May 15, 2025

S&P futures are down 0.5% Thursday morning, following mixed U.S. equity performance on Wednesday. Big tech and semis outperformed, while defensives and healthcare lagged. Asian markets traded mostly lower overnight, with Japan and Greater China notable laggards. European markets are also down ~0.5%. Treasuries are firmer, with yields lower by 2-3 bps. The dollar index is down 0.3%. Bitcoin futures declined 1.9%, while WTI crude fell 4%, driven by potential progress on a U.S.-Iran nuclear deal.

Key Developments:

- Trade talks between the U.S. and China continued in South Korea. Trump hinted at a U.S.-India tariff deal and agreed to intensified U.S.-EU negotiations.

- Trump claimed progress toward a U.S.-Iran nuclear agreement.

- In Washington, House Republicans continue to debate the reconciliation bill, focusing on SALT cap and Medicaid cuts.

Economic Data:

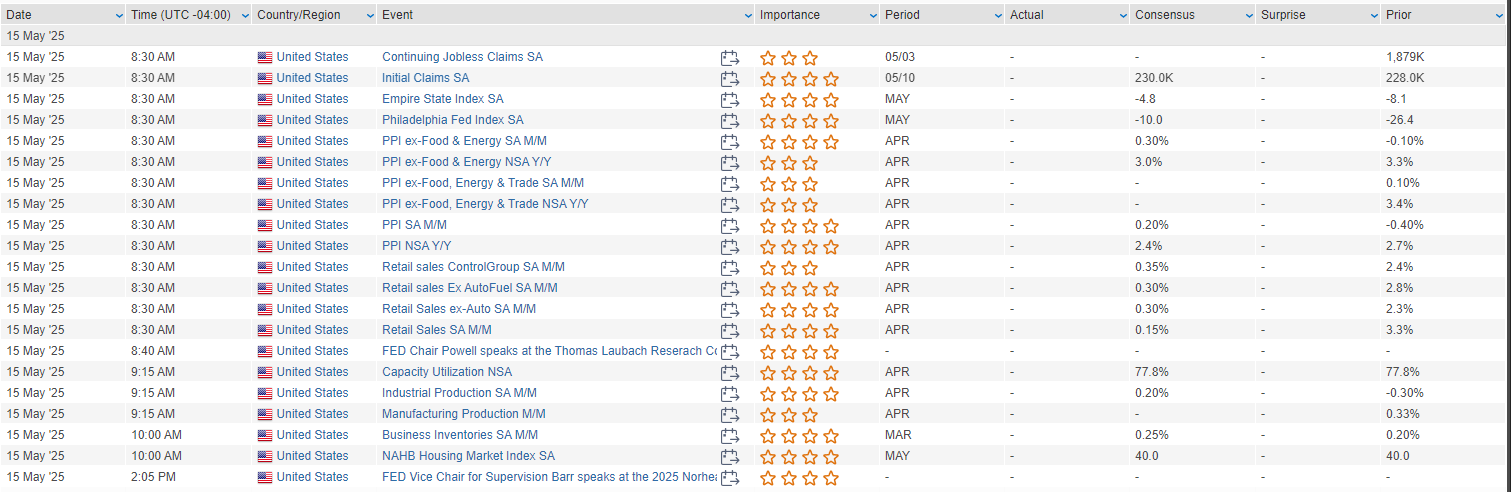

Thursday brings a busy U.S. calendar with Empire Manufacturing, retail sales, PPI, industrial production, and homebuilder sentiment. Retail sales will be closely watched, given the divergence between resilient data and soft sentiment. Fed Chair Powell speaks on the central bank’s monetary policy framework.

Corporate News:

- Earnings: Alibaba missed on fiscal Q4 revenue and EPS. Cisco beat on fiscal Q3 revenue and EPS, highlighting AI momentum. Deere beat and maintained FY guidance. Birkenstock exceeded estimates, citing potential tariff-driven consumer shifts.

- Other Headlines: Trump urged Apple to relocate production from India to the U.S. Nvidia may get U.S. approval to ship 500K AI chips annually to the UAE. UNH faces a criminal probe into Medicare fraud. Starbucks is reportedly considering selling its China business. Dick’s Sporting Goods confirmed a $2.4B acquisition of Foot Locker

U.S. equities closed mixed on Wednesday, with the S&P 500 holding onto a modest year-to-date gain and extending its rebound to over 18% from the YTD low on April 8. The Nasdaq notched its sixth straight session of gains, buoyed by strength in megacap tech stocks like Alphabet, Nvidia, and Tesla, which offset weaker breadth across the broader market. Equal-weight indices underperformed their cap-weighted counterparts, reflecting the continued dominance of large-cap names in driving market performance.

Treasuries ended weaker across the curve, with yields rising as the bond market priced in a slightly steeper curve. This shift suggests diminished recession fears, aligning with easing trade tensions and stronger sentiment in certain economic sectors. The dollar index recovered from earlier losses, ending the day up 0.1%, supported by reports of potential trade deals between the U.S. and Asian partners, though skepticism about broader trade agreements lingers.

In commodities, gold fell sharply, losing 1.8% and closing below $3200/oz for the first time since April 10, as rising real yields and a stronger dollar weighed on demand. Oil prices also softened, with WTI crude declining 0.8%, reflecting continued uncertainty about global supply-demand dynamics. Bitcoin futures followed the broader risk-off tone, sliding 1.4% on the day.

Trade developments remained a focal point, as reports suggested that Japan and South Korea were nearing agreements with the U.S., while Canada and China announced pauses in retaliatory measures. Despite these positive signals, concerns about the sustainability of these moves and the broader implications for U.S.-China trade relations tempered optimism.

On the policy front, Federal Reserve commentary offered limited new insights. Fed Governor Jefferson highlighted the potential for tariffs to slow economic growth and raise inflation but expressed confidence in the Fed’s ability to manage these challenges. Daly and Waller also spoke, but their remarks focused on less market-sensitive topics. Markets adjusted their expectations for rate cuts, now pricing in less than 50bps of easing for the year.

Looking ahead, a heavy economic calendar on Thursday includes Empire Manufacturing, retail sales, industrial production, and housing data, all of which will provide fresh insights into the state of the U.S. economy. Fed Chair Powell’s scheduled remarks on the central bank’s monetary policy framework are also anticipated, while housing starts, import/export prices, and consumer sentiment data will close out the week.

Sector Performance:

- Top Performers: Communication Services (+1.58%), Technology (+0.96%), Consumer Discretionary (+0.38%).

- Lagging Sectors: Healthcare (-2.31%), Materials (-0.96%), Real Estate (-0.90%)

Corporate Highlights:

Consumer Discretionary:

- PVH Corp (+8.4%): Upgraded to “Buy” at Jefferies, citing new initiatives expected to drive sales growth.

- American Eagle Outfitters (-6.4%): Preliminary Q1 results missed on operating income due to elevated promotions and a $75M inventory write-down. The company withdrew FY25 guidance citing macro uncertainty.

Technology:

- Advanced Micro Devices (+4.7%): Announced a $6B share repurchase program, highlighting confidence in long-term growth.

- Super Micro Computer (+15.7%): Secured a $20B contract with Saudi Arabian datacenter company DataVolt for high-performance GPU platforms.

- Dynatrace (+5.9%): FQ4 results exceeded expectations, with broad-based growth in AI-native software driving 15% y/y ARR growth.

Healthcare:

- Exelixis (+20.8%): Strong Q1 results driven by Cabometyx’s market share gains, leading to raised FY25 guidance.

- GRAIL (-23.3%): Missed Q1 revenue and EBITDA targets but noted commercial progress with Galleri and extended cash runway into 2028.

- Alcon (-6.1%): Q1 revenue and EPS fell short, pressured by U.S. implantable device weakness amid competitive and market headwinds.

Industrials:

- Everus Construction Group (+17.3%): Beat Q1 earnings expectations on improving backlogs in data center and hospitality projects.

- Boeing: Benefited from a $96B Qatar Airways deal for up to 210 aircraft, boosting sentiment around its commercial aerospace recovery.

Financials:

- KKR (+1.7%): Upgraded to “Overweight” by Morgan Stanley on expectations that tariff de-escalation could catalyze private market activity.

Communication Services:

- Warner Bros.: Rebranding its streaming service back to “HBO Max” in a strategic move to bolster brand recognition.

Materials:

- MP Materials (+1.5%): Partnered with Saudi Arabian Mining Company to explore a fully integrated rare-earth supply chain, aligning with global decarbonization efforts.

Energy:

- WTI Crude (-0.8%): Continued to face downward pressure amid demand uncertainties and global supply negotiations.

Eco Data Releases | Thursday May 15th, 2025

S&P 500 Constituent Earnings Announcements | Thursday May 15th, 2025

Data sourced from FactSet Research Systems Inc.