It’s been a busy and eventful week to say the least. President-elect Donald Trump is headed back to the Whitehouse for a second 4-year term, becoming the first former President to reclaim the office after losing an election bid since Grover Cleveland did so in 1892.

Equities had a bullish response to Trump’s win with the S&P 500 out to new all-time highs. With the US Presidency now settled, we examine our factor proxies to see what is changing in the US equity market’s leadership profile.

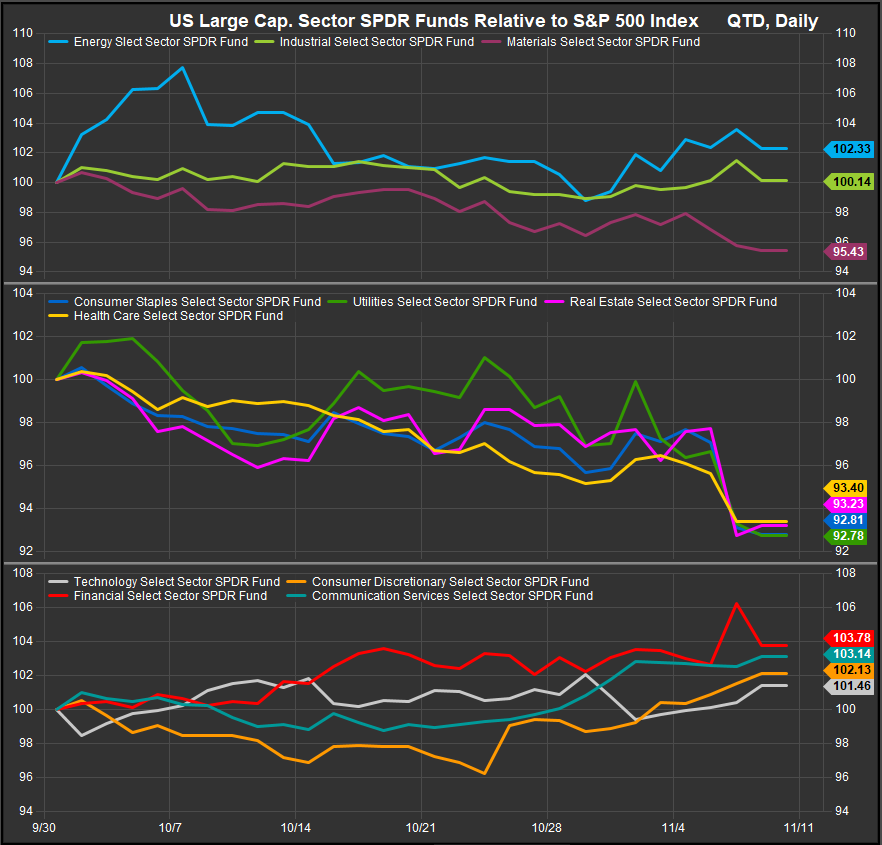

Sectors

The last time Donald Trump was elected president, cyclical stocks, led by Financials, raced out of the gate to large gains into year-end 2016. We have seen an echo of that in 2024, the question is whether there will be a 40+ day surge like there was then. The US sector relative performance chart shows a clear preference for historical upside exposures (chart, bottom panel) and selling in the lower vol., high dividend sectors (chart, middle panel) since the end of September. The election results swung stocks further into the direction of these trends on Tuesday. Our trend-following Elev8 Sector Model has us aligned with these offensive exposures as well as the Industrials and Energy Sectors. We are short the historically low beta side of the market and we aren’t seeing the technical strength needed to own the Materials Sector.

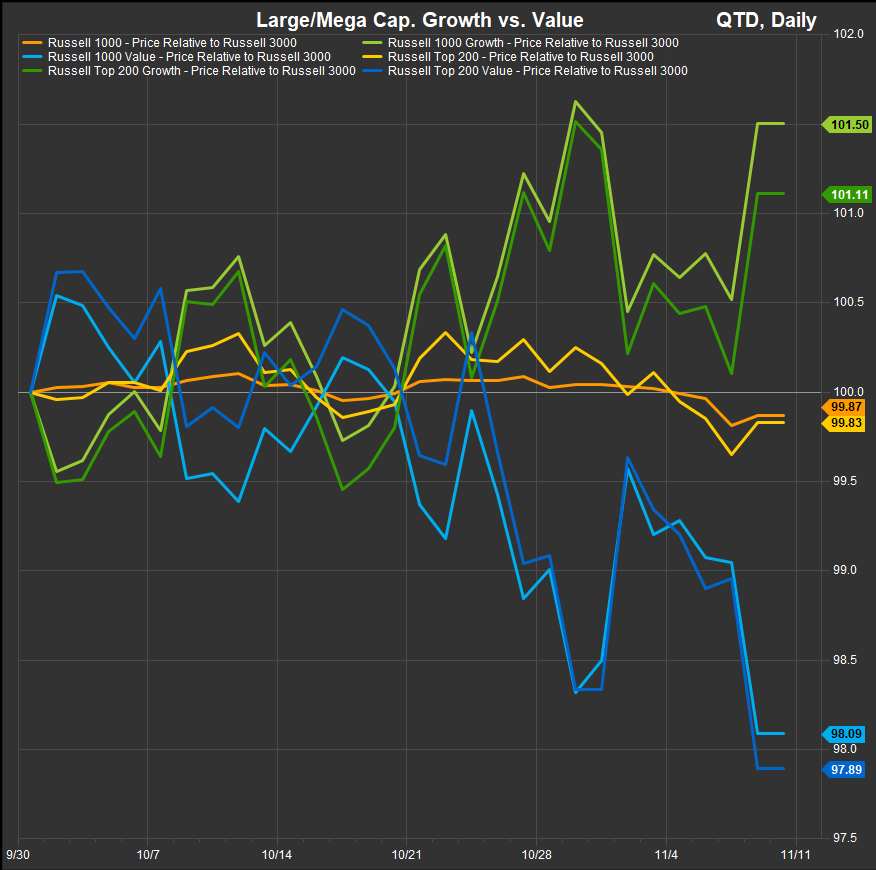

Large/Mega Cap. Growth Edging out Value in the Near-term

If you had asked us two weeks ago, we would have opined that a Trump Presidency would be a boon to Value stocks over Growth. It is early days, but those days have shown a preference for Large Cap. Growth stocks near-term. To be sure, there has been some improvement in Financials and Energy Sector performance, but low vol. Value has likely been a drag in the near-term. We would also point out that the spread is still pretty tight here.

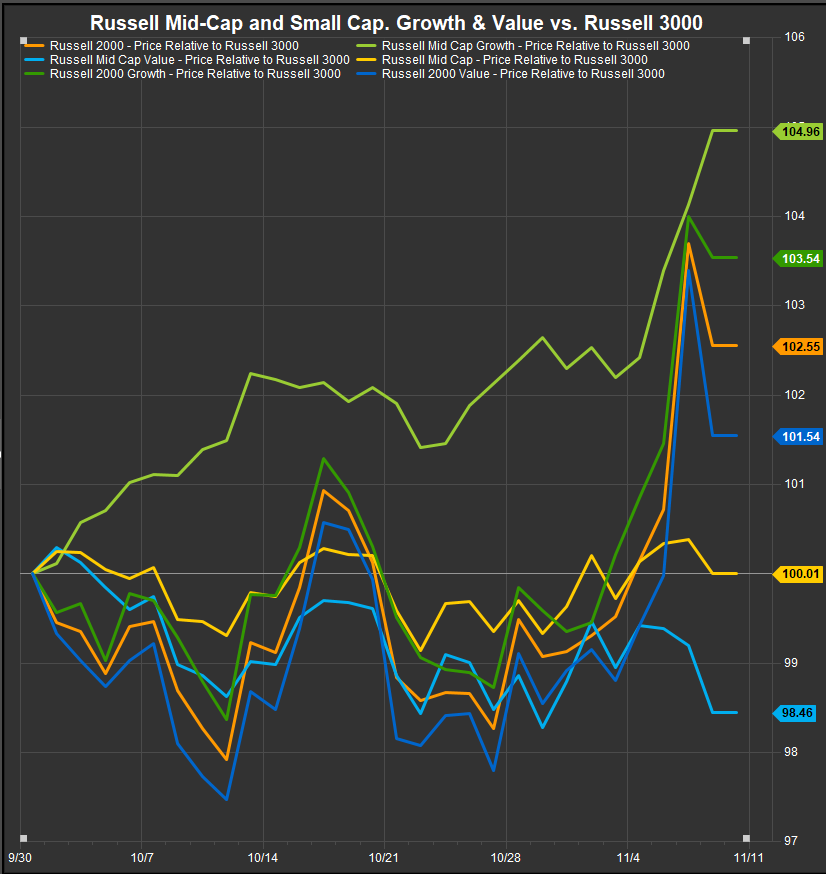

Small/Mid Stocks: Growth Emerging as Leadership?

The leadership profile appears to be changing in the Mid and Small Cap. tiers. Bifurcation between Growth and Value styles is starting to emerge. Throughout most of this bull market cycle (which we trace back to the first half of 2023) the Small/Mid space has been a scrum. Returns were tightly correlated regardless of style, and it seemed that investors were treating “SMID” equities as their own asset class. Now we are seeing some investor preference for Small and Mid-Growth emerge in the near-term. We are also seeing a near-term preference for Small Caps vs. Mid.

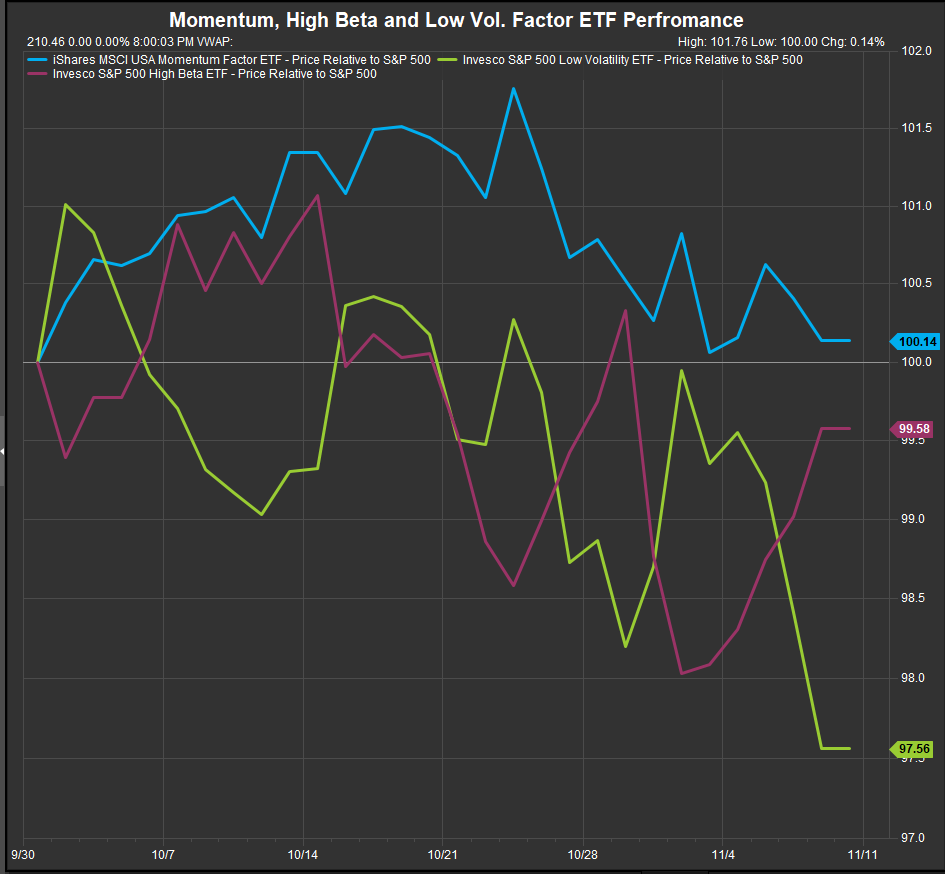

Momentum, High Beta & Low Vol: Low Vol. is being redeemed

One of the key takeaways of this cycle has been the persistent feedback loop between emergent optimism à rates move higher à emergent pessimism because rates moved higher. We are at a potential inflection point for this feedback loop. Rates have moved higher in the near-term along with equities. This is against the cycle’s pattern of positive correlation between stock and bond returns that has been with us throughout the current bull market cycle. If investors see Trumps restoration to the Presidency as a pro-economic event, they may be willing to bet on equities despite higher rates, at least in the near-term. That would be a change in psychology worth noting.

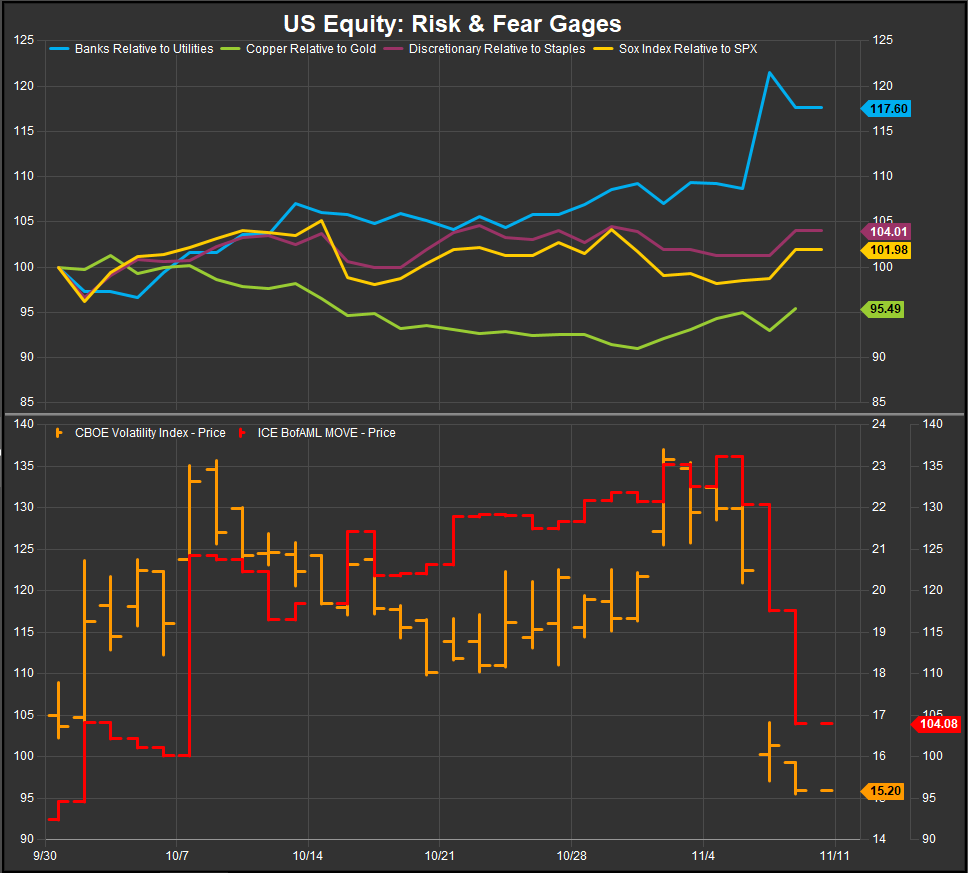

Risk On/Risk Off: Equity Risk-on Ratios Remain Constructive for the Bull, Volatility Diminishes on Election Results

Looking at our equity market risk gages, Banks have executed a sharp postive turn against Utilities while Semiconductors and Discretionary stocks remain in constructive patterns. The biggest takeaway on the chart below is the sharp reduction in the VIX and MOVE indices (chart below, bottom panel) which measure volatility priced into the stock and bond market through options activity. This is either dangerous complacency from investors, or bullish recognition. Given the overall picture shaping up, we are betting on the latter.

In Conclusion

Equity leadership has been fleeting since July, but the upward pressure has come off Commodities prices while rates have pushed higher regardless. With Commodities prices lower, Growth performance has improved and has an edge at present. The forward direction of rates will likely have a big impact on leadership. We’d expect a mix of defense (on inflationary recession fears) and Value (on inflationary growth scenarios) to outperform with rates rising. We’d expect Growth factor exposures to outperform if rates end the year on a 3-handle.

Data sourced from FactSet Research Systems Inc.