Soft earnings reports from Mag7 members GOOGL and TSLA led to the S&P 500 to trade off 2.31% snapping an impressive streak without a decline of more than 2%. The Nasdaq was down 3.64% and the Dow declined 1.25%. At the Sector level, the XLK Technology ETF led SPDR’s lower down more than 4%, ending the day as a YTD laggard. Rotation away from Mag7 heavy sectors XLC, XLK and XLY have picked up in the past two weeks as earnings have failed to clear lofty expectations.

Market internals were negative at 3:1 decliners:advancers among S&P 500 constituents, but shy of full capitulation. Nonetheless the unwind of Mega Cap. Growth leadership has been very sharp, which is more indicative of a buyable correction than a market top.

The yield on the 2-yr treasury note ended the session at 4.4% while the 10yr finished at 4.26%. Crude and commodities prices were slightly softer.

Jobless Claims, Continuing Claims and Core PCE highlight the economic calendar for Thursday, while there is also another robust slate of earnings releases. ABBV and big industrials HON, RTX and UNP highlight the names reporting.

Eco Data Releases | Thursday July 25th, 2024

| Date Time | Event | Survey | Actual | Prior | Revised | |

| 07/25/2024 08:30 | GDP Annualized QoQ | 2Q A | 2.00% | — | 1.40% | — |

| 07/25/2024 08:30 | Personal Consumption | 2Q A | 2.00% | — | 1.50% | — |

| 07/25/2024 08:30 | GDP Price Index | 2Q A | 2.60% | — | 3.10% | — |

| 07/25/2024 08:30 | Core PCE Price Index QoQ | 2Q A | 2.70% | — | 3.70% | — |

| 07/25/2024 08:30 | Initial Jobless Claims | 20-Jul | 238k | — | 243k | — |

| 07/25/2024 08:30 | Continuing Claims | 13-Jul | 1868k | — | 1867k | — |

| 07/25/2024 08:30 | Durable Goods Orders | Jun P | 0.30% | — | 0.10% | — |

| 07/25/2024 08:30 | Durables Ex Transportation | Jun P | 0.20% | — | -0.10% | — |

| 07/25/2024 08:30 | Cap Goods Orders Nondef Ex Air | Jun P | 0.20% | — | -0.60% | — |

| 07/25/2024 08:30 | Cap Goods Ship Nondef Ex Air | Jun P | 0.20% | — | -0.60% | — |

| 07/25/2024 11:00 | Kansas City Fed Manf. Activity | Jul | -5 | — | -8 | — |

S&P 500 Constituent Earnings Announcements by GICS Sector | Thursday July 25th, 2024

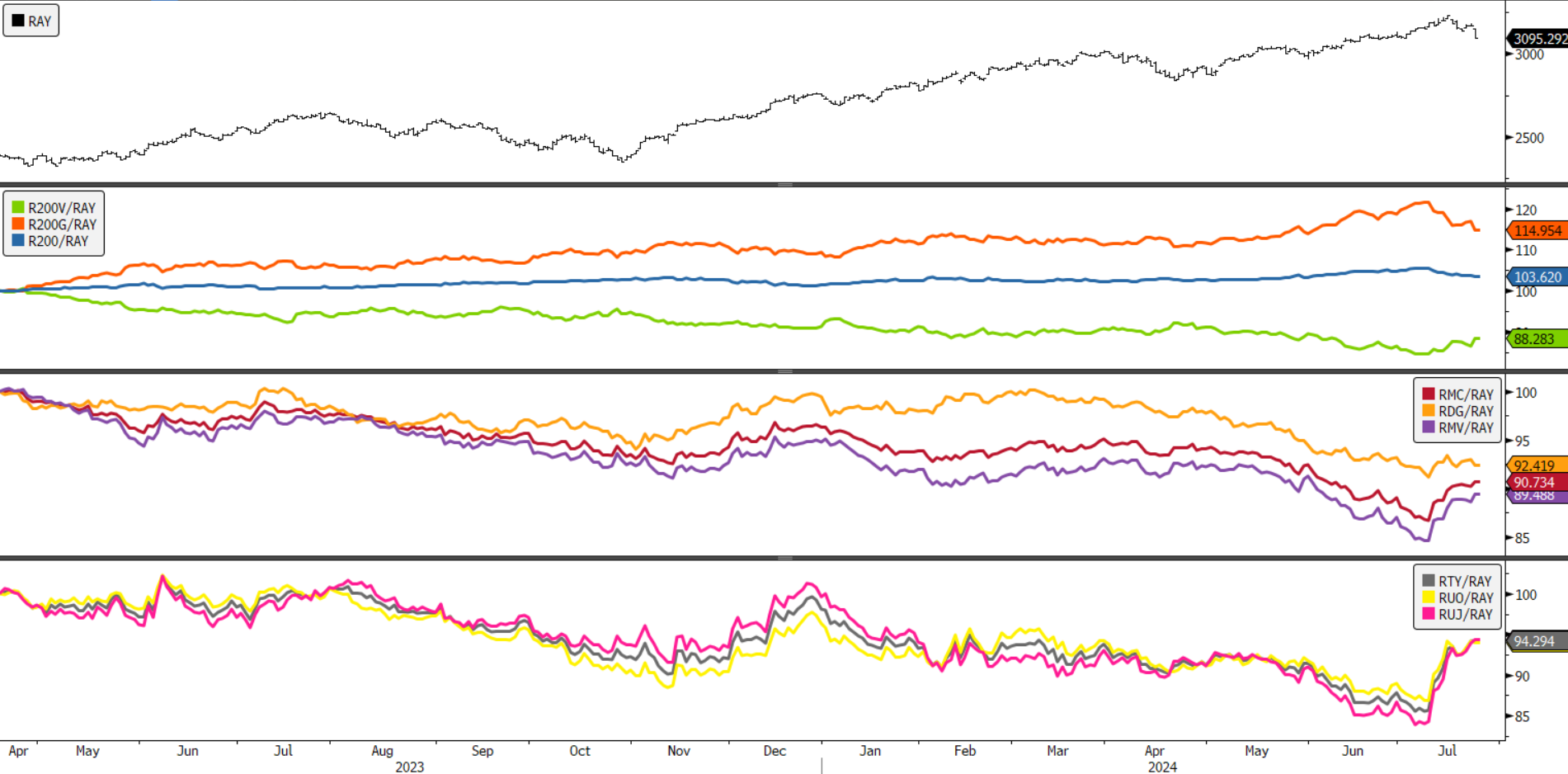

With a wide mix of names reporting, we will see if the preference for min. vol. stocks continues. Likely it will be directionally dependent on the broad market. We are at the seasonally weak period of the year with equities sitting on double-digit returns. Potentially a correction that precedes opportunity.

Thematic Thursday

The theme of the past two weeks has been clear, it’s all Value and Small/Mid-Cap. at the expense of Mega Cap. and Growth. The Russell 2K has reclaimed performance across all styles, but Mid Value and Mega Value are clear winners.

- RAY 1yr, daily

- Panel 2: Russell Mega Cap Growth / Value

- Panel 3: Russell Mid Cap Growth / Value

- Panel 4: Russell 2000 Growth / Value

Source: Bloomberg