Equities capped a strong weak with gains on Friday as the Dow paced the major indices, adding 0.24% while the Nasdaq was up 0.21% and the S&P 500 0.20%. The weekly gain was the best for the S&P 500 this year as recession fears fade in light of a slew of data that has threaded the needle between recessionary and inflationary. This keeps investors on expectation of rate cuts as soon as September.

At the sector level, Financials led the tape, along with Utilities, Comm Servies and Staples. Industrials were the laggard with Energy and Real Estate sectors also finishing in the red on the day.

WTI Crude retreated to $76.51, and Commodities prices generally traded weaker. While interest rates also moved lower with the 10yr down to 3.88% and the 2yr at 4.049%.

International stocks closed mixed with the MSCI EAFE Index adding 0.31% and the EM Index off 0.20%. International stocks continue to lag domestic over longer timeframes in this bull market.

Futures as of this writing are up a tick for the S&P 500 and the Nasdaq. If we see more buying on Monday through resistance, we will be triggering short covering in some of our higher beta positions.

Eco Data Releases | Monday August 19th, 2024

No Releases Today

S&P 500 Constituent Earnings Announcements by GICS Sector | Monday August 19th, 2024

No S&P 500 Constituents report Today

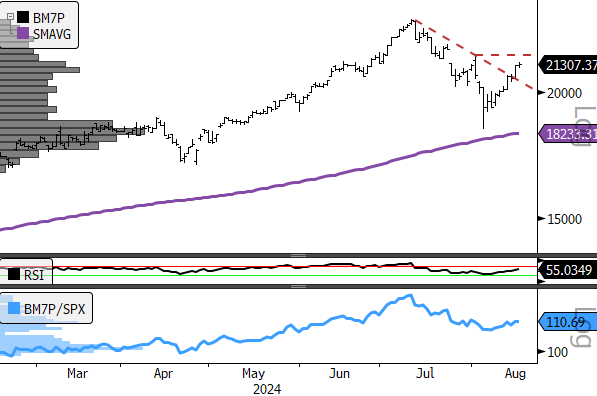

Momentum Monday

Checking in on the Mag7, we can see the recent rally is nearing overhead resistance. Mag7 outperformance has been a hallmark of this bull trend going back to January 2023. The recent spike in RSI momentum is a longer-term bullish sign. How the cohort does facing near-term resistance going into this week will be an important check for potential thematic leadership.

- Bloomberg Mag7 Price Index (200-day m.a. | RSI | Relative to S&P 500)