February 21, 2025

We wanted to change the usual cadence of our Factor Friday report this week to review longer-term trend in factor investing with an aim to give our readers more context for interpreting current factor behavior. We will be back with our regular format next week when we will be surveying our indicator set ahead of our month end rebalance.

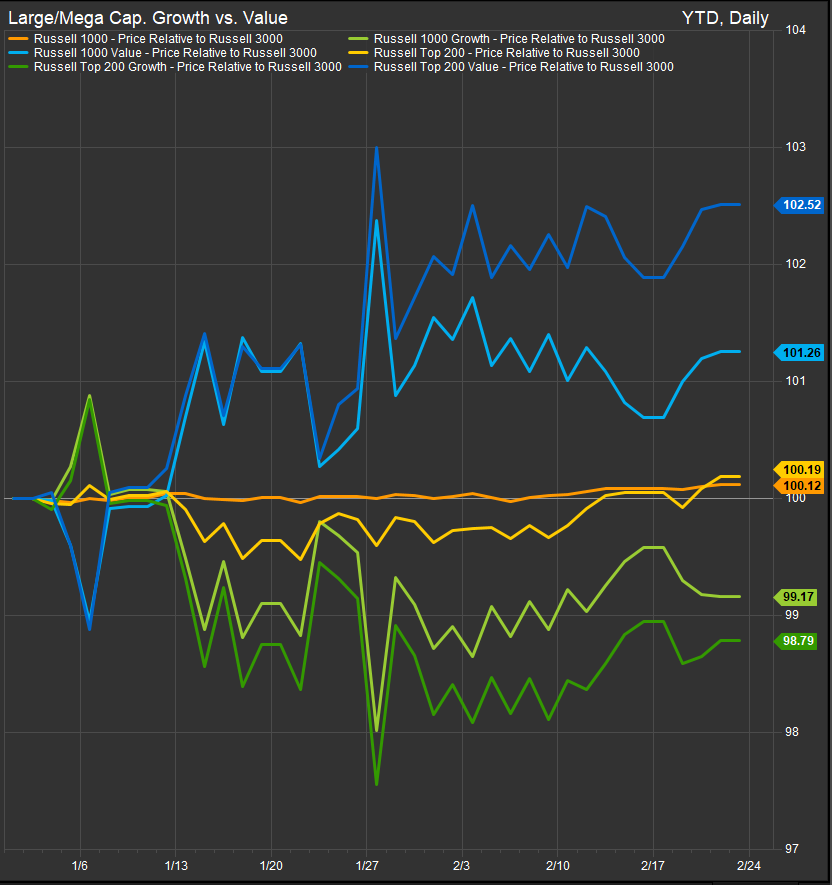

Growth vs. Value

The chart below shows our usual Large Cap. Growth vs. Value performance chart on a YTD timeframe. Value has had the advantage so far in 2025 though the spread is tight and the macro picture is ambivalent with rates generally moving sideways, equities inching higher and Commodities prices perking up (but not enough to motivate rates?).

This week, we are looking back at deeper history with the chart below showing the top 3 domestic Growth and Value ETFs by AUM and looking at their total return performance relative to the S&P 500 going back 20 years. What becomes obvious is the clear preference for Growth over the look-back period. In the recent past, the pandemic/post-pandemic cycles have seen Growth as an upside play and Value as an outperformer on the downside (chart below).

While we have 20 years of history to observe, we should note that this period has been dominated by Growth stocks in general for several structural reasons. The past 20 years have generally been characterized by historically low base-line interest rates in the US driven by the QE response to the Global Financial Crisis, the transition of the Commodities Super Cycle from a bull phase to a bear phase post GFC and the emergence of Technological innovation. These secular trends have been tailwinds to Growth over the very long-term.

Quality and Dividend Factors

While we don’t have as much history on Quality and Dividend, the chart below shows 10 years of daily returns for the top 3 ETF’s by AUM tracking each factor, there are some clear takeaways. 2 of our 3 Quality funds, the Invesco S&P 500 Quality ETF (SPHQ) and the iShares MSCI Quality Factor ETF (QUAL), have generally tracked market performance over the long-term while offering some alpha potential when equities correct at the top line. In contrast, the Dividend factor has underwhelmed with notable breakdowns in performance beginning in 2019.

The weakness in Dividend factor performance is hard to explain relative to traditional drivers of performance where interest rates moving lower has historically been a tailwind. Rates moved lower from 2019, but investors rotated into Growth stocks instead of income stocks. After finding footing as a haven in the bear market environment of 2022, the Dividend factor has underperformed significantly since equities regained their footing at the beginning of 2023. We suspect that an overhang of higher infaltion expectations is a primary culprit and that these stocks could remain under pressure until the advent of the next recession.

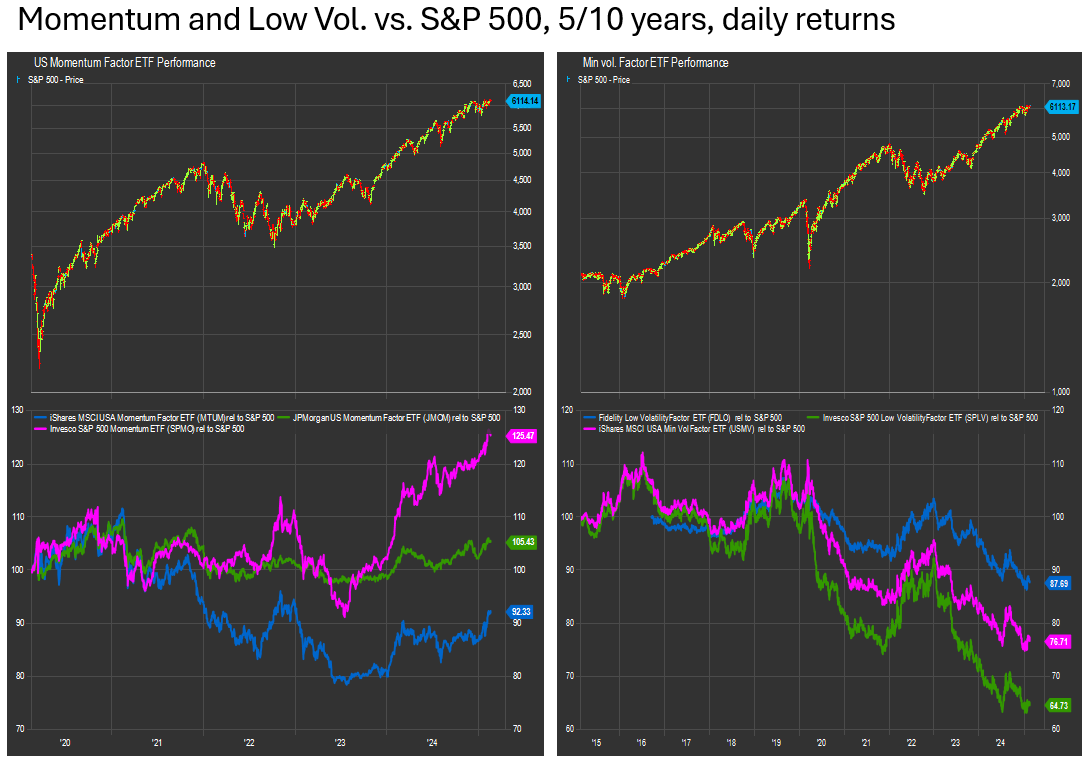

Momentum and Min Vol.

Min Vol. Factor ETFs have a very similar performance profile to the Dividend Factor funds we just discussed. They have lost significant ground since peaking prior to the COVID pandemic.

Momentum factor funds don’t have as much track record as others Factor-specific ETF categories, but it is interesting if somwhat ironic that momentum performance exhibits mean-reverting tendencies over the observed 5 year period. The Invesco S&P 500 Momentum Fund (SPMO) is currently the only Momentum fund really exhibiting any. Charts are below.

Conclusion

Anyone reading this below the age of 50 has seen most of their investment tenure play out in a pro-Growth market environment as well as a low (or falling) interest rate environment. From a long-term technical perspective, we believe we are in a transition period from a deflationary to a potentially inflationary environment similar to what played out in the 1960’s. We are skeptical that the US 10yr Yield will have a 1 or 2-handle on it at any future point in our lifetime (for reference we showed up in 1977), and we would also expect that the golden age of Growth investing is at hand, and likely in its later innings. That isn’t to say we should sell our Growth shares tomorrow, but just that over the next 5 years we are likely to see more inflationary pressures emerge rather than less, and we need to be prepared both mentally and tactically for that development as it is counter to what we have spent a long time experiencing.

Data sourced from FactSet Research Systems Inc.