S&P futures up 0.2% Thursday morning after US equities finished higher Wednesday, led by AI plays, banks, pharma, utilities, and REITs. Asian markets mostly higher with China and Hong Kong up over 1%, while European markets rallied ~0.8%. Treasuries weaker with curve flattening, dollar index up 0.4%, gold down 0.4%, Bitcoin futures up 2.2%, and WTI crude rising 0.9%.

Little new on tariffs, with markets awaiting the Trump-Xi call. Focus remains on Trump 2.0 policy uncertainty, as the Senate plans a reconciliation bill excluding taxes. Treasury Secretary Bessent emphasized efforts to lower 10-year yields rather than the Fed funds rate, citing energy price relief and government efficiency. Earnings were mixed, with notable disappointments in tech, healthcare, and auto. Retail buying remains strong, supporting bullish sentiment.

US economic data includes jobless claims (expected at 213K vs. 207K prior) and productivity/unit labor costs. Fed Governor Waller speaks at 14:30 ET on global finance. Nonfarm payrolls (Friday) forecast at +170K for January (vs. +256K prior), with unemployment steady at 4.1% and hourly earnings up 0.3% m/m.

Sector and Company News

Information Technology

- Qualcomm (QCOM): Beat expectations but raised concerns over pull-in effects and Huawei licensing.

- Arm Holdings (ARM): In-line guide underwhelmed, citing slower v9 adoption.

- Cognizant (CTSH): Beat estimates, but organic growth guidance was light.

- Symbotic (SYM): Fell sharply on weak fiscal Q2 guidance.

- Skyworks (SWKS): Dropped on weaker iPhone 17 content guidance.

- Coherent (COHR): Highlighted AI-driven data center demand.

- FormFactor (FORM): Reported soft demand in high-volume markets.

- TTM Technologies (TTMI): Beat and raised guidance, citing Gen AI demand.

- Impinj (PI): Declined on excess inventory concerns.

Consumer Discretionary

- O’Reilly (ORLY): Strong comps but EBIT light at midpoint.

- Ford (F): Missed 2025 EBIT guidance.

Healthcare

- Becton Dickinson (BDX): Plans to separate Biosciences and Diagnostic Solutions businesses.

- McKesson (MCK): Strong pharma performance but Med/Surg remained soft.

- Molina Healthcare (MOH): Missed on higher medical loss ratio.

- Align Technology (ALGN): Weak FY25 guide on FX headwinds.

Financials

- MetLife (MET): Issued light guidance.

- Allstate (ALL): Beat on better combined ratio and investment income.

Materials

- Corteva (CTVA): Guidance better than feared.

- Crown Holdings (CCK): Beat expectations, citing shipment increases.

US equities ended higher on Wednesday, with the major indices finishing at their best levels of the day. Market breadth was positive, and the equal-weight S&P 500 outperformed, though mixed performances among mega-cap technology stocks weighed on broader gains. Treasuries saw notable firming, leading to curve flattening, with 10-year yields nearing 4.40%, their lowest level since mid-December. The US dollar index declined by 0.3%, with yen strength driven by firmer wage data in Japan being a major FX development. Gold advanced by 0.6%, while Bitcoin futures declined 1.5%. WTI crude oil fell by 2.3%.

Key macroeconomic data included the January ADP private payrolls report, which exceeded expectations at 183K (vs. 150K consensus) and was revised upward from 122K to 176K for December. The ISM Services Index came in softer than expected at 52.8 (vs. 54.0 consensus), with new orders falling to their lowest level since June. However, employment ticked higher while prices paid declined. Additionally, the US Treasury’s quarterly refunding statement was in line with expectations, leaving auction sizes unchanged for three-, ten-, and 30-year securities. Federal Reserve commentary highlighted ongoing concerns around tariffs and economic uncertainty, with policymakers leaning towards rate cuts in 2025 while maintaining a cautious stance.

In Washington, policy uncertainty increased with reports that tax measures may be omitted from an initial GOP reconciliation package. Government shutdown fears also grew. On the trade front, the US Postal Service reversed its temporary suspension of parcels from China and Hong Kong, causing confusion among importers. Additionally, Chipotle’s CFO indicated that the company is not planning near-term price hikes despite potential tariff impacts. ByteDance reportedly may allow TikTok’s US operations to shut down rather than agree to a forced sale.

Sector and Company News

Information Technology

- Alphabet (GOOGL): Shares declined following earnings, with concerns over a slowdown in Cloud growth and a significant increase in capital expenditures for AI infrastructure ($75B projected for 2025, a 40%+ YoY rise). However, Google Search and YouTube revenue remained strong.

- Nvidia (NVDA): Stock rose on continued AI investment optimism, with Google announcing plans to run its first customer workloads on Nvidia’s Blackwell chips.

- Advanced Micro Devices (AMD): Fell on disappointing data center results, despite overall Q4 results meeting expectations and a strong client segment.

- Cirrus Logic (CRUS): Advanced due to better-than-expected iPhone demand and a favorable mix toward higher-end models.

- Super Micro Computer (SMCI): Gained following the announcement of full production availability for Nvidia’s Blackwell Rack-Scale Solutions.

Financials

- Banks and credit card firms were among the market’s outperformers.

- Fiserv (FI): Stock gained after posting better-than-expected Q4 earnings, driven by strong Clover revenue growth.

- Workday (WDAY): Announced a restructuring plan involving layoffs of ~8.5% of its workforce to improve profitability, boosting shares.

Consumer Discretionary

- Chipotle Mexican Grill (CMG): Declined after reporting softer-than-expected comp growth and light guidance, though management expects a second-half acceleration.

- Harley-Davidson (HOG): Fell on weak FY25 guidance, citing cyclical headwinds.

- Columbia Sportswear (COLM): Dropped after missing earnings expectations and issuing weak FY25 guidance.

- Mattel (MAT): Surged after beating earnings and providing strong FY25 guidance, despite factoring in tariff headwinds.

- Electronic Arts (EA): Gained after announcing a $1B stock repurchase program and expectations for a return to net booking growth in FY26.

- Match Group (MTCH): Declined after issuing weak Q1 and FY25 guidance, with a CEO change announced.

- Uber Technologies (UBER): Fell on light bookings guidance despite Q4 revenue and EBITDA beating expectations.

Industrials

- Old Dominion Freight Line (ODFL): Rose on Q4 earnings and revenue beats, though management flagged ongoing softness in the domestic market.

- Timken (TKR): Advanced following a Q4 EPS beat and cost-reduction plans for 2025.

Healthcare

- Amgen (AMGN): Issued guidance in line with expectations, though a clinical hold for its obesity drug raised concerns.

- Novo Nordisk (NVO): Gained following strong Q4 results, with Ozempic and Wegovy sales largely in line with expectations.

- Bio-Techne (TECH): Advanced after posting strong earnings, supported by solid growth in protein sciences and diagnostics.

Real Estate

- Real Estate Investment Trusts (REITs) performed well as lower Treasury yields improved sentiment.

Consumer Staples

- Mondelez (MDLZ): Dropped after missing organic growth expectations, with cocoa prices highlighted as a key concern.

- Reynolds Consumer Products (REYN): Declined after issuing weak FY25 sales and EBITDA guidance.

Energy & Materials

- FMC Corp (FMC): Plunged after issuing weak Q1 and FY25 guidance, citing pricing pressure and cautious purchasing trends.

Communication Services

- Snap (SNAP): Declined despite strong Q4 earnings, as guidance pointed to an investment-heavy period weighing on EBITDA.

- Disney (DIS): Rose post-earnings despite warning of a Q2 decline in Disney+ subscriptions.

Eco Data Releases | Thursday February 6th, 2025

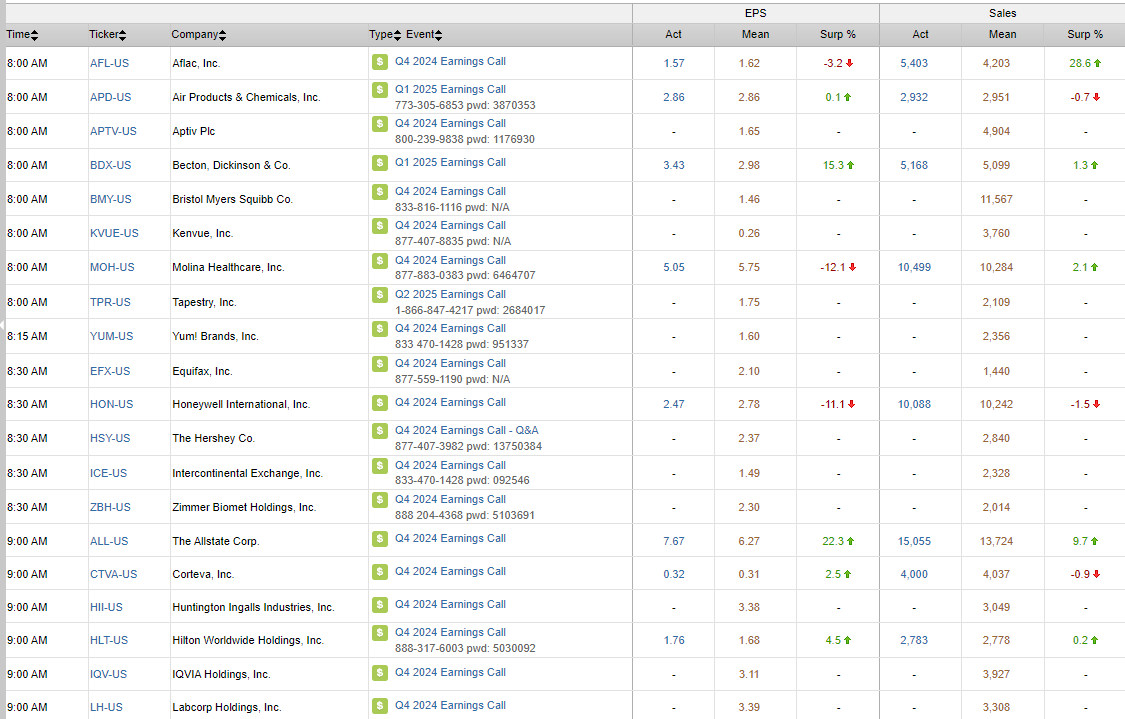

S&P 500 Constituent Earnings Announcements | Thursday February 6th, 2025

Data sourced from FactSet Research Systems Inc.