically led advance.

Healthcare

- CVS +7.7%: Q1 earnings and revenue beat, helped by Health Care Benefits strength, better MBR and membership metrics, government-business support, and stronger pharmacy comps. FY guidance was raised.

- DVA +23.5%: Q1 earnings and revenue beat, with strength in treatment volume, revenue per treatment, and cost per treatment. FY guidance was raised, and the stock was upgraded at Deutsche Bank.

- JAZZ +7.7%: Q1 earnings and revenue beat, with Neuroscience strength from Xywav and Epidiolex and Zepzelca standing out in Oncology. FY guidance was reaffirmed.

- NVO +2.0%: Q1 sales, EBIT, and EPS beat, helped by positive Wegovy trends. FY26 guidance was raised, driven by stronger expected U.S. GLP-1 demand.

- PODD -9.7%: Q1 revenue and EPS beat on continued Omnipod strength, and FY26 revenue growth guidance was raised, but gross margin came in slightly below consensus.

- COR -17.4%: Fiscal Q2 earnings and revenue missed, with U.S. Healthcare below consensus. FY revenue growth guidance was trimmed, though FY EPS midpoint was raised.

- ALC -11.7%: Q1 sales growth missed, with Surgical and Implantables a drag. EPS beat and guidance was raised, but competition and softer market trends weighed.

Industrials

- ITT +1.9%: Q1 organic growth, revenue, EBIT, and sales all beat, with strength in Flow Technologies, 33% Aerospace growth, share gains, and broad-based order growth.

- PRIM -50.1%: Q1 revenue and EPS missed, and FY26 guidance was lowered. Management cited cost pressures on renewables projects and slower-than-expected project starts.

- JCI: Notable post-earnings laggard.

- J -7.3%: FQ2 revenue and adjusted EPS beat, but operating profit missed. Management cited strong infrastructure, advanced facilities, and data-center demand, and raised FY26 guidance.

Materials

- IFF: Post-earnings standout.

- CC -15.3%: Q1 EBITDA beat, helped by TiO2 and refrigerants, but Q2 EBITDA guidance was below consensus amid APM polymer softness. Shares also faced pressure from lower oil and chemical pricing tied to easing Iran tensions.

- CTVA -2.5%: Q1 earnings and revenue beat across Seed and Crop Protection, but FY guidance was only reaffirmed. Management said agricultural fundamentals remain mixed.

- Commodity and ag chemicals: Underperformed even as the broader Materials sector gained.

Real Estate

- Real Estate +1.35%: Benefited from lower yields and the broader risk-on tape, though no major company-specific catalyst was highlighted.

Utilities

- Utilities -1.45%: Lagged as investors rotated away from defensives and into AI infrastructure, semis, industrial cyclicals, and higher-beta areas.

Eco Data Releases | Thursday May 7th, 2026

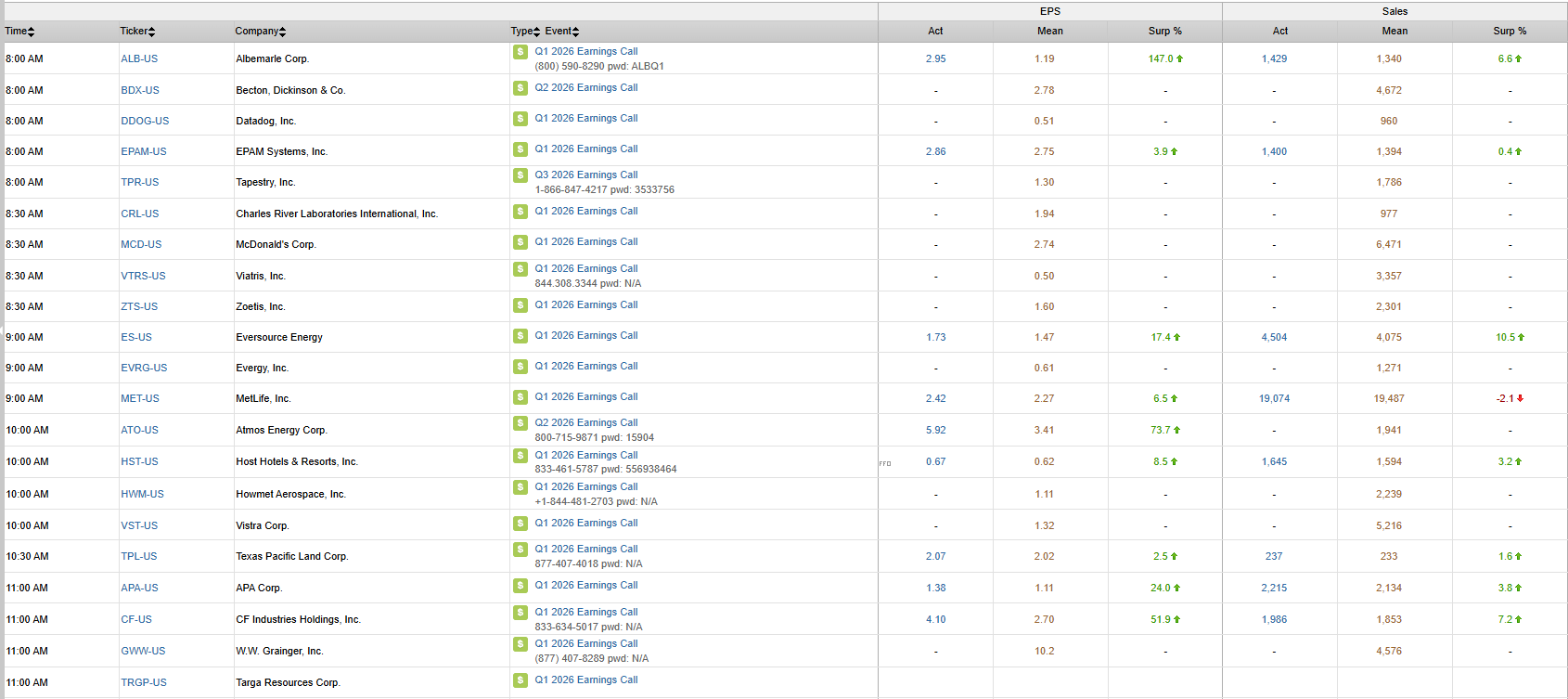

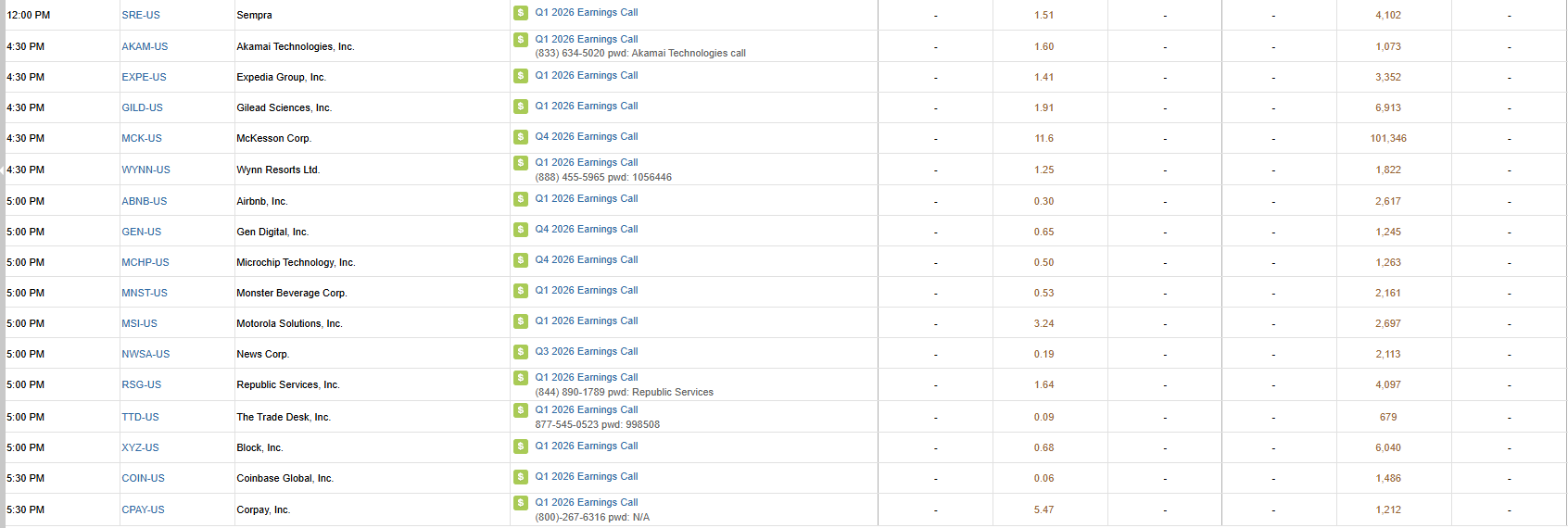

S&P 500 Constituent Earnings Announcements | Thursday May 7th, 2026

Data sourced from FactSet Research Systems Inc.