Another record day for the Nasdaq (+0.34%) and the S&P 500 (+0.23%) as AVGO shares spiked 12.3% on a strong beat and raise. The XLI (-0.6%) led economically sensitive shares lower with the Dow off 0.11%. That matched the broad tenor of the market as the near-term rally has been almost entirely Tech driven. NVDA closed up 3.5%.

At the macro level, the 10yr Treasury Yields moved lower to 4.24% and is at its lowest level since late March. WTI Crude fell to $77.80 a barrel and appears to be rolling over below its 200-day m.a. and the Bloomberg Commodities index was also lower finishing off 0.53%.

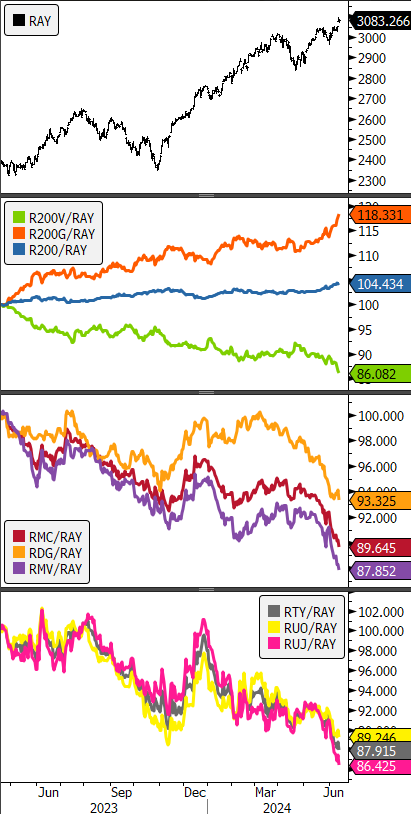

The macro picture underpins a growing disconnect between the index level trends for equities and the breadth beneath the surface. Leadership is becoming narrow. This is likely unsustainable for the bull market without some signs of broadening participation. In the near-term lower rates is enough to motivate investors into equity, but a slowing economy could override that enthusiasm if evidence of stagnation mounts. In the mean-time Mega Cap. Growth is the clear leading factor behind outperformance.

Eco Data Releases | Friday June 14th, 2024

| Date Time | Event | Survey | Actual | Prior | Revised | |

| 06/14/2024 08:30 | Import Price Index MoM | May | -0.10% | — | 0.90% | — |

| 06/14/2024 08:30 | Import Price Index ex Petroleum MoM | May | 0.20% | — | 0.70% | — |

| 06/14/2024 08:30 | Import Price Index YoY | May | 1.30% | — | 1.10% | — |

| 06/14/2024 08:30 | Export Price Index MoM | May | 0.10% | — | 0.50% | — |

| 06/14/2024 08:30 | Export Price Index YoY | May | 0.60% | — | -1.00% | — |

| 06/14/2024 10:00 | U. of Mich. Sentiment | Jun P | 72 | — | 69.1 | — |

| 06/14/2024 10:00 | U. of Mich. Current Conditions | Jun P | 72.2 | — | 69.6 | — |

| 06/14/2024 10:00 | U. of Mich. Expectations | Jun P | 72 | — | 68.8 | — |

| 06/14/2024 10:00 | U. of Mich. 1 Yr Inflation | Jun P | 3.20% | — | 3.30% | — |

| 06/14/2024 10:00 | U. of Mich. 5-10 Yr Inflation | Jun P | 3.00% | — | 3.00% | — |

S&P 500 Constituent Earnings Announcements by GICS Sector | Friday June 14th, 2024

No S&P 500 Constituents Reporting

ADBE beat after the bell on both the top and bottom-line which lines up with strong results from ORCL and ADSK and could spark some rotation into Software names. The macro environment and the leadership trend is lined up behind Tech. and Growth with mega caps front and center.

Factor Friday

I dream of the day when there will be some mystery and skill behind which factors one ought to be exposed to. It used to be fun to pick between low vol., high-beta, momentum, value, out of favor, dividend yield…alas, there is only one factor that is mattering to the market at present. Are you big? Are you Growth? The rest, for now, can hang. Keep the XLK and XLC longs, but we need some clue on what’s next. Absent any segment of the market raising its hand, you eventually want some oversold defense in the portfolio and XLP and XLV are currently fitting that profile.

- Russell 3000 Index

- Panel 2: Mega Cap. | Mega Cap. Growth |Mega Cap. Value

- Panel 3: Mid Cap. | Mid Cap. Growth| Mid Cap. Value

- Panel 4: Small Cap. | Small Cap. Growth |Small Cap. Value

Sources: Bloomberg