ETFsector.com Daily Trading Outlook, August 12, 2024

Equities closed the week on a positive note with the major US indices notching gains. The Nasdaq continued to retrace recent declines adding 0.51% while the S&P 500 was up 0.47% and the Dow 0.13%. XLC paced the sector SPDR’s adding 0.85% While XLB was the laggard sector and the only negative on the day dropping 0.08%.

The VIX retreated to the 20 level while interest rates were mixed with the Yield on the 2yr moving higher to 4.05% while the 10yr saw its Yield drop to 3,939%. Commodities prices were marginally higher.

All in all, we need to see more to feel the worst is behind us looking at the market. We expect a risk off tone to predominate in the near-term. The earnings and economic calendars are light on Monday and we are in peak vacation season through Labor Day.

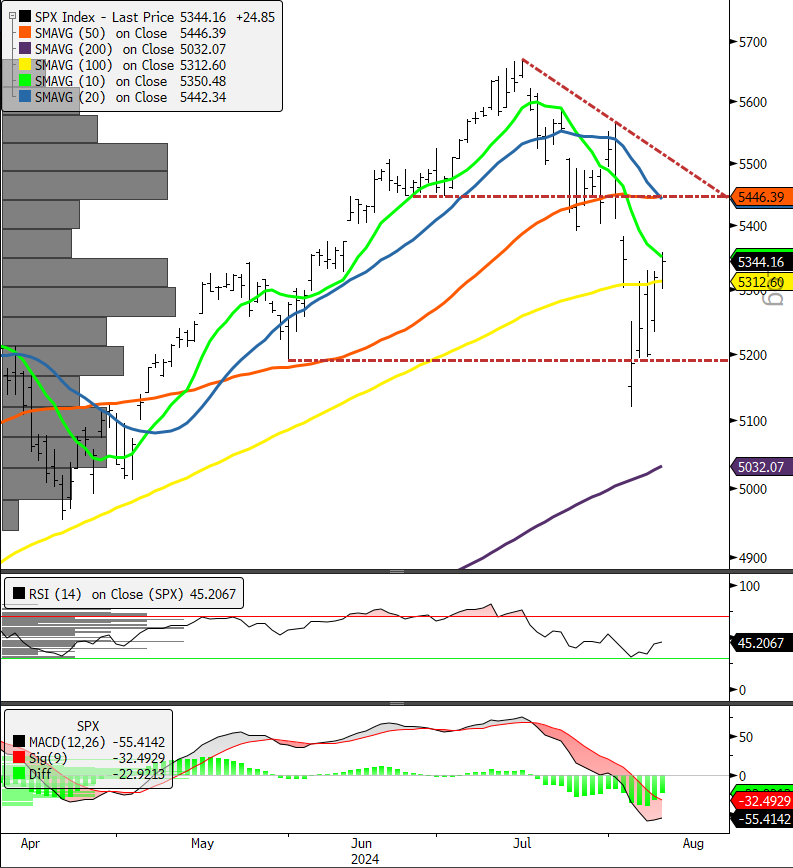

Correction Watch: Price Still Below Key Resistance

Friday’s price action was short of a material bullish reversal, and we would need to see prices move above the 5450-5500 range to feel confident betting on upside. The S&P 500 YTD chart below shows the price congestion zone at that level which is the near-term point of control on the chart. On the other hand, a move below 5200 would signify more technical damage.

- S&P 500 daily, YTD (RSI | MACD)

- Price is short of congestion and the MACD oscillator is still short of a pivot buy signal. Remain cautious for now

Eco Data Releases | Monday August 12th, 2024

| Date Time | Event | Survey | Actual | Prior | Revised | |

| 08/12/2024 11:00 | NY Fed 1-Yr Inflation Expectations | Jul | — | — | 3.02% | — |

| 08/12/2024 14:00 | Monthly Budget Statement | Jul | -$242.0b | — | -$66.0b | — |

S&P 500 Constituent Earnings Announcements by GICS Sector | Monday August 12th, 2024

No S&P 500 Constituent Earnings Releases on Monday

Momentum Monday

We take a look at Homebuilders in today’s feature. A positive re-rate from more dovish interest rate expectations is getting priced in. Near-term the chart is overbought. Homebuilders have been one of the areas of strength underpinning the bull. Housing shortage is a secular tailwind to builders while higher rates represent a potential headwind. It will be interesting to see if the Consumer can stay above water given that prices still seem fairly high despite the fact the growth rate is slowing.

- S&P 500 Homebuilders Industry (200-day moving average | RSI | Relative to S&P 500 )

- Just below the Mag7, Homebuilders have been one of the strongest momentum plays of the cycle and a boon to XLY. Unfortunately they are tactically vulnerable, rolling over from overbought conditions

Sources: Bloomberg