April 30, 2025

Markets remain in a holding pattern ahead of key Mag 7 earnings and a heavy macro calendar. Supportive factors include improving earnings (particularly around tariff mitigation), some easing in Fed expectations, and recent tariff relief headlines. However, trade-related growth risks remain significant, especially amid delays in striking multiple trade deals. Concerns about Fed independence persist, with Trump renewing criticism of Powell.

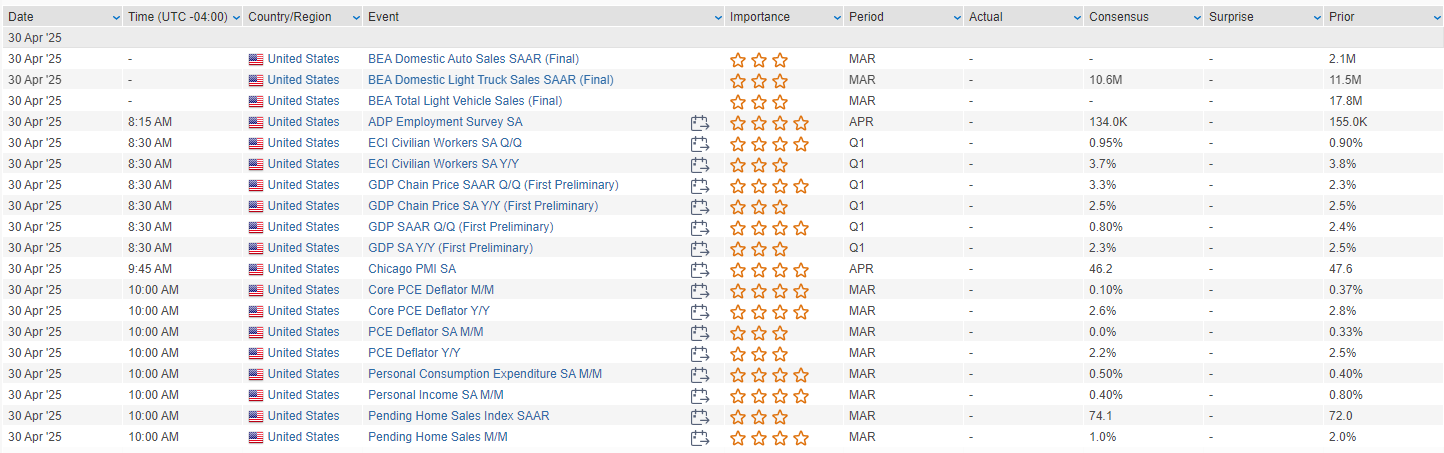

Today’s macro focus includes April ADP payrolls, Q1 GDP (with import-related drag), Q1 ECI, PCE inflation, personal income/spending, Chicago PMI, and pending home sales. Thursday features ISM manufacturing, jobless claims, and vehicle sales. Friday brings the April jobs report, with expectations for ~130K in payroll gains and stable 4.2% unemployment.

Corporate Highlights

- V beat and reaffirmed guidance; said consumer spending is holding up.

- BKNG Q1 strong but trimmed 2025 cc guidance; flagged macro uncertainty.

- SBUX missed and suggested a longer turnaround is needed, though some progress noted.

- MDLZ reiterated FY guidance despite cocoa price pressures.

- PPG beat and maintained outlook; demand remains solid.

- SMCI dropped on a negative preannouncement citing delayed customer decisions.

- STX rallied on margin-driven beat and improving visibility.

- SNAP tumbled after avoiding formal Q2 guidance due to macro uncertainty.

- FSLR missed and cut FY outlook on tariff-related impacts.

- CZR beat slightly; highlighted strong ops and balance sheet.

- FLS noted continued strength in Power segment bookings.

- QRVO beat and raised; upbeat content commentary.

- TENB fell sharply after cutting FY guidance, citing weaker federal business.

- WERN missed, pressured by higher costs and softer volumes.

U.S. equities ended higher on Tuesday (Dow +0.75%, S&P 500 +0.58%, Nasdaq +0.55%, Russell 2000 +0.56%), near session highs, with the S&P 500 extending its longest winning streak of the year to six days. Breadth was positive and leadership came from financials, materials, and consumer staples, while energy lagged despite falling oil prices. Treasury yields fell 3–5 basis points with some curve flattening, and the 10Y yield declined for the sixth straight day. The dollar index rose 0.3%, gold was down 0.4%, and WTI crude dropped 2.6%, settling just above $60 per barrel.

Macro sentiment improved on confirmation of tariff relief for the auto sector, with the White House announcing that automakers will be spared from “stacked” tariffs and allowed some offsets for foreign-made parts. Commerce Secretary Lutnick said a trade deal had been reached with at least one unnamed country and emphasized efforts to reward U.S. production. Still, there were no signs of thawing in U.S.-China relations.

Economic data was mixed. April Consumer Confidence fell to 86.0, the lowest since Spring 2020, while the Expectations Index plunged to levels not seen since 2011. JOLTS job openings fell to 7.2M, below expectations, reflecting slower hiring momentum. The labor market differential narrowed as more consumers viewed jobs as hard to get. Meanwhile, home price data came in modestly above consensus.

The market remains in wait-and-see mode ahead of a busy stretch of macro releases, including Q1 GDP, core PCE inflation, ADP private payrolls (Wednesday), ISM manufacturing (Thursday), and nonfarm payrolls (Friday). The Street expects April job growth of ~130K and flat unemployment at 4.2%.

S&P 500 Sector Performance

- Outperformers: Financials (+0.97%), Materials (+0.92%), Consumer Staples (+0.77%), Real Estate (+0.74%), Utilities (+0.70%), Industrials (+0.64%), Consumer Discretionary (+0.59%)

- Underperformers: Energy (−0.37%), Technology (+0.46%), Healthcare (+0.49%), Communication Services (+0.50%)

Company-Specific News by Sector

Information Technology

- CDNS: Q1 EPS beat, revenue in line. Raised FY guidance; noted strength across segments but remained cautious on China.

- HON: Q1 beat on revenue, EPS, and organic growth; raised lower end of EPS guidance and included tariff mitigation in updated outlook.

- ZBRA: Q1 beat and raised FY EPS outlook. Revenue guidance unchanged, but margins lowered due to tariff costs.

- NXPI: Q1 in line; Q2 guide slightly better. Auto/Industrial segments light, margins and CEO retirement noted as overhangs.

- PYPL: Q1 beat on EPS but revenue missed. Mixed TPV trends; Venmo grew 9.6% y/y. FY EPS guidance unchanged.

- SANM: Q2 beat, but Q3 guide light. Customers adjusting inventories amid geopolitical shifts.

Communication Services

- SPOT: Q1 revenue in line, but operating margin missed. Subscriber growth solid, but ARPU and premium revenue disappointed.

- META: Launched new standalone AI app as competition with OpenAI intensifies.

Consumer Discretionary

- AMZN: Criticized by White House over rumored plan to display tariff costs, which the company denied.

- HLT: Q1 beat, but cut FY RevPAR and EBITDA guidance due to macro uncertainty.

- JBLU: Q1 beat; 2Q RASM guidance soft. Passenger revenues fell 4.2%, but Loyalty and International segments noted as strengths.

- EAT: Q1 beat and raised FY guide, but stock fell on high expectations following YTD rally.

- SPGI: Q1 beat with strength in Ratings and Commodity Insights. Announced Mobility unit spin-off and $650M buyback.

Consumer Staples

- KO: Organic sales growth ahead of expectations; maintained FY guidance.

- PEP: Cut FY guide. KO outperformed on relative execution.

- KHC: Cut FY guide; widely expected reset amid policy-driven uncertainty.

- SHW: Q1 beat on EBITDA and EPS; reaffirmed FY guidance despite weaker commercial demand.

Industrials

- UPS: Q1 beat; announced 20,000 job cuts citing trade-related headwinds.

- WWD: Q2 beat and raised FY guidance. Aerospace aftermarket strong; OEM and defense soft.

- CR: Q1 beat, FY guidance reaffirmed. UBS upgrade highlighted long-term optimism and M&A potential.

- NE: Q1 EBITDA beat; reiterated full-year guide. 15 rig-years of backlog added.

- PCAR: Q1 miss on both Truck and Parts. Market cautious on demand trends.

Financials

- WFC: Announced $40B buyback program.

- SOFI: Q1 beat; raised FY guidance. Total accounts up 5% y/y.

- BKU: Q1 beat helped by lower provisions, but fee income and NII missed. Loan attrition flagged.

Healthcare

- PFE: Q1 sales slightly light, EPS helped by expense control.

- REGN: Q1 miss with softness in Eylea and Libtayo; competitive pressure cited.

- THC: Q1 beat and raised FY EPS. Hospital and Ambulatory segments strong; expense control also noted.

- ADMA: FDA approval for yield-enhancement process lifted shares.

- HIMS: Surged after announcing Wegovy distribution partnership with NVO.

Real Estate

- SBAC: Improved U.S. activity noted; raised FY guide and launched $1.5B buyback.

Materials

- CCK: Big Q1 beat, raised FY guidance. Strong volumes in Brazil and Europe; well-positioned on tariffs.

- LGIH: Q1 beat, but cut FY gross margin due to tariff-related supplier cost increases.

Energy

- BP: Q1 net profit dropped 48%, missed estimates. Strategy chief departing; cash flow in line.

Eco Data Releases | Wednesday April 30th, 2025

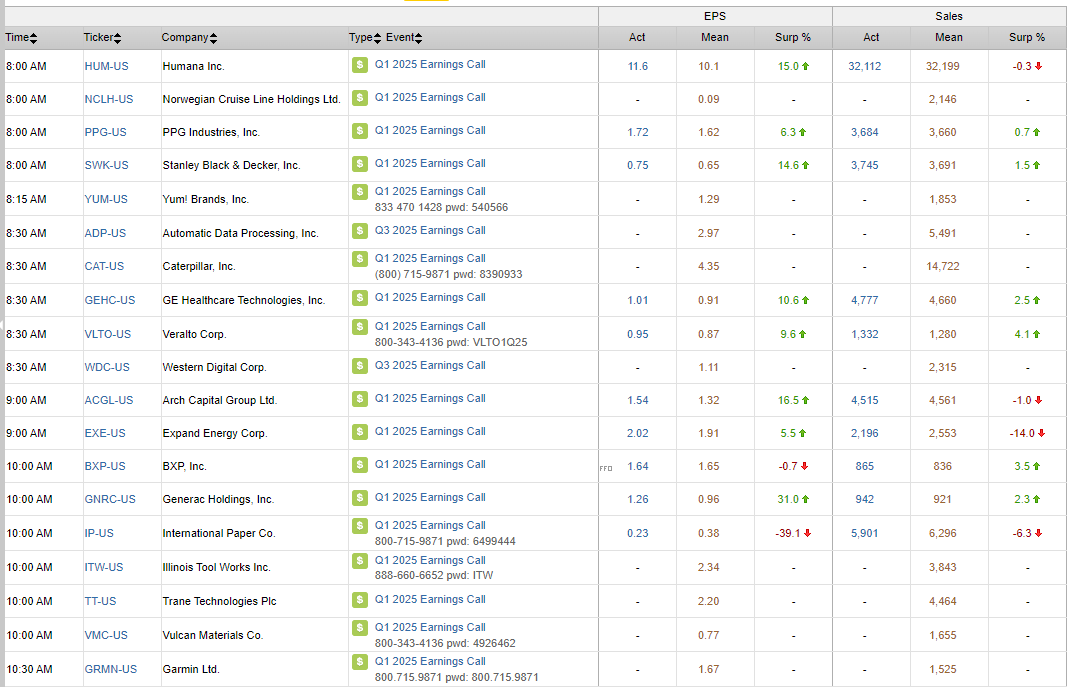

S&P 500 Constituent Earnings Announcements | Wednesday April 30th, 2025

Data sourced from FactSet Research Systems Inc.