Factor Friday: October 25, 2024

The S&P 500 has been in near-term consolidation this week after reaching all-time highs in the middle of October. Investors continue to weigh the bull market and a supportive Fed against the potential that easier interest rate policy could re-ignite some inflationary dynamics back into the picture. Our macro work becomes important in these times because the charts of the US 10yr Yield and the Bloomberg Commodities Index give us key levels to watch for and ID trend change. Our research across cycles informs us that Commodities prices are a key indicator, driver and sustainer of inflationary trends. That’s why we have been so focused on Crude and Commodities over the past several months despite the small Market Cap. footprints of the Energy and Materials Sectors. We want to lead off this week’s Factor Friday report with a recap of those charts as they will go a long way in determining whether Growth or Value oriented sectors take the leadership role as we move forward.

The US 10yr Yield chart has backed up into overhead resistance. The band between 4.3%-4.5% is an important potential pivot. Failure here conforms to the long-term downtrend in rates that has developed over the past 12 months. We’ve pointed out on several occasions that relief from higher interest rates is a key consideration for the Consumer as well as the Industrial base of the economy. We would be very skeptical that Yields at 4.5-5% would offer the necessary relief, hence a key component of the bullish case is Yields moving lower. 4.3% is the current “line in the sand”. See below.

The Bloomberg Commodities Index is showing a similar upside reversal to yields which should be unsurprising. Here we see the key zone as between 100 and 103. A move above 103 would have us taking the inflation trade a lot more seriously. If Commodities prices stay flat to lower moving forward, we will have more confidence/conviction in the sustainability of the bull trend in equities.

Sectors

The Fed’s interest rate intervention had initial elicited positive price reactions from the Consumer Discretionary, Info Tech. and Energy Sectors, but the since September 1, performance dispersion has been narrow. Healthcare, Staples and Energy have been laggards while Discretionary has made the biggest relative gains followed by Utilities. That pairing is historically an odd couple, but it speaks to the near-term hesitance of market participants despite the context of the prevailing bull trend.

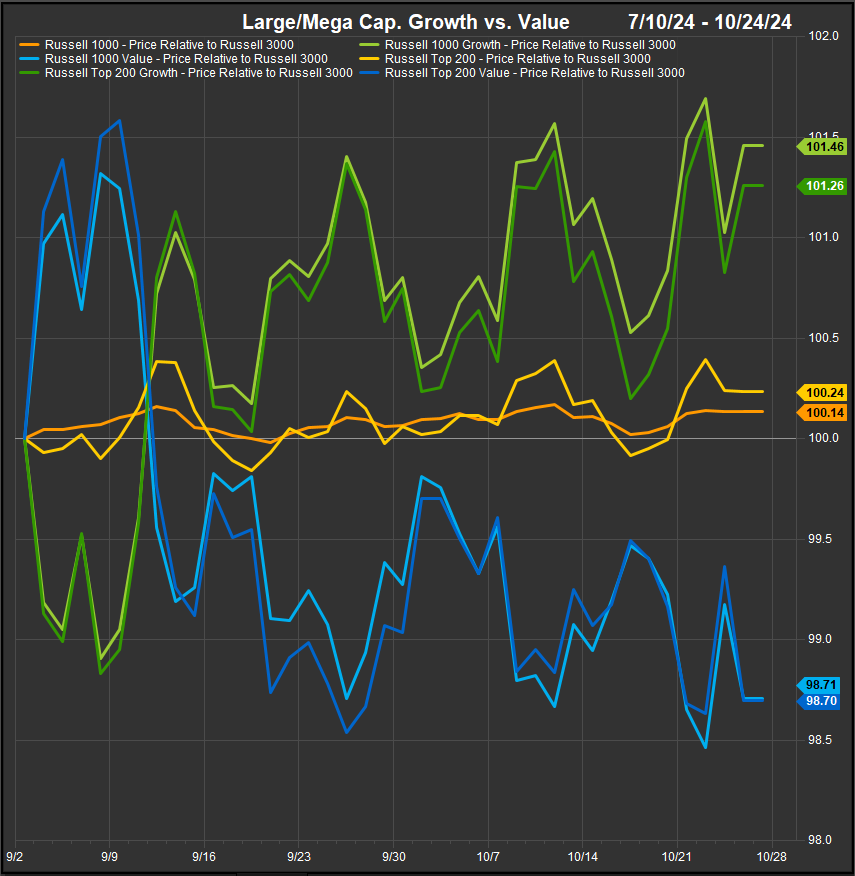

Large/Mega Cap. Growth vs. Value has been a knife fight since September

Sharp mean-reversion has continued to inform the dynamic between large cap. Growth and Value. This week investors shifted back to Growth and put just a tiny bit of daylight between the two styles. At the reisk of oversimplifying we think Value will outperform in inflationary scenarios and Growth will do better if rates end the year with a 3-handle. Utilities, Energy, and Financials have the largest positive weight differentials in Value indices vs. the broad market S&P 500, while Technology and Comm Services Sectors have the least. There are market structure elements that would motivate rotation if inflation re-emerges.

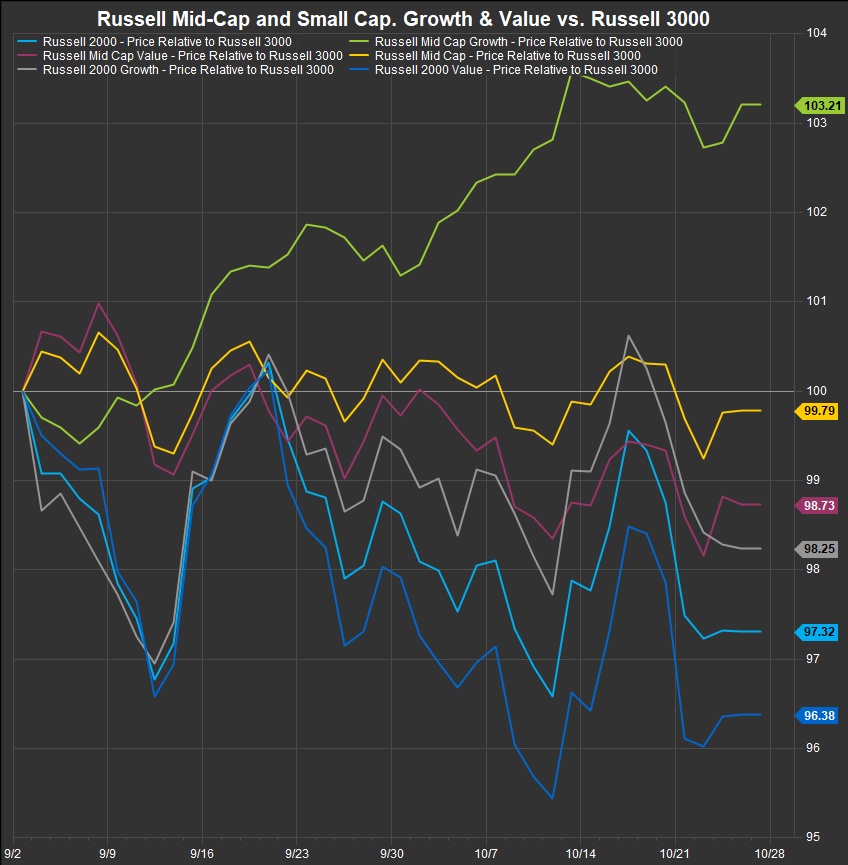

Small/Mid Stocks: MidCap Growth Starting to Differentiate Positively

In contrast to the Large/Mega Cap. space, the Small/Mid tiers of the US equity market continue to be a scrum. The one development of significance has been the recent emergence of MidCap Growth which has started to distinguish itself positively. In general the Mid-Cap tier is performing better than Small Cap as the chart below shows.

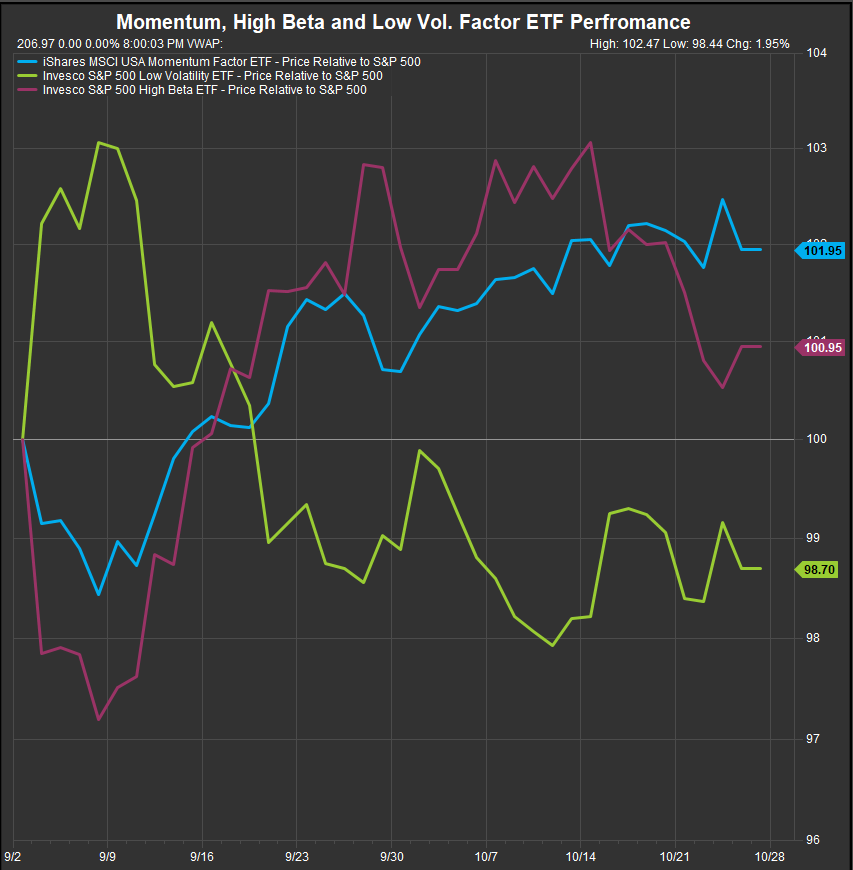

Momentum, High Beta & Low Vol: High Beta Rolls Over

One of the key takeaways of this cycle has been the persistent feedback loop between emergent optimism à rates move higher à emergent pessimism because rates moved higher. We are seeing that play out again around Fed policy intervention. High beta took the baton, investors moved out of bonds and bought stocks, and now we’re worried the Yields rose. The Invesco S&P 500 High Beta ETF rolled over on October 15th. This may have been more motivated by Geo/Political concerns, as Crude Oil also had a setback. Economically sensitive cyclicals which encompass a large swath of Commodities-adjacent Sectors like Energy, Materials and Industrials are among the highest beta stocks. The momentum factor is generally more representative of the Growth side of the market, and that cohort has weathered the macro turbulence a little better in the near-term.

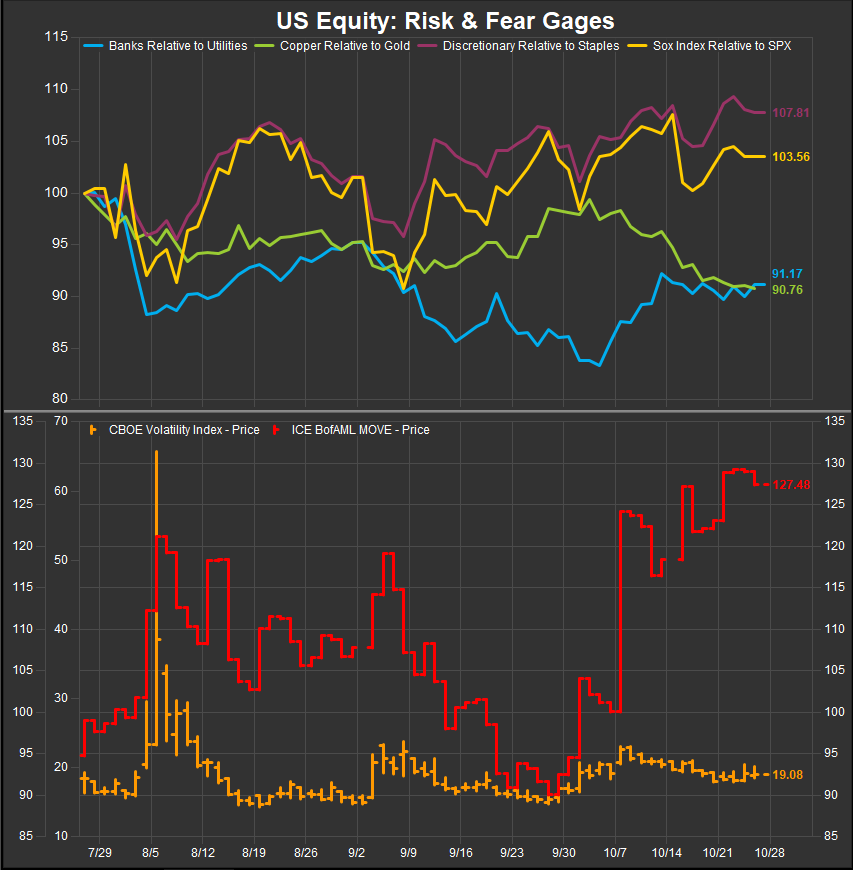

Risk On/Risk Off: Equity Risk-on Ratios Remain Constructive for the Bull

As we mentioned in our lead, bond vol. and generally rising rates in the very near-term reminds us that there are vulnerabilities to the current bullish scenario being discounted on the equity side. VIX has settled from its move up to the 20’s.

Looking at our equity market risk gages, Banks have executed a sharp positive turn against Utilities while Semiconductors and Discretionary stocks remain in constructive patterns despite respective pullbacks vs. defensive counterparts in the past week. On the Cmmodities side, Copper has given back vs. gold and has made new 12-month relative lows. Aligning with our bullish thesis longer-term, we are looking for rates to continue sideways to lower but will take a move higher as a caution flag.

In Conclusion

Equity leadership has been fleeting since July, but the upward pressure has come off Commodities prices while rates have pushed higher regardless. With Commodities prices lower, Growth performance has improved and has a slight edge at present. The forward direction of rates will likely have a big impact on leadership. We’d expect a mix of defense (on inflationary recession fears) and Value (on inflationary growth scenarios) to outperform with rates rising. We’d expect Growth factor exposures to outperform if rates end the year on a 3-handle.

Data sourced from FactSet Research Systems Inc.