Equities are likely to close a third consecutive week above the 6000 level on the S&P 500. Bullish macro conditions prevail as rates continue to roll over from near term highs in mid-November. Leadership has clustered around large cap. Growth again with the Discretionary Sector driving outperformance along with Communications services. The Mag7 may be winnowed down to a Mag4, but TSLA, AMZN, GOOG and META have remained stalwart, and the Tech Sector giants are still owed some time to consolidate after banner performance in 2023 that launched this bull market.

Sectors

Over a 6-month time period, Discretionary stocks have established clear outperformance followed by Comm. Services. Financials have pulled back in the near-term after strong post-election performance. This troika makes up the sector leadership profile of what we consider the 2nd phase of this bull market. The first was the Tech led AI melt-up and if we are lucky, we are starting the next phase where successful AI practitioners (like WMT) execute strategies that compound operating efficiencies and earnings power. So far so good for the Waltons, and if other companies can follow suit, we will see big productivity gains across value chains and the catalyst for a continued bull trend. We’re getting a bit over our ski’s here, but the performance trends are encouraging for bull market exposures.

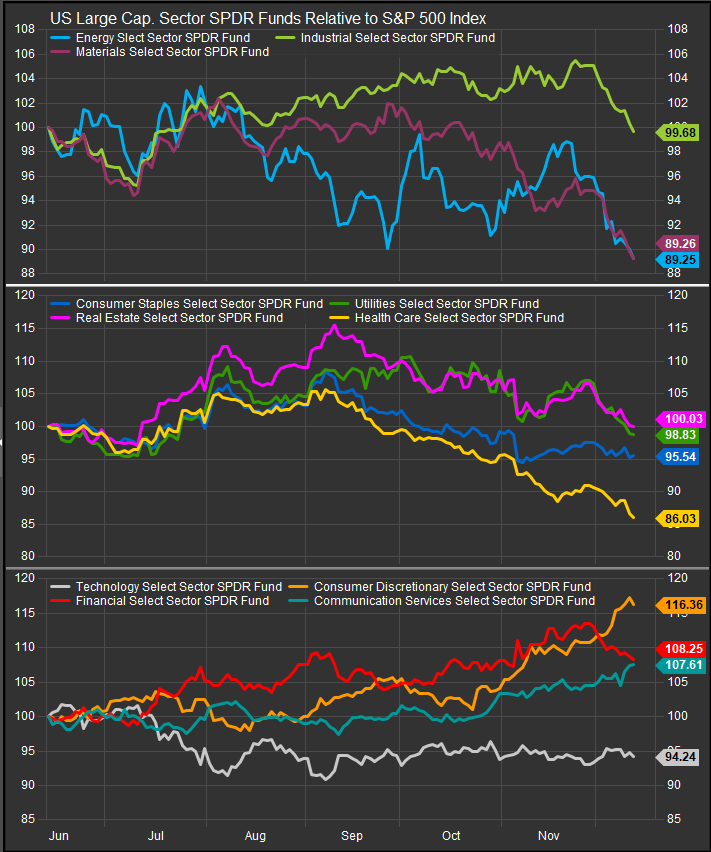

On the downside, as seen in the chart below, the Energy Sector is back to 6-month lows, while the Materials Sector is right there with it. The bullish reversal in low vol. sectors (chart, middle panel) is a fading memory as well. Our Elev8 model has us under-exposed to both of these groups at present, though we feel more comfortable hedging our current positioning with low vol. sector exposures as we do think the stock level drivers of the bull market are near-term overbought from a technical perspective.

Large/Mega Cap: Growth Breaks-Out, Gives a Clear Buy Signal

With rates continuing to consolidate and the equity uptrend intact, Growth has continued to separate positively from Value as a style factor. The re-emergence of Mag7 leadership in the near-term is a clear catalyst, but we are also seeing enthusiasm for the recently down-and-out ARKK fund, as well as Crypto, which has boosted a few halo stocks to big gains. While rates stay under control of the Fed, we expect Growth to lead.

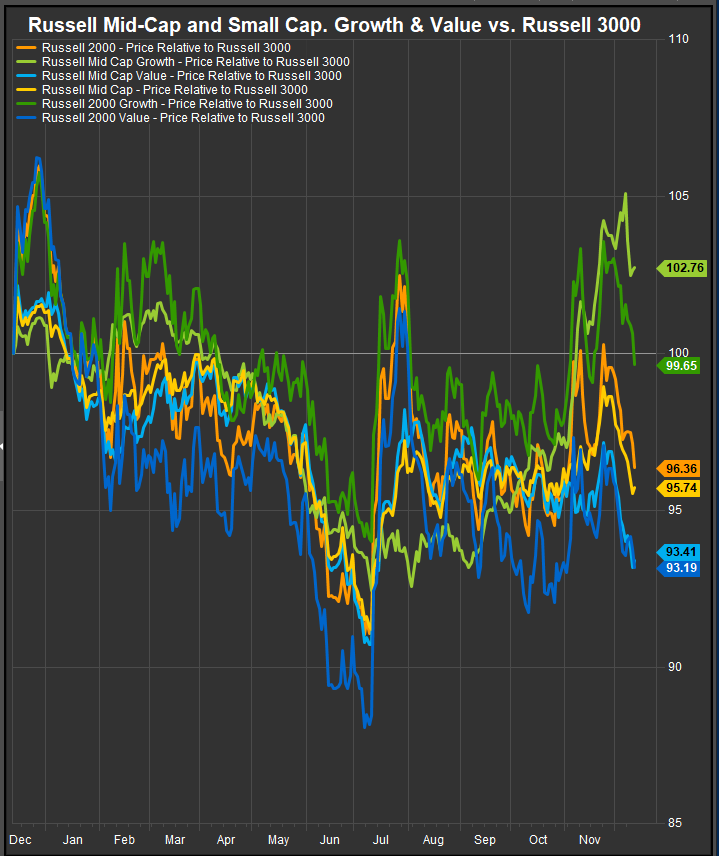

Small/Mid Stocks: Small/Mid still showing higher correlation

MidCap Growth and Small/Mid Growth in general has outperformed Value since the election. When analyzing the MidCap index, the drivers of Growth stock outperformance are a little different than one might think. Asset managers like KKR and other financials are a big driver of Growth outperformance as well as MidCap Comm Services stocks which have inflected higher on speculation that deregulation could lead to M&A roll-ups at premium prices.

In the very near-term Small/Mid Growth is pulling back and the smaller cap-tiers are starting to exhibit elevated positive correlation again after a brief untethering. The chart below tells the story. It’s a Large Cap. World again.

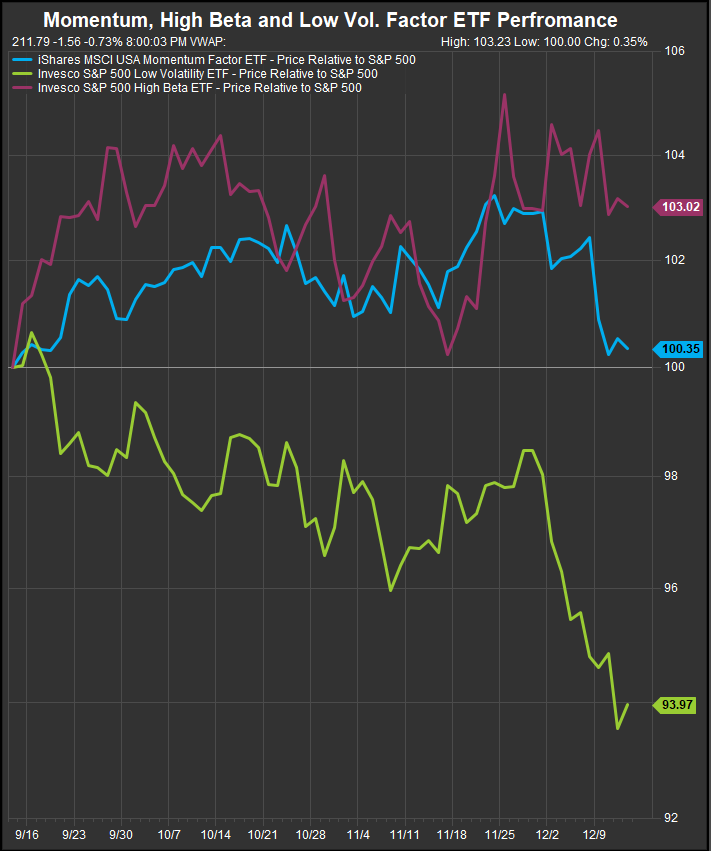

Momentum & High Beta have the Edge over Low Vol.

The Invesco Low Vol. ETF, our low vol. factor proxy, is now oversold in the near-term and setup to bounce if any negative news effects the tape. Momentum has cooled off while High-Beta has held up a little better in December. This is still a clear bull market posture.

Risk On/Risk Off: Vol. Remains Low, Risk Appetite Gages Firm

The VIX and MOVE Indices, representing volatility in the equity and fixed income markets respectively, are both at or near lows of the past 6-months. It is important to note that these gages represent only the vol. that is “priced in” by the options market. With interest rates rolling over again to the downside our biggest risk to the continued bull market has ameliorated for the time being. The main risk we see at present is complacency, and we recommend a small allocation to lower vol. positions even though they are currently out of favor.

Looking more closely at the risk on/risk off ratios we track, Banks have had their way with Utilities and are clear outperformers, but Copper isn’t showing vs. Gold and Semiconductors are in consolidation and losing ground to the broad market. Discretionary stocks have taken leadership from staples and show a clear risk-on signal.

In Conclusion

Growth is back in the driver’s seat as investors are feeling sanguine about Fed policy and the “Soft Landing” scenario. Inflation, so far, has threaded the needle and the Fed continues to signal that it is in the business of supporting the economcy, not battling inflation. The outlook is positive, and the only warning we can issue is against complacency. Spend some time thinking about how you would re-position for the next exogenous shock, but keep aligned with Growth and historically upside sector exposures like Financials, Discretionary, Comm. Services and Technology.

Data sourced from FactSet Research Systems Inc.