S&P Futures Down 0.1%:

S&P futures are down 0.1% in Friday morning trading after US equities closed higher on Thursday, with the S&P reaching another all-time high and the Nasdaq extending its gains for a fourth consecutive session. Semiconductors, China tech, industrial metals, chemicals, and autos were standouts. Asian markets surged overnight, with Hong Kong up more than 3.5% and China’s Shanghai Composite gaining nearly 3%. European markets are up ~0.2%. Treasuries are mixed with some curve flattening, while the Dollar Index is up 0.1%. Yen strength is the main story in FX due to news that Shigeru Ishiba will be the next Prime Minister of Japan, weighing on Nikkei futures after the index gained over 2%. Gold is down 0.4%, Bitcoin futures are up 1.7%, and WTI crude is up 0.3% but down over 4% for the week.

The focus this week has been on aggressive stimulus measures out of China and the subsequent rally in under-owned Chinese shares, as well as continued optimism around the AI secular growth theme. While core PCE inflation is out today, market interest is more focused on next Friday’s September NFP data, as the Fed pivots its focus from inflation to growth.

Performance Recap of Large Cap Sector SPDR Funds for September 26, 2024

On September 26, 2024, US equities experienced mixed performance across the different sectors, with some sectors benefitting from continued optimism surrounding economic growth, AI-related advancements, and China’s fiscal stimulus measures, while others were weighed down by specific macro factors and geopolitical uncertainties.

Technology (XLK)

The Technology sector continued its leadership on the back of AI optimism. The sector was primarily driven by Nvidia (NVDA-US) and Microsoft (MSFT-US), both of which gained from bullish sentiment around AI and cloud infrastructure. Micron’s stronger-than-expected earnings and guidance also provided a significant boost to the semiconductor space. XLK saw a notable gain of +1.4%, supported by growing demand in data centers and chip manufacturing.

Healthcare (XLV)

Healthcare had a modest performance with +0.3%, benefiting from stability in pharmaceutical stocks, but with headwinds from MedTech companies. Regeneron (REGN-US) was a drag on performance, as the stock was downgraded after concerns about its Eylea franchise. Biotech stocks also saw some mixed reactions, particularly in the smaller cap space.

Financials (XLF)

Financials ended slightly lower by -0.2%, with pressure coming from regional banks and asset managers. Jefferies (JEF-US) missed Q3 earnings expectations, leading to a pullback in the sector. However, some large financial institutions like Goldman Sachs (GS-US) showed resilience ahead of the Q3 earnings season, with expectations of improved trading volumes and M&A activity.

Energy (XLE)

Energy stocks fell, with XLE down 0.8%, as crude oil prices retreated. WTI crude settled lower by 2.1%, weighing heavily on oil producers and service companies. Energy names such as ExxonMobil (XOM-US) and Chevron (CVX-US) led the decline, as profit-taking followed a recent strong run in oil prices.

Consumer Discretionary (XLY)

The Consumer Discretionary sector gained +1.0%. Tesla (TSLA-US) and Nike (NKE-US) were key drivers, with the latter experiencing positive sentiment as its new CEO announcement was well-received. Retailers showed mixed performance, though optimism about consumer demand ahead of the holiday season provided a slight lift to the broader sector.

Consumer Staples (XLP)

Consumer Staples fell slightly, down -0.3%, as concerns over inflation pressures and slowing demand affected performance. Procter & Gamble (PG-US) and Coca-Cola (KO-US) were laggards. There were also downgrades in the food and beverage space, impacting sentiment across the sector.

Industrials (XLI)

Industrials gained +0.7% on the back of strong machinery and construction-related stocks. Industrial metals and chemicals, which have exposure to China, rallied as well following the announcement of stimulus measures from Beijing. Caterpillar (CAT-US) and Honeywell (HON-US) were top gainers in the sector, supported by expectations of infrastructure spending and stronger demand from international markets.

Utilities (XLU)

The Utilities sector dropped -0.5%, lagging the broader market. Rising bond yields hurt interest-sensitive sectors like utilities, leading to a rotation out of the sector. Despite its year-to-date outperformance, investors took profits from utility names like NextEra Energy (NEE-US) and Duke Energy (DUK-US).

Real Estate (XLRE)

Real Estate was down -0.4% as higher interest rates weighed on REITs and property-related stocks. The sector continues to face pressure from high financing costs and concerns over lower demand in commercial real estate. Prologis (PLD-US) and American Tower (AMT-US) were among the notable decliners.

Materials (XLB)

The Materials sector was up +0.6% on strong performances in metals and mining stocks. Freeport-McMoRan (FCX-US) and Albemarle (ALB-US) led the gains, driven by renewed optimism for China’s demand for commodities. Chemicals stocks also posted solid returns with Dow (DOW-US) benefiting from higher industrial demand.

Communication Services (XLC)

The Communication Services sector rose +0.8%, supported by the strong performance of Meta Platforms (META-US), which benefited from continued optimism around AI-driven advertising and digital services. Snap (SNAP-US) also saw a boost after announcing a partnership with Google to integrate AI into its platform.

Conclusion:

Overall, it was a positive day for US equities, with strength in technology, industrials, and materials leading the way. However, energy and utilities underperformed, reflecting ongoing volatility in commodity prices and interest rate sensitivities.

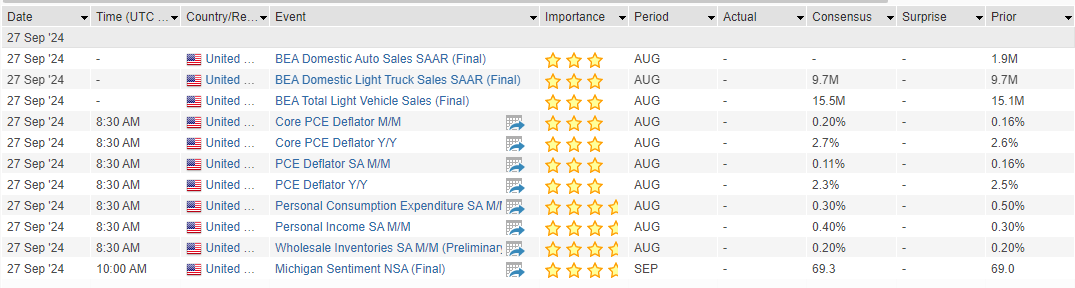

Economic Data

- Core PCE inflation is expected to rise by 0.2% month-over-month, bringing the year-over-year rate to 2.7%.

- The final University of Michigan consumer sentiment report for September is due today after the Conference Board’s measure showed the largest decline in over three years.

- Fed Governor Bowman will speak today, having already indicated she favors a more measured pace of rate cuts.

Refinancing Activity on the Rise:

- The Fed’s pivot has pushed mortgage rates down to around 6%, the lowest in two years, spurring a pickup in refinancing activity. The MBA refinancing index jumped over 20% in the week ended September 20th, following a 25% rise the prior week. Bloomberg estimates that current refinancing trends could save homeowners over $4K annually. This development, coupled with lower gas prices, is helping mitigate concerns about weakening consumer resilience.

Nvidia Market Cap Tops $3T:

- Nvidia (NVDA-US) saw its market cap surpass $3T on Wednesday. Analysts flagged the ~4% rally on Tuesday as being driven by reports that CEO Jensen Huang had completed his stock sale. Positioning dynamics were also a factor, with UBS noting that long-only portfolios remain underweight in Nvidia, which has cost large-cap managers 130 bps YTD. Nvidia is a major contributor to the Tech sector’s expected 15.3% y/y earnings growth in Q3, with its EPS expected to grow 85% y/y. Without Nvidia, Tech sector growth would halve to 7.9%.

Eco Data Releases | Friday September 27th, 2024

S&P 500 Constituent Earnings Announcements | Friday September 27th, 2024

No S&P 500 Constituents Report Today

Data sourced from FactSet Data Systems