ETFsector.com Daily Trading Outlook, July 15, 2024

Buyers stepped in on Friday with the major large cap. indices all higher. The S&P 500 added 0.55% while the Dow was up 0.62% and the Nasdaq gained 0.63% to close the week. The Yield on the US 10yr Treasury closed lower at 4.18%. At the sector level XLC continued to lag, while XLY, XLB and XLK led the sectors higher on the day. Lower interest rates continued to boost laggard areas of the market and breadth improved as measured by the NYSE cumulative advance/decline line.

The small cap. Russell 2000 surged 1.09% while Crude moved lower on the day and broad commodities were flat. Developed market shares traded in line with the US, but EM shares showed weakness.

Light economics calendar on Monday with Empire Manufacturing data the sole release. GS and BLK continue Financial Sector releases as Q3 earnings season continues.

Eco Data Releases | Monday July 15th, 2024

| Date Time | Event | Survey | Actual | Prior | Revised | |

| 07/15/2024 08:30 | Empire Manufacturing | Jul | -8 | — | -6 | — |

S&P 500 Constituent Earnings Announcements by GICS Sector | Monday July 15th, 2024

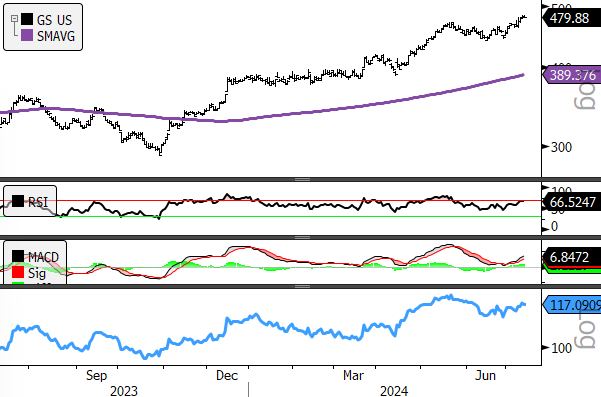

GS will be an interesting one to watch this quarter as the stock has been one of the few steady outperformers outside of the Mag7 in 2024, outperforming the S&P 500 buy >17% over that time period. If our XLC sell is triggered this week (as we discuss in our weekly market letter), XLF would likely receive some of the allocation on recent improvement.

- Goldman Sachs 1yr, daily (200-day m.a.)

- RSI

- MACD

- Relative to S&P 500

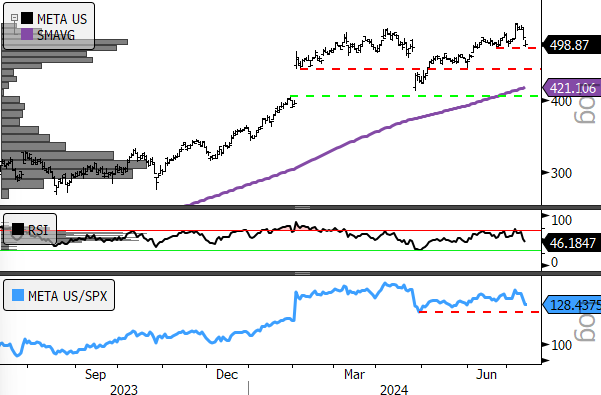

Momentum Monday: Gut-check time for META

Thursday’s reversal in big Tech was pervasive up and down the market cap. tiers as Value surged vs. Growth in each cohort.

- META, 1yr, daily (200-day m.a.) Tactical sell gets triggered at $487, potential downside near $400

- Panel2: RSI—showing a negative divergence

- Panel 3: Relative to S&P 500—near support, April low is important for the chart

Sources: Bloomberg