Throughout 2024 we have highlighted fundamental and style factors that have been thematic drivers of sector rotation. Since the current bull market’s inception in 2023, Meg Cap. Growth has been the dominant leadership cohort along with the momentum factor. Corrections in the market have typically benefitted a broad range of other factors and styles, while moves to new highs are typically driven by Mega Cap. Growth. With the S&P 500 making new all-time highs in September, let’s take a look at these performance trends and see if anything has changed from a factor leadership perspective.

Commodities linked sectors and themes are finally in focus this week as fighting in the Middle East has escalated between Israel and Iran-backed Hezbollah. Combined with the onset of stimulative interest rate policy, there is now a potential for demand pull from a re-accelerating economy and a supply shock if fighting continues to escalate between Israel and Iran.

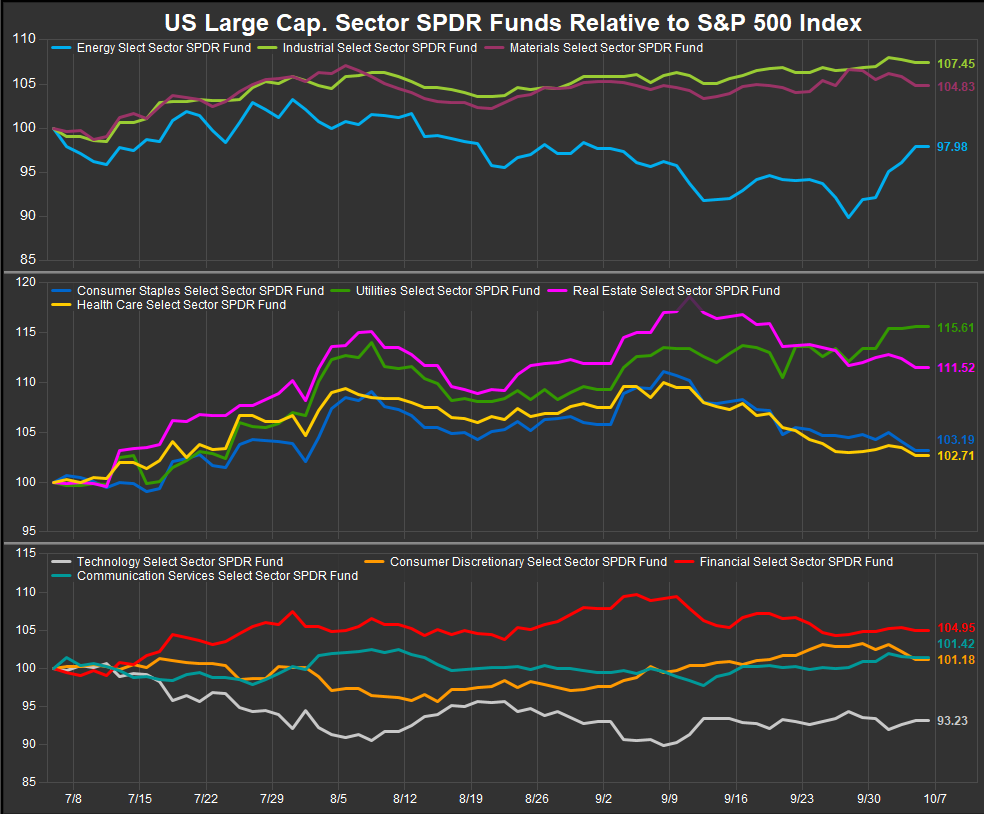

The results of the Mid East turmoil have been a sharp near-term rally in Energy prices and Energy stock prices. A look at 3-month sector relative performance in the chart below illustrates the dynamic. Outperformance has broadened out as 9 sectors have beaten the S&P 500 over the past 3 months. The two laggards at present are Technology as proxied by the XLK and Energy (XLE). In the very short-term we have seen Staples, Healthcare, Real Estate and Discretionary roll over as Energy has put a potential bullish reversal on the chart.

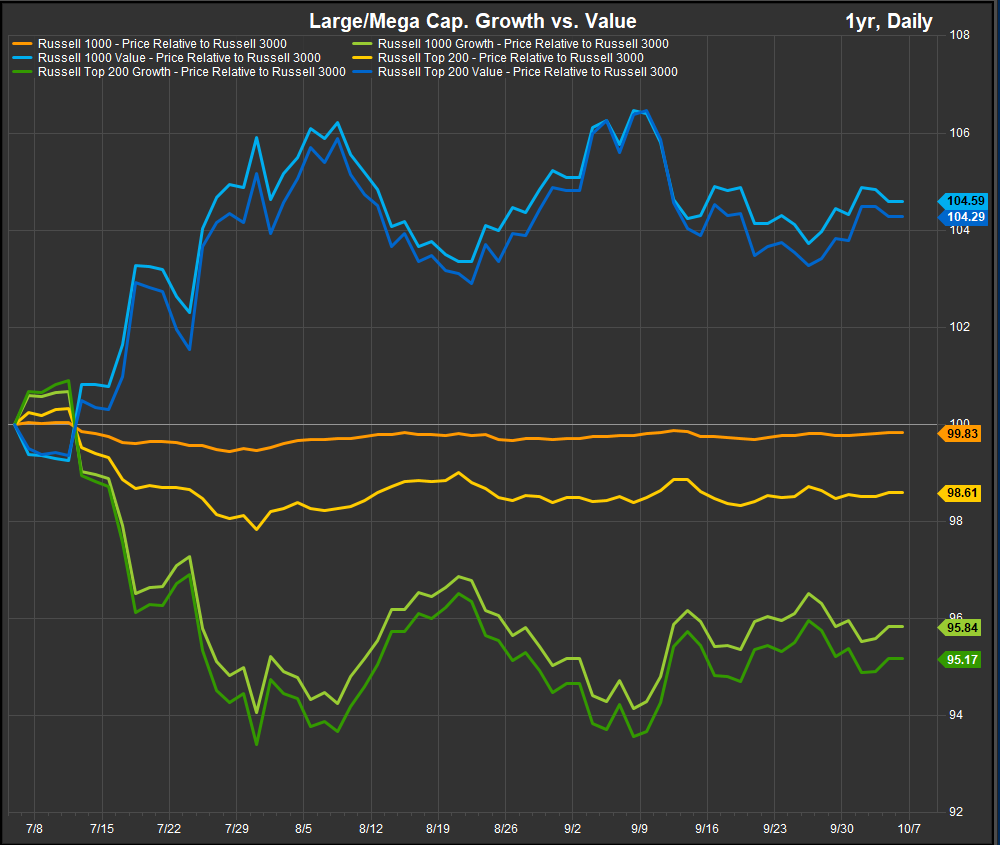

Large/Mega Cap. Growth Still Upside Leadership

Looking at Large and Mega-Cap. Growth vs. Value in the chart below, we can see Mega Cap. Growth and Value as proxied by the Russell Top 200 Growth and Value Indices have both lost momentum in the near-term. This is likely a pre-election pause as, generally, equities have churned through leadership themes since July. We continue to believe that the path of commodities prices from here will dictate Growth or Value leadership. Rapidly rising commodities prices are likely to spur inflation/recession positioning while we prefer the outlook for Large and Mega Cap. Growth exposures if commodities prices stay contained.

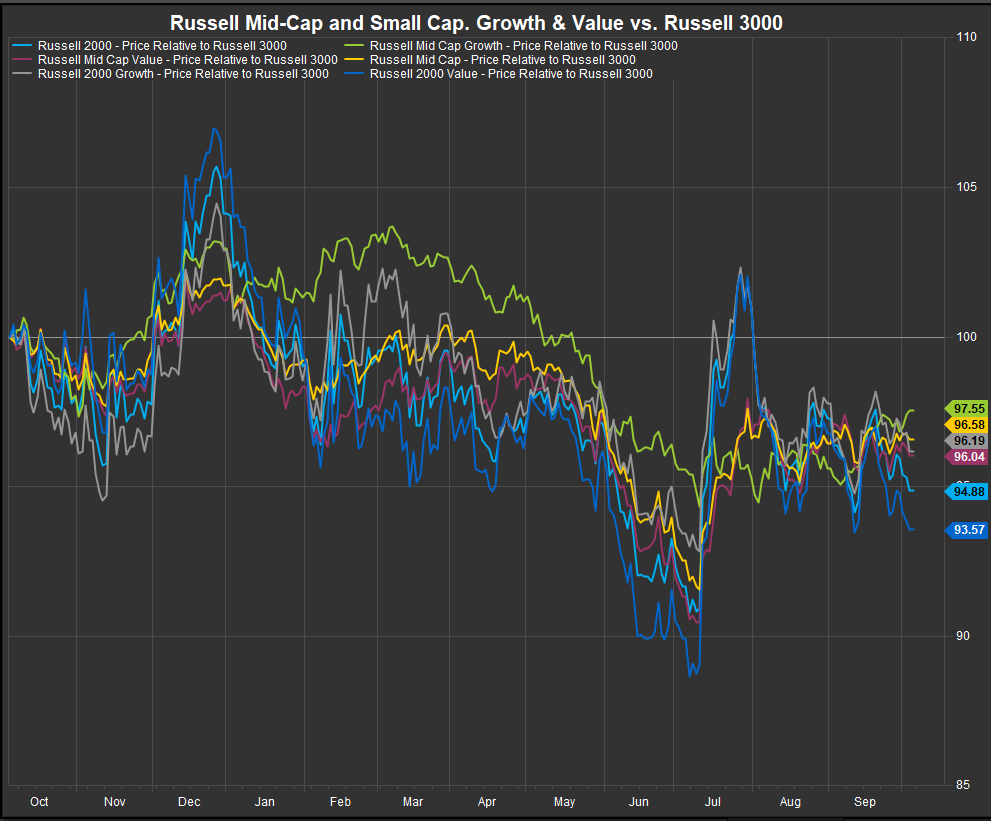

Small/Mid Stocks still trade together

In contrast to the Large/Mega Cap. space, the Small/Mid tiers of the US equity market continue to be a scrum. As the chart below shows, dispersion of returns over the past 12 months has been narrow and highly correlated. Mid-Cap. Growth has been the marginal outperformer YTD whhile Small Value has been the laggard, but the biggest message is that all continue to trade together.

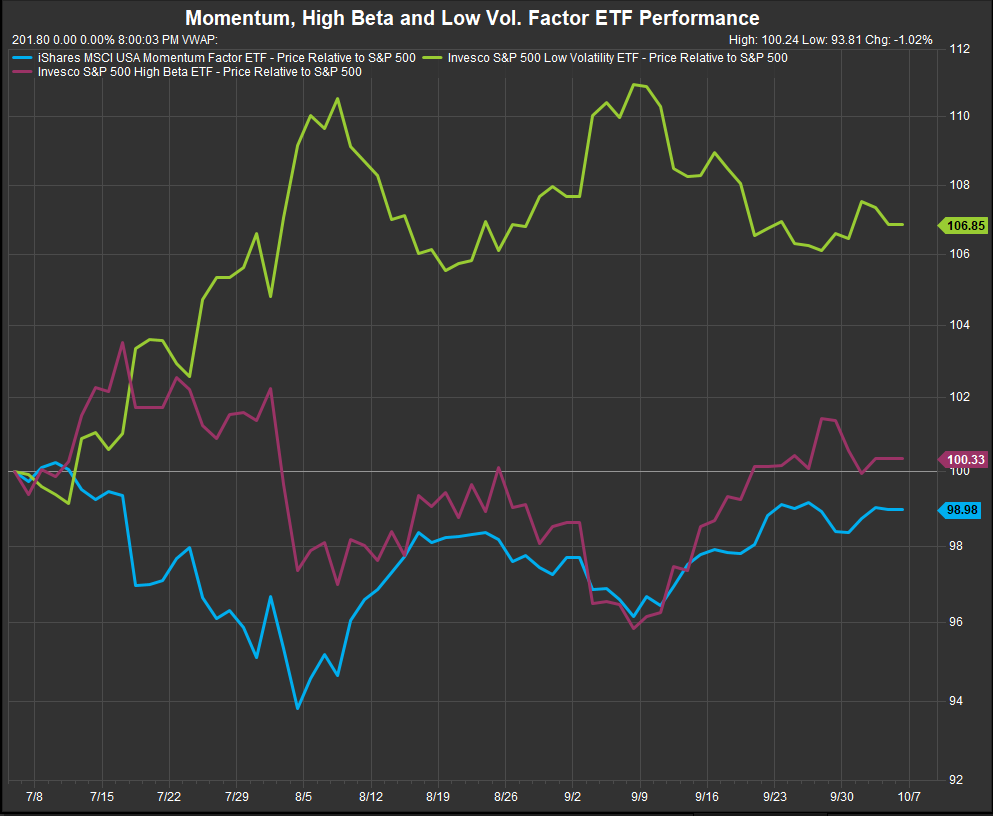

Momentum and High Beta pausing to reassess:

Reviewing our key factor ETF’s we see low vol. relative performance peaking in early September and giving way to high beta. Momentum has also improved but hasn’t made a new 3-month high. We are looking for that to confirm the market’s renewed enthusiasm for Tech and Growth stocks. With commodities showing signs of life this week, we are getting an expected pause in momentum as investors try to gage the latest developments. We are paying close attention to commodities at the moment, but we need to see more sustained buying in the near-term to trigger our long position entry signals for XLE. If we do hit them, we would likely fund a position in our sector rotation portfolio by selling some XLY and some XLRE to cover our current short in XLE.

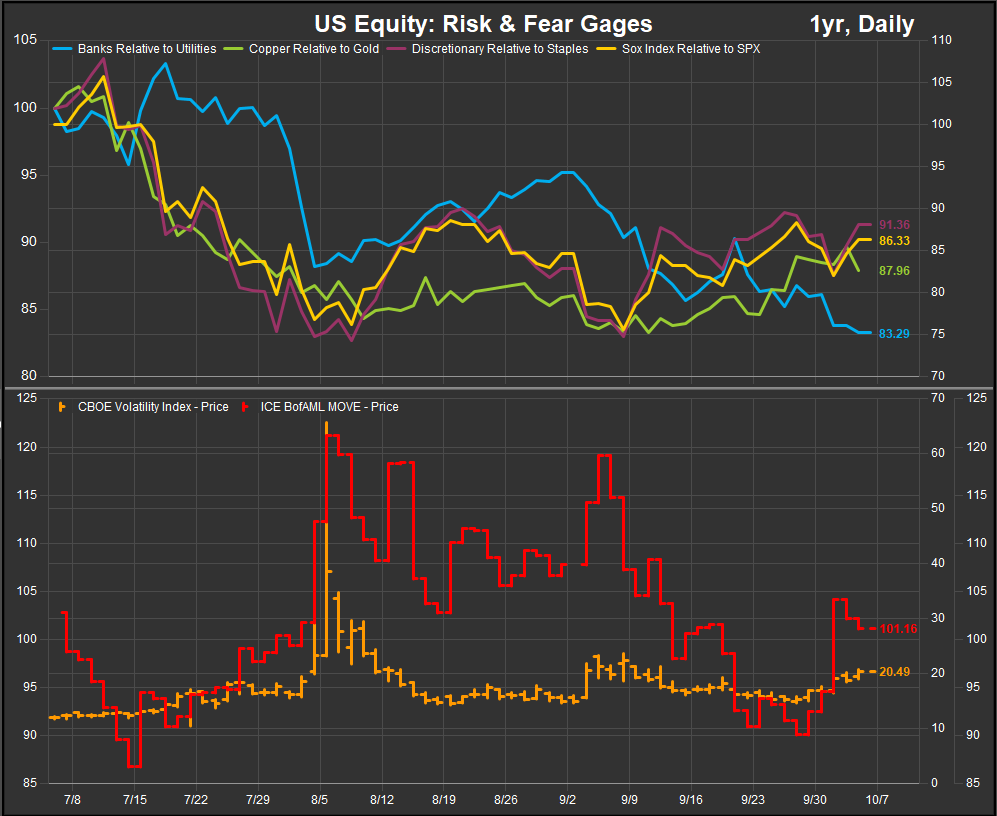

Risk On/Risk Off proxies have switched to favoring Risk On

We are seeing an uptick in volatility in both the stock and the bond market to go along with the recent sharp move higher in Energy prices. However, when looking at our four risk on/risk off gages in the top panel we see that three of them have been constructive since the early August low for US equities. Only the Banks/Utilities ratio has been negative while Semiconductors have firmed vs. the broad market, Discretionary has outperformed Staples and Copper has marginally improved performance vs. Gold during the last 3-months.

In Conclusion

Conflict in the Middle East has put a pause on the near-term enthusiasm around policy easing that developed in September. The 104 level on the Bloomberg Commodities Index and $77 on the WTI continuous contract are levels we’re watching to gage a more sustained bullish reversal for commodities exposuress. We balance that concern against the long-term bull trend in the US which is still intact and now has the Fed supporting economic outcomes.

Data sourced from FactSet Research Systems Inc.