Factor Friday: October 11, 2024

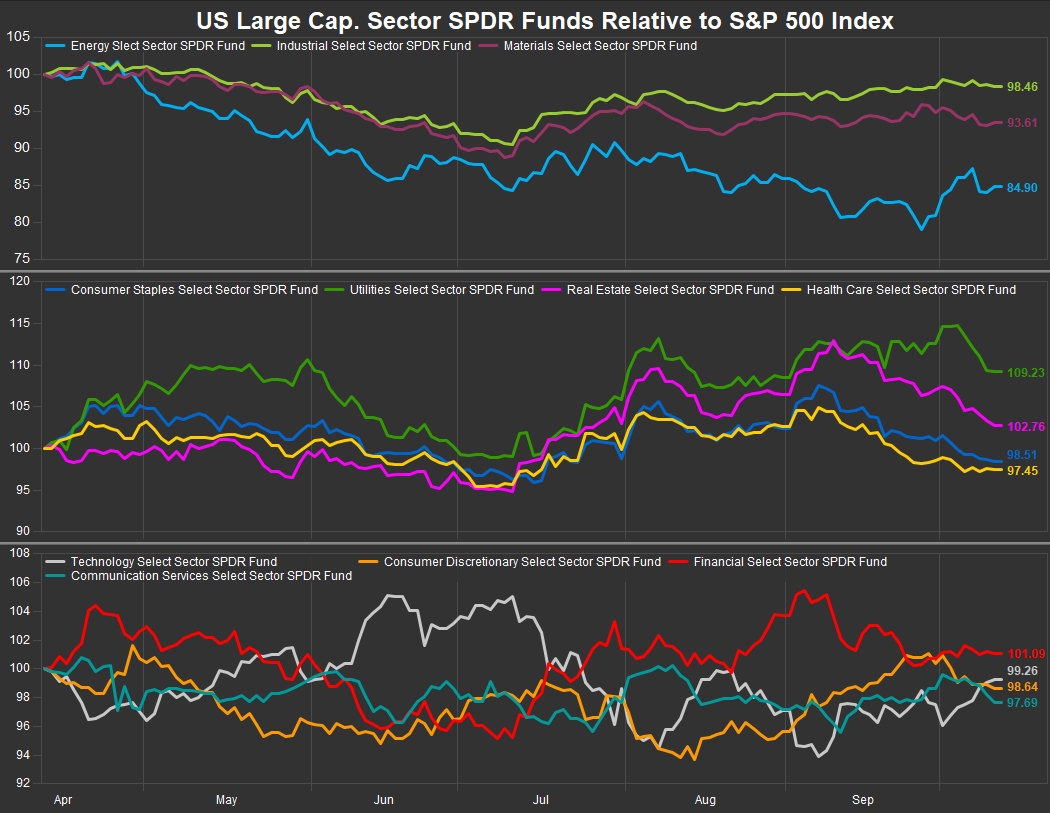

Despite the S&P 500 making a fresh all-time price high on October 9, sector leadership has been in rotation. The best performing sector over the past 6 months has been the Utilities Sector despite the S&P 500 printing numerous new highs. The chart below shows Large Cap. GICS Sector ETF’s relative to the S&P 500 over the past 6 months. Performance spreads have tightened in October with Technology and Energy sectors firming and the summer’s winners (Financials, Utilities and Real Estate) retracing relative gains.

In the past month, the Energy Sector has been leadership and lower volatility sectors (chart below, middle panel) have seen profit taking/lagging performance. Escalating Mid East tensions have kept the upwards pressure on Crude prices though they remain shy of our trend-change indicators at this point.

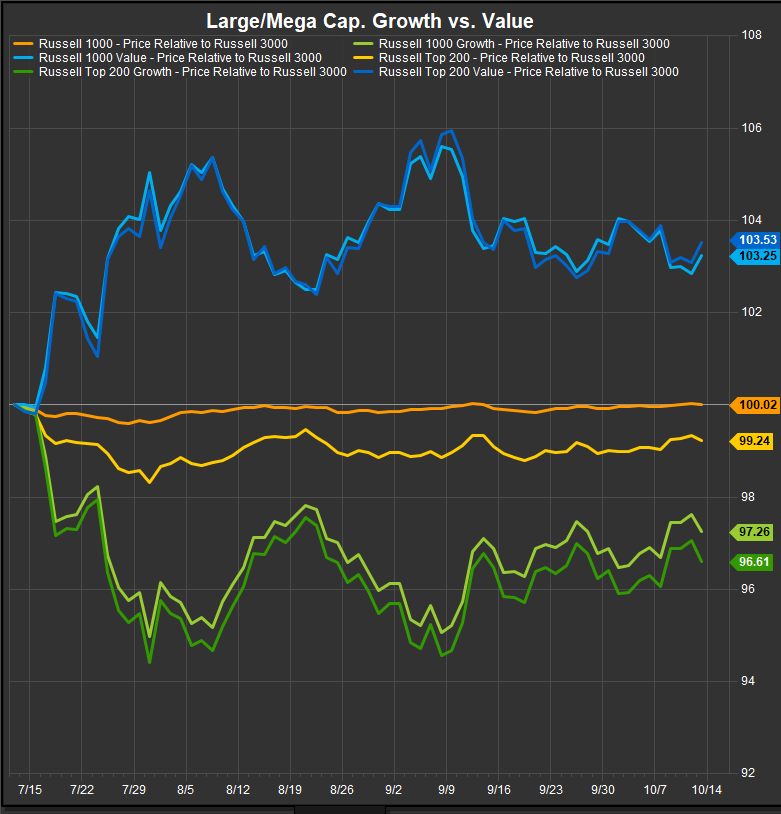

Large/Mega Cap. Growth Still Upside Leadership

Looking at Large and Mega-Cap. Growth vs. Value in the chart below, the patterns developing over the past 3 months are instructive. Growth has lagged since making highs on July 15th, but the basing (bottoming) pattern in the Growth relative curves is more encouraging than the distributional look from Value. New relative highs are positive signal in our trend following work. New relative lows are correspondingly negative. We are looking at the pivots made on August 20th and July 23rd to give us confirmation, but we are positioned for Growth exposures to follow through to the upside based on what we see at present.

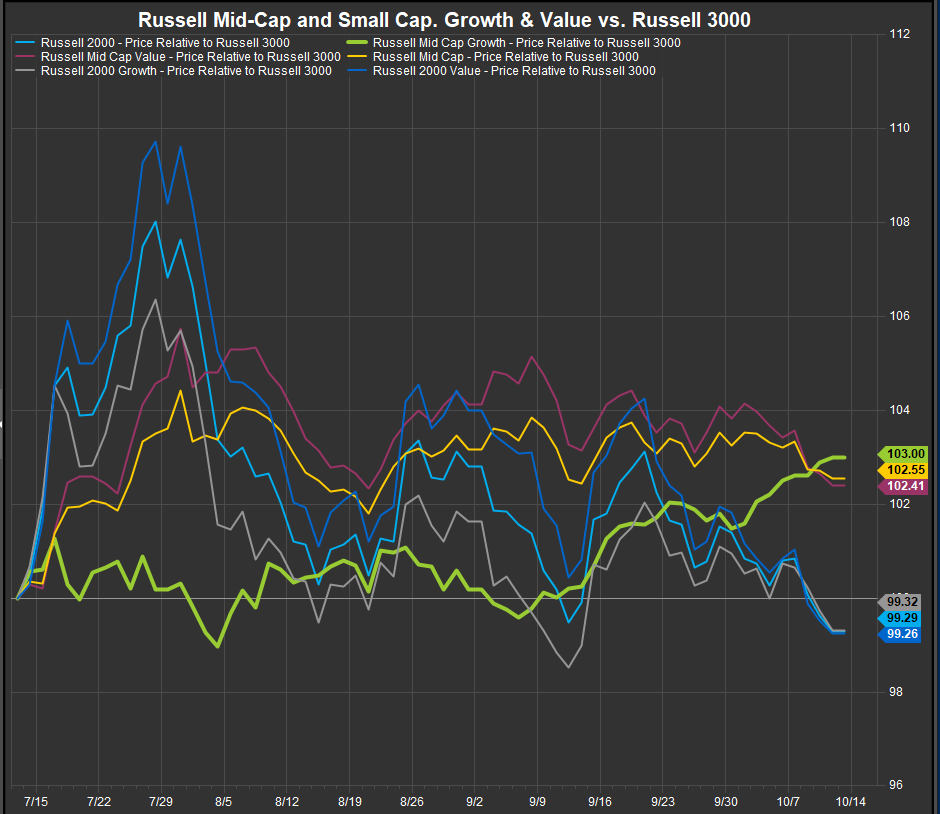

Small/Mid Stocks: Mid Cap. Growth improving near-term

In contrast to the Large/Mega Cap. space, the Small/Mid tiers of the US equity market continue to be a scrum. As the chart below shows, dispersion of returns over the past 12 months has been narrow and highly correlated. Mid-Cap. Growth has been the only cohort trending positively over the past 3 months.

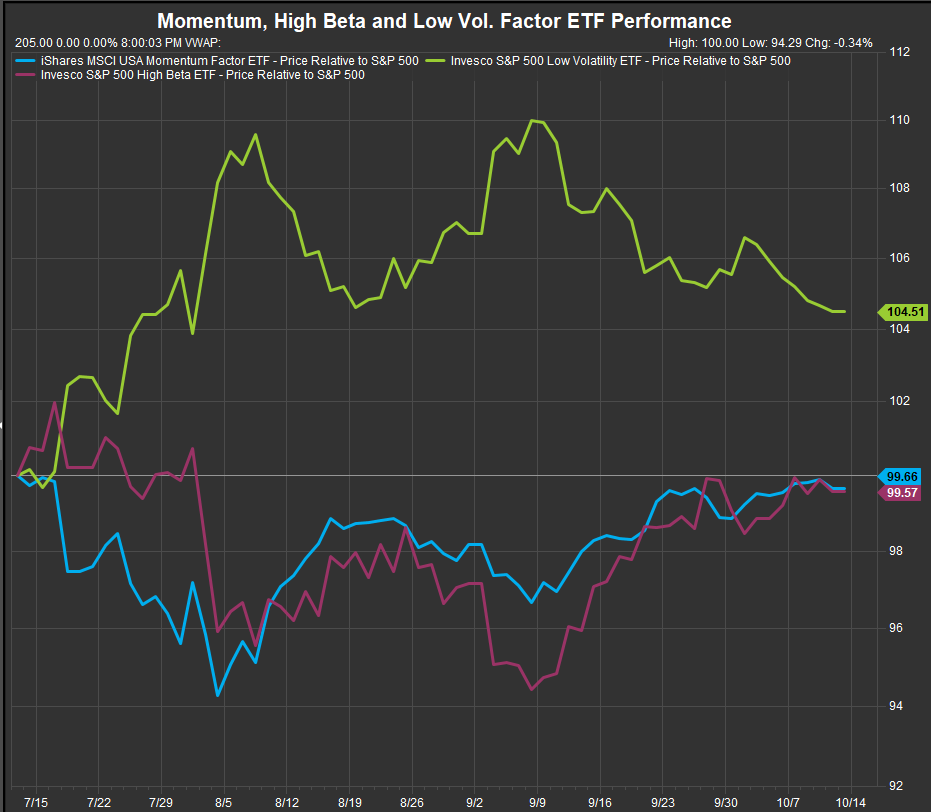

Momentum, High Beta & Low Vol: Min Vol. Continues to lag near-term

Reviewing our key factor ETF’s, we see low vol. relative performance peaking in early September and giving way to high beta. Momentum has also improved but hasn’t made a new 3-month high. We are looking for that to confirm the market’s renewed enthusiasm for Tech and Growth stocks. With commodities showing signs of life, we are getting an expected pause in momentum as investors try to gage the latest developments. We are paying close attention to commodities at the moment, but we need to see more sustained buying in the near-term to trigger our long position entry signals for XLE. If we do hit them, we would likely fund a position in our sector rotation portfolio by selling some XLY and some XLRE to cover our current short in XLE.

Risk On/Risk Off: October has seen Volatility increase

The MOVE Index recently made a new high which shows up as potentially significant on a longer-term 2yr chart. The VIX is still under early September highs which is our threshold for an upside break-out. However, when looking at our four risk on/risk off gages in the top panel we see that three of them have been constructive since the early August low for US equities. Banks relative to Utilities has firmed in favor of Banks, while the Copper/Gold ration has weakened. Our advice is to watch the Commodities prices closely. We think any significant rotation way from Growth leadership would be led through rising rates and higher commodities and crude prices. To be clear, this isn’t our base case, but it is the bearish alternative scenario remain the most concerned about at present.

From a more tactical perspective, October is historically a bearish month from the lens of seasonality. Historically the middle of the month is the pivot. Being in an election year, there is obviously plenty of potential for near-term surprises.

In Conclusion

Equity leadership has been fleeting since July and we are seeing an uptick in volatility, particularly as interest rate markets try to digest the implications of a dovish Fed, an escalating situation in the Middle East and a Presidential election. Not to mention a ruinous hurricane season in the Southeastern US. Factor exposures are aligning with consolidation, but we evaluate the technical condition as supportive of bullish positioning over the intermediate term into year end.

Data sourced from FactSet Research Systems Inc.