The factor tape is not flashing recession. It is showing a market still willing to own risk, but with a much higher bar for crowded trades. The biggest macro inputs this week are subdued jobless claims, sticky inflation risk, possible Fed hikes, bank earnings optimism, and a choppy momentum unwind.

For sector investors, the message is straightforward: keep exposure to AI-linked momentum, add quality screens, and use cyclical exposure selectively through Financials and Industrials.

- Momentum Still Leads, But the Trade Is More Fragile

Momentum remains the strongest intermediate-term factor. The momentum ETF group in the factor dashboard is up roughly 15.7% over 3 months and 20.9% over 6 months, with average excess returns versus the S&P 500 of about +5.2% over 3 months and +12.7% over 6 months. Invesco S&P 500 Momentum (SPMO) has been especially strong, with 24.9% 3-month and 28.1% 6-month returns.

But the short-term signal is weaker. Momentum ETFs averaged a 0.8% 1-week decline, while iShares MSCI USA Momentum (MTUM) has only about 44% of holdings above their 50-day moving average, even though roughly 90% remain above their 200-day moving average. That is a classic “long-term trend intact, short-term leadership stretched” setup.

Sector implication: Vanguard Information Technology (VGT) and Vanguard Communication Services (VOX) remain supported, but investors should not chase broad momentum exposure indiscriminately. The better approach is to own the durable parts of momentum: AI hardware, semiconductors, cloud platforms, data-center infrastructure, and profitable mega-cap platforms. Stock examples include NVDA, AVGO, MSFT, META, GOOGL, AMAT, LRCX and KLAC.

Chart: High beta and momentum of tracked in 2026. Upwards pressure on interest rates has kept a lid on low vol. factor performance until recently.

- Higher-for-Longer Rates Favor Quality, Banks and Dividend Growth

The macro backdrop is not giving the market a clean easing signal. Jobless claims remain subdued, the Fed still sees inflation risk, markets are pricing rate-hike risk through year-end, and NY Fed President Williams flagged AI demand as a potential inflation and neutral-rate risk. That keeps real-rate pressure in the market and makes low-quality duration harder to own.

The factor data supports a quality-over-speculation view. JPMorgan U.S. Quality Factor (JQUA) gained 3.2% over 1 month, 14.2% over 3 months, and 12.3% over 6 months, outperforming the S&P 500 across all three periods. Invesco S&P 500 Quality (SPHQ) also outperformed, with 2.6% 1-month, 10.8% 3-month, and 13.5% 6-month returns.

Value is more mixed, but there is clear support in cleaner large- and small-cap value proxies. iShares Russell 1000 Value (IWD) gained 3.4% over 1 month and 13.2% over 6 months, while iShares Russell 2000 Value (IWN) gained 3.5% over 1 month and 14.8% over 6 months. Dividend growth is also more attractive than high dividend yield. First Trust Rising Dividend Achievers (RDVY) gained 4.1% over 1 month, while traditional high-dividend funds were less impressive.

Sector implication: Vanguard Financials (VFH) should remain one of the most important beneficiaries of the factor setup. Higher-for-longer rates, resilient credit, bank earnings, capital-markets activity, and post-stress-test capital return all support large banks, brokers, exchanges and insurers. Stock examples include JPM, BAC, WFC, GS, MS, ICE, CME, CB and PGR.

- The Cycle Looks Firm Enough for Selective High Beta

The strongest cyclical signal comes from high beta. Invesco S&P 500 High Beta (SPHB) is up 22.5% over 3 months and 21.6% over 6 months, outperforming the S&P 500 by roughly 12.0 percentage points over 3 months and 13.4 points over 6 months. That lines up with the macro data: claims remain low, services activity is still expanding, demand in construction, infrastructure and health care remains resilient, and AI/data-center activity continues to support growth.

However, this is not a green light for all cyclical exposure. Existing home sales fell, affordability remains strained, and inflation is still too high for the Fed to declare victory. Low-volatility funds have not led over 3- and 6-month periods, which tells us investors are not hiding in defensives. But the market is also not rewarding low-quality cyclicals indiscriminately.

Sector implication: Vanguard Industrials (VIS) is the cleanest cyclical sector call. The best exposure is in infrastructure, electrical equipment, machinery, automation, defense and data-center buildout. Stock examples include ETN, VRT, PWR, GEV, HUBB, CAT, EMR and PH.

Vanguard Health Care (VHT) also deserves a place in the broadening trade, but as a quality/catalyst exposure rather than a deep cyclical. ISM commentary pointed to resilient health care demand, while the market has been rotating back toward biotech and selected pharma. Stock examples include LLY, NVO, REGN, VRTX, AMGN and ABBV.

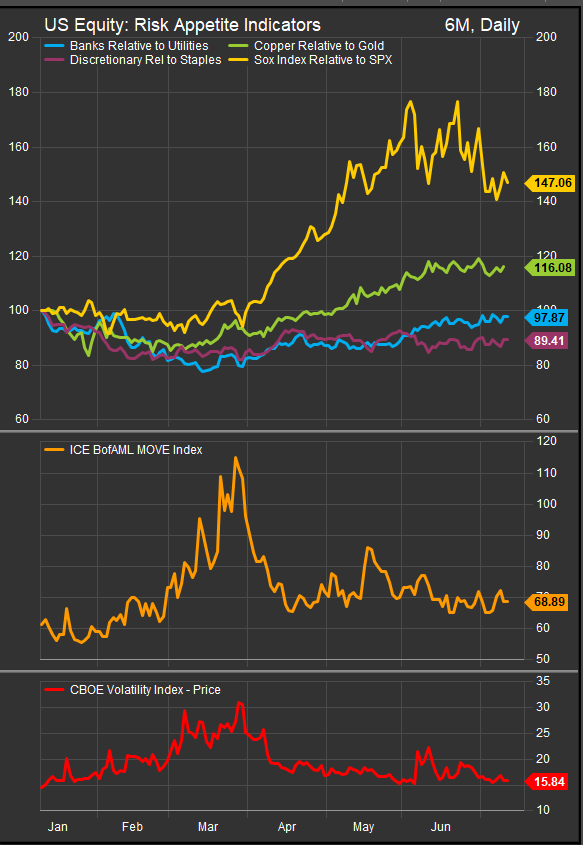

Chart: Economic data prints have been firmer in 2026 with initial jobless claims remaining subdued despite inflation concerns. Risk Appetite indicators are constructive despite the recent shake-out in the Semiconductor space.

Sector Takeaway

Factor returns are saying the business cycle still looks firm, but leadership is becoming more disciplined. Momentum has not broken, but it is stretched. High beta is working, but mainly where earnings leverage is visible. Quality is becoming the better wrapper for equity risk. Value is improving, but the best expression is not generic cheapness; it is banks, insurers, dividend growers and cyclicals with earnings support.

| Factor signal | Sector implication | Sector ETFs | Stock examples |

| Momentum intact but stretched | Stay exposed to AI leadership, but emphasize quality | VGT, VOX | NVDA, AVGO, MSFT, META, GOOGL |

| Higher-for-longer rates | Favor banks, insurers and dividend growth | VFH | JPM, GS, MS, CB, PGR |

| High beta still working | Own selective cyclicals and infrastructure | VIS | ETN, VRT, PWR, GEV, CAT |

| Quality outperforming | Use quality screens across Tech, Financials and Industrials | VGT, VFH, VIS | MSFT, AVGO, ETN, JPM |

| Defensive bond proxies not leading | Avoid overpaying for rate-sensitive defensives | VPU, VDC, VNQ | Utilities, staples and REITs need rate relief |

The bottom line: Factor Friday is still constructive on equities, but not on indiscriminate risk-taking. The best sector setup is quality momentum in Vanguard Information Technology (VGT), rate-supported Vanguard Financials (VFH), and infrastructure-linked Vanguard Industrials (VIS). Vanguard Health Care (VHT) can participate as a non-AI quality rotation. The weakest setup is in defensive bond proxies, speculative long-duration growth and low-quality cyclicals that need lower rates to work.

Disclaimer: This material is for informational and educational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any ETF, security, sector exposure, or investment strategy. Factor performance and sector leadership can change quickly and may reflect short-term positioning rather than durable market trends. Past performance is not indicative of future results. Investors should consider their objectives, risk tolerance, liquidity needs, and consult a qualified financial professional before making investment decisions.