Equities are likely to close a second consecutive week above the 6000 level. The bull is in control of the tape and interest rates have acted according to the Bull’s stage directions, rolling over before they scared us too much.

We started off last week’s report highlighting near-term performance improvement in the Russell 2000 and warning of a loss of momentum in the Tech Sector. This week saw mean reversion for both of those charts against our near-term expectations. The Tech Sector broke out to new highs while the R2K consolidated though it remains in a constructive pattern. The Sox Index is still exhibiting a concerning lack of buyer interest despite retracing almost all of its outperformance over the past 12 months.

Tech Sector Regaining Strength

The VGT has now made sequential higher highs above its July peak. Our intermediate-term price target for the fund is $700, about 8% higher than today’s price.

SOX (Semiconductors) Index Still in a Vulnerable Position

With Information Technology shares firming in aggregate, we are a bit more optimistic on the forward prospects for Semiconductors, but they are not out of the woods yet as the saying goes. The chart below shows an unresolved wedge pattern that continues to linger near a flattening 200-day moving average. This is not a position of strength in the technical paradigm. In the oscillator work the absence of an overbought reading since the big 27+% correction in July. 5217-5315 remains the key level for Semi’s to register a bullish reversal, but we can’t get too hyped about the Tech Sector while Semiconductors look like this. That said we continue to have a long position in the former despite the latter.

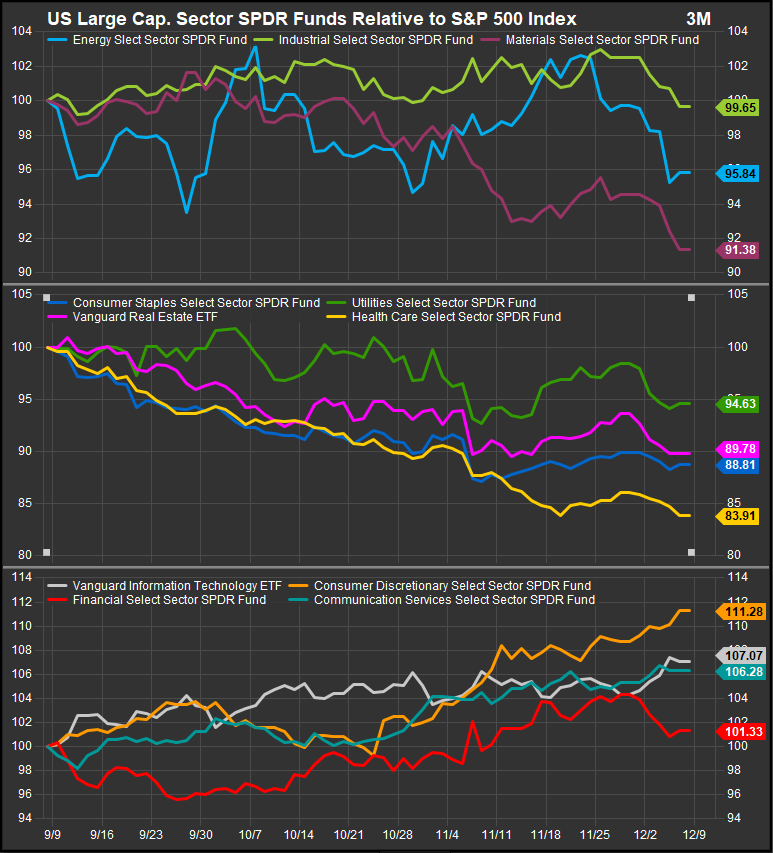

Sectors

With another week in the books, the sector leadership picture over the past 3 months has resolved around the Bull. On the chart below, commodities linked sector performance (top panel) has rolled over, min vol. sectors (panel 2) have persisted in a performance downtrend and historical upside exposures (bottom panel) are generally in uptrends. The upside momentum from the Discretionary Sector has been impressive and has strengthened our bullish conviction. We had some concerns about the Consumer’s ability to weather resurgent interest rates, but with rates softening we like what we are seeing there and we think investors should be long.

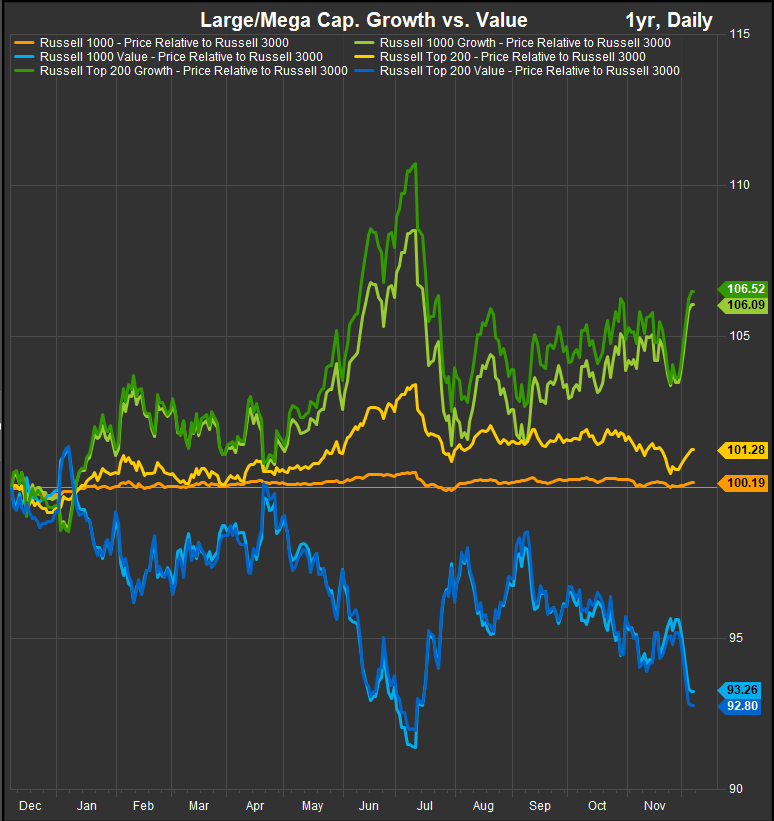

Large/Mega Cap: Growth Breaks-Out, Gives a Clear Buy Signal

The relationship between interest rates and Growth vs. Value is a powerful one. Interest rates have rolled over in the past week and Growth has taken off vs. Value. In our opinion, the one one is the driver of the other, and really has been since the beginning of the Q/E era after the Global Financial Crisis of 2008. The chart below illustrates the dynamic. If these were stock charts and not relative performance, you would expect Growth to eventually retest relative highs of July and Value to retest those same relative lows.

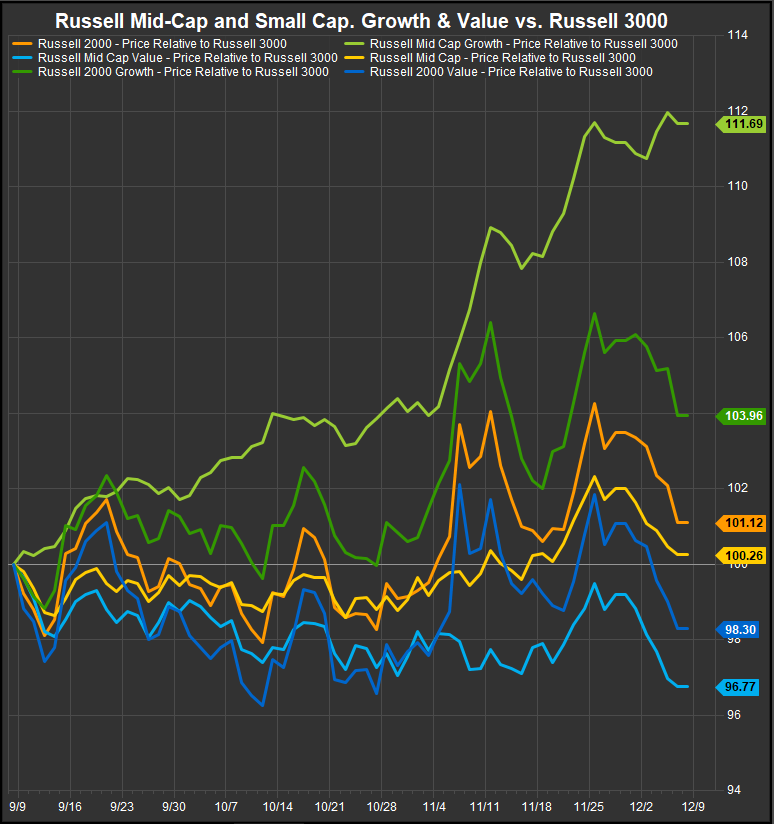

Small/Mid Stocks: MidCap Growth Surge Continues

MidCap Growth outperformance continues while Small Cap. shares have corrected in the past week. With Mid-Cap. Growth breaking away from the Small/Mid pack this is confirmation of Growth over Value for us from what had been a knife-fight for much of August through October.

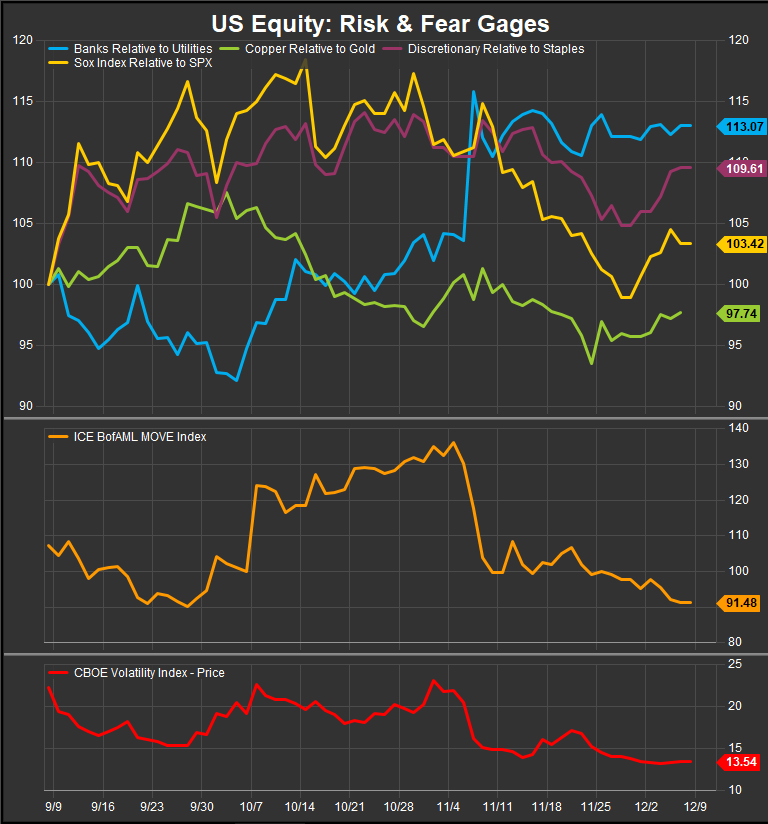

Momentum & High Beta have the Edge over Low Vol.

Momentum and High Beta have widened out the spread vs. Min Vol. The latter is now deeply oversold and has some potential to bounce back with rates now in a more favorable position for equity income investors. That said, risk appetite has firmed since the US Election and we think investors should be positioned for higher prices through year-end at this time.

Risk On/Risk Off: Vol. Remains Low, Risk Appetite Gages Firm

The VIX and MOVE Indices, representing volatility in the equity and fixed income markets respectively, are both at lows of the past 3-months. It is important to note that these gages represent only the vol. that is “priced in” by the options market. With interest rates rolling over again to the downside our biggest risk to the continued bull has ameliorated for the time being. There is or course a risk of complacency as there are certainly developments locally and abroad that could end up being negative for financial markets in general and equities in paricular, but we are seeing a fairly clean technical setup for the Bull trend to continue and we make our money by respecting the message of the market rather than by thinking we know something it doesn’t.

In Conclusion

Equity leadership has been fleeting since July, but the upward pressure has come off Commodities prices and has now come off interest rates as well. Given the context of a sustained bull trend for US equities at the index level, this favors Growth over Value and risk on over risk off. We will leave it at that until next week.

Data sourced from FactSet Research Systems Inc.