US equities capitulated to the downside on Thursday with all three of the major large cap. benchmarks posting losses along with the Russell 2000 Small Cap. Index which fell 1.85% after a week of strong gains. The Dow finished the session off 1.29% while the S&P 500 and the Nasdaq Composite finished down 0.78% and 0.70% respectively.

At the sector level, Healthcare shares led large cap’s lower with the XLV giving up 2.27% followed by selling in the XLF (-1.21%) and XLY (-1.02%). On the positive side, XLE led sectors adding 0.18%, while the XLK which had its largest single day drawdown of 2024 on Wednesday added 1 basis point in the session.

DHI delivered a strong quarter, delivering more homes than expected. But, while shares jumped >10% on the result, enthusiasm was tempered by weaker forward guidance. In general, the selling was attributed to profit taking and political uncertainty as investors had been rotating away from Mega Cap. Growers into other sectors, but on Thursday started cashing out entirely. As a result, the VIX (CBOE volatility index) was up 10% on the day to a reading of 15.

Yields on the 2yr and 10yr treasury bonds rose to 4.47% and 4.2% respectively while the Dollar strengthened vs. the major developed market crosses and Crude and Commodities finished weaker.

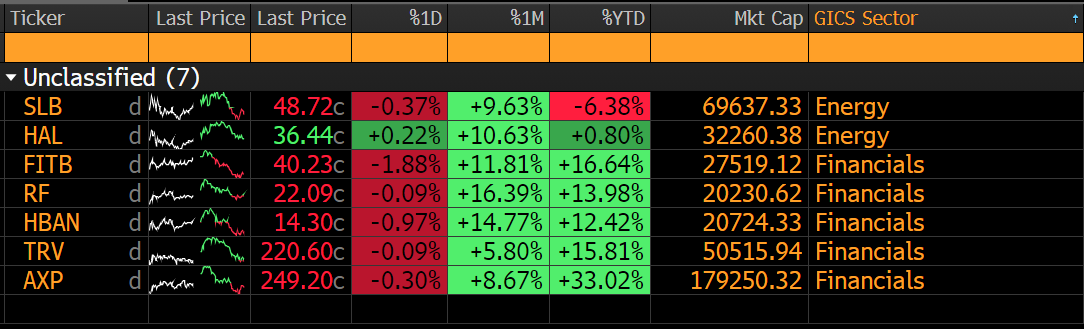

Energy services majors HAL and SLB report earnings on Friday along with several regional banks, TRV and AXP.

Eco Data Releases | Friday July 19th, 2024

No Economic Releases Today

S&P 500 Constituent Earnings Announcements by GICS Sector | Friday July 19th, 2024

Friday’s earnings slate will give investors a chance to evaluate some very economically sensitive co.’s in AXP, SLB and HAL. Those results and any guidance will be interesting data points as the market searches for direction amid profit taking.

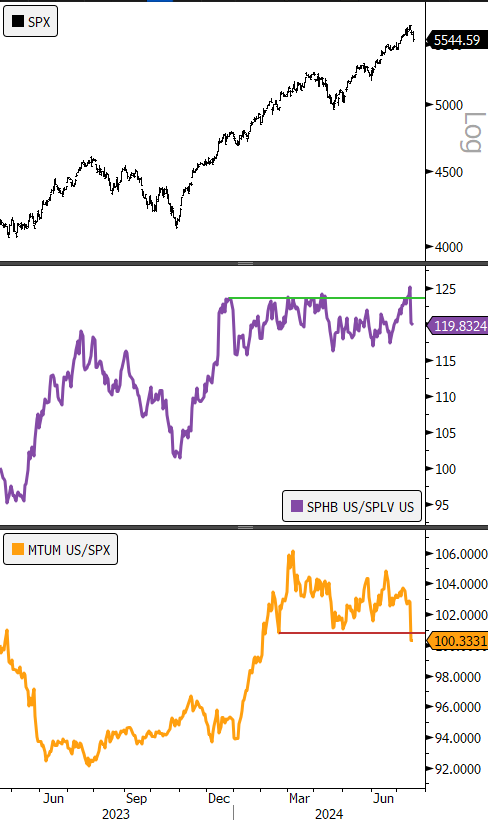

Factor Friday: Momentum Breaking Down

Since February of 2024 the relative performance of the iShares Momentum Factor ETF has been in consolidation vs. the S&P 500, while the Invesco S&P High Beta ETF has been in a stalemate measured against the Invesco Low Vol. ETF. We are now seeing potential movement in each series with MTUM breaking down and SPHB (at least initially) breaking out to the upside against SPLV. These will be crucial gages to watch in the near-term as the market could potentially correct lower into the election.

- Panel 1: S&P 500

- Panel 2: Invesco S&P High Beat ETF Relative to Invesco S&P Low Vol. ETF

- Panel 3: iShares Momentum ETF Relative to S&P 500

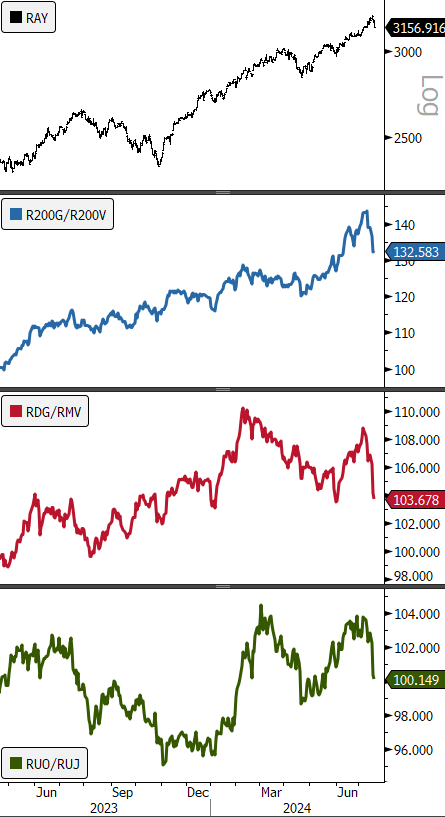

While high-beta and low vol. factors remain at loggerheads over the intermediate-term, we can see in the chart below that the near-term rotation in the market clearly favors Value. We are of the opinion that Growth isn’t done yet from a long-term perspective, but when Value is still a material underperformer vs. Growth over multiple longer timeframes.

- Panel 1: Russell 3000

- Panel 2: Russell Mega Cap. Growth vs. Russell Mega Cap. Value

- Panel 3: Russell Mid-Cap. Growth vs. Russell Mid-Cap. Value

- Panel 4: Russell 2000 Growth vs. Russell 2000 Value

Sources: Bloomberg