March 13, 2026

The Iran conflict has pushed factor investing back into a macro regime where oil, rates, and risk appetite matter more than narrative alone. The market is trying to reconcile two competing realities at once. On one side, U.S. Growth still has the strongest structural earnings story, led by AI capex, software monetization, and semiconductor demand. On the other, a war-driven energy shock is the classic setup for higher inflation risk, firmer long yields, and pressure on long-duration assets.

That tension is why factor leadership has become less about conviction and more about survivability.

The most important macro development is that the conflict has not behaved like a textbook “flight-to-safety” event for bonds. Reuters reported that the U.S. 10-year Treasury yield has risen to 4.26%, up nearly 30 basis points since the conflict intensified, as investors reassessed inflation and term-premium risks rather than rushing unambiguously into duration. Reuters’ survey also found strategists looking for the 10-year to remain around current levels near 4.20%–4.25% over the next six to twelve months.

That matters because rising or sticky real yields are the single biggest headwind to pure Growth leadership. Growth can still work—but it needs either falling yields or so much earnings momentum that it can outrun the discount-rate problem. The headlines this week give both the bullish and bearish versions of that story. On the bullish side, AI revenue and capex commentary remain strong: Broadcom’s longer-dated AI targets, OpenAI and Anthropic revenue momentum, and ongoing hyperscaler spending all reinforce the secular case. On the bearish side, Oracle job cuts, AI export-rule risk, and renewed scrutiny of ROI and software disruption all remind investors that this cycle is capital-intensive and increasingly contested.

US 10yr Real Yield Proxy

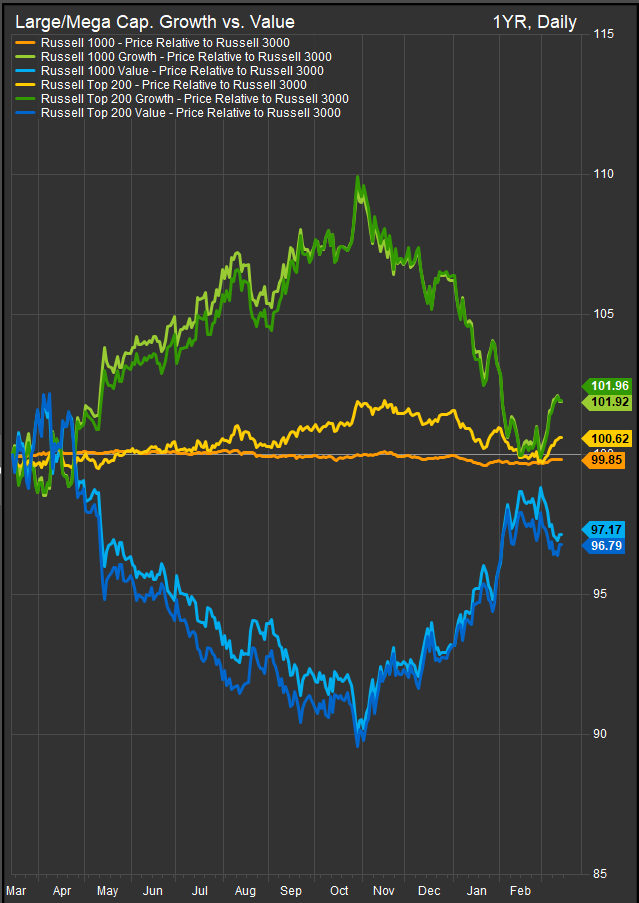

Growth: still the best long-term story, but no longer the easiest trade

Growth is not broken. It is simply more conditional. The recent rebound in software and semis makes sense because positioning had become too defensive and because earnings revisions in parts of Tech remain intact. But if oil stays elevated and the conflict pushes inflation expectations higher, Growth’s valuation premium becomes harder to defend. In other words, Growth needs stability—in rates, in energy, and in policy. Without that, it becomes a stock-picking factor rather than a broad market leadership factor.

Value: the macro hedge is back

Value currently has the cleaner macro tailwind. An energy shock naturally supports Energy, Materials, and parts of Financials and Industrials. MSCI’s recent work on geopolitical shocks tied to oil disruption found that energy had the highest positive sensitivity across regions, and that where oil disruption becomes a broader macro shock, inflation stays higher and central-bank flexibility shrinks. That maps directly onto the current setup. The StreetAccount headlines reinforce it: Gulf supply disruptions, shipping risks, and reserve-release skepticism all point to a world where hard-asset cash flows regain strategic importance.

Per the factor performance chart above, Growth has rebounded in the very near-term, but context is important. As the lagging factor heading into the advent of hostilities, we expect a near-term bounce. Adverse market events typically spur profit taking and rotation into out-of-favor exposures. We think that technical dynamic explains the bounce in Growth stocks. We don’t expect Growth performance to hold up if rates continue higher from present levels.

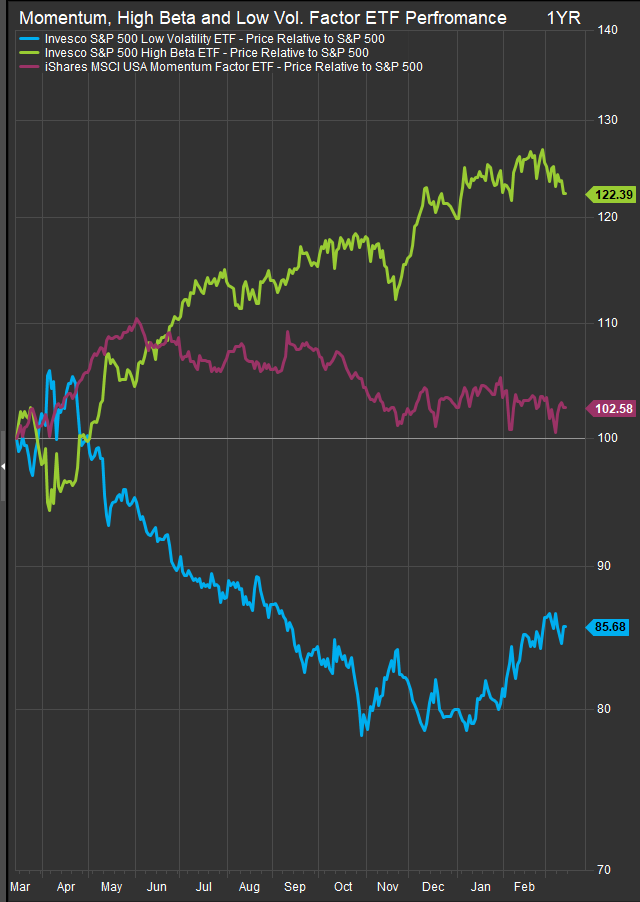

High Beta: not the place to be aggressive

High Beta is where investors should be most careful. If the macro environment were simply “soft landing plus lower rates,” high beta could work. But this is not that. This is an environment with rising oil, higher Treasury volatility, and concern that parts of the private-credit complex remain fragile. MSCI’s research argues that when geopolitical shocks remain contained, losses often fade within a month—but when they become true oil-supply shocks, the damage spreads across asset classes and lasts much longer. High beta is a bet that the conflict fades quickly and that the macro spillover remains minimal. That may happen, but the risk-reward is no longer asymmetric.

Low Vol: increasingly relevant

Low Vol is becoming easier to justify. The same MSCI work found that minimum volatility outperformed across regions during the early phase of this shock, and that defensive sectors held up best outside the U.S. In U.S. equities, that points investors toward Utilities, Consumer Staples, Health Care, and selective Real Estate. These sectors offer a combination of lower earnings cyclicality, steadier balance sheets, and in some cases direct pricing power. If the market keeps oscillating between war headlines and inflation concerns, Low Vol becomes less a hiding place and more a core allocation.

Momentum: still positive, but increasingly narrow

Momentum has not broken, but it is becoming more selective. The strongest momentum remains in commodity-linked winners, select AI infrastructure names, and defensive growth franchises. What is fading is the idea that one can simply own “the market leaders” indiscriminately. Momentum works best when macro uncertainty is declining. Here, it is being continually interrupted by oil spikes, geopolitical headlines, and changes in rate expectations. That argues for following earnings-backed momentum, not sentiment-driven momentum.

What should macro investors favor now?

At the moment, macro trends favor a barbell tilted toward Value and Low Vol, with selective rather than broad Growth.

The clearest favored exposures are:

- Energy and Materials, because the conflict keeps oil and commodity risk front and center.

- Low Vol / defensive sectors such as Utilities, Staples, and Health Care, because they offer resilience if higher oil spills into weaker consumer and business confidence.

- Selective Growth, especially semis and software with clear earnings visibility, but only where balance-sheet strength and demand durability are obvious.

The least favored exposures are:

- High Beta cyclicals that depend on a fast normalization in oil and rates.

- Speculative long-duration Growth that still needs falling yields to justify current multiples.

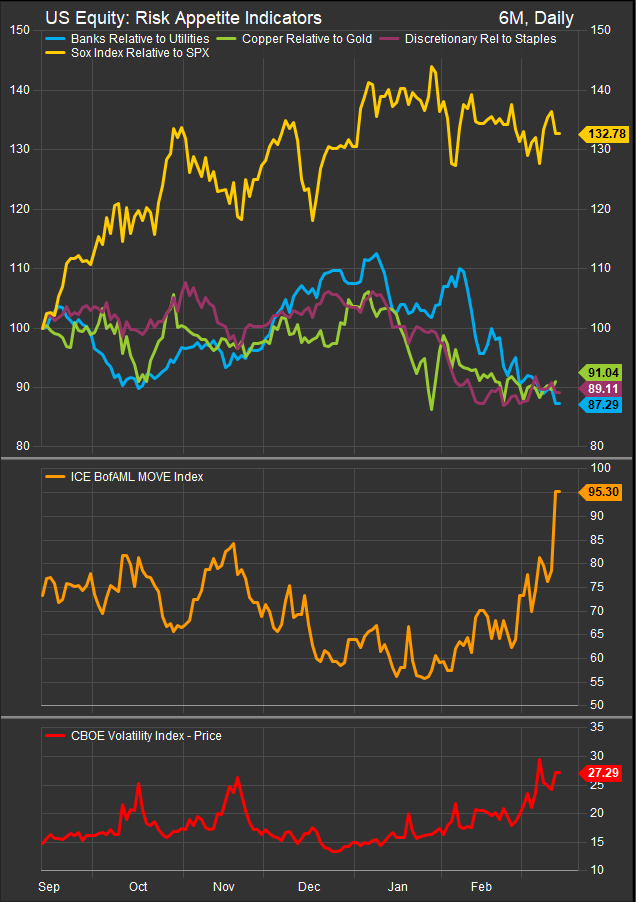

Our risk appetite gages (chart below) are rolling over to favor risk-off in the near-term as the VIX and MOVE indices continue to push higher. Conservative exposures are likely to benefit in the short-term at least.

Bottom line

The Iran conflict has not ended the Growth story. It has changed the burden of proof. Growth can still outperform, but only if earnings stay exceptional enough to overpower higher yields and inflation fears. Value has the cleaner macro setup, and Low Vol has the most obvious role as a portfolio stabilizer. Momentum still works, but it must be filtered through balance-sheet quality and earnings durability.

For now, the most sensible factor stance is not to chase the most exciting story. It is to own the factors that can still work if the war lingers, oil stays high, and the bond market refuses to fully relax.

-

FactSet Research Systems / StreetAccount – Market summaries, sector performance commentary, geopolitical headlines, and macro event recaps used throughout the analysis.

-

Reuters – Reporting on oil market disruptions, Strait of Hormuz shipping risks, inflation implications, and U.S. Treasury yield expectations.

-

Bloomberg News – Coverage of energy market volatility, Treasury market movements, AI-related borrowing, and global investor positioning.

-

Financial Times – Analysis of geopolitical risk transmission into global supply chains, private credit markets, and energy pricing dynamics.

-

MSCI Research – Multi-asset analysis of geopolitical shocks and oil supply disruptions and their impact on factor and sector performance.

-

International Energy Agency (IEA) – Emergency oil reserve release data and global oil supply outlook.

-

U.S. Energy Information Administration (EIA) – Data on global crude flows through the Strait of Hormuz and oil market sensitivity to supply disruptions.

-

Federal Reserve Bank of New York – Survey of Consumer Expectations data on inflation expectations, income outlook, and labor market sentiment.

-

National Federation of Independent Business (NFIB) – Small Business Optimism Index and economic outlook data

Other charts and data sourced from FactSet Research Systems Inc.