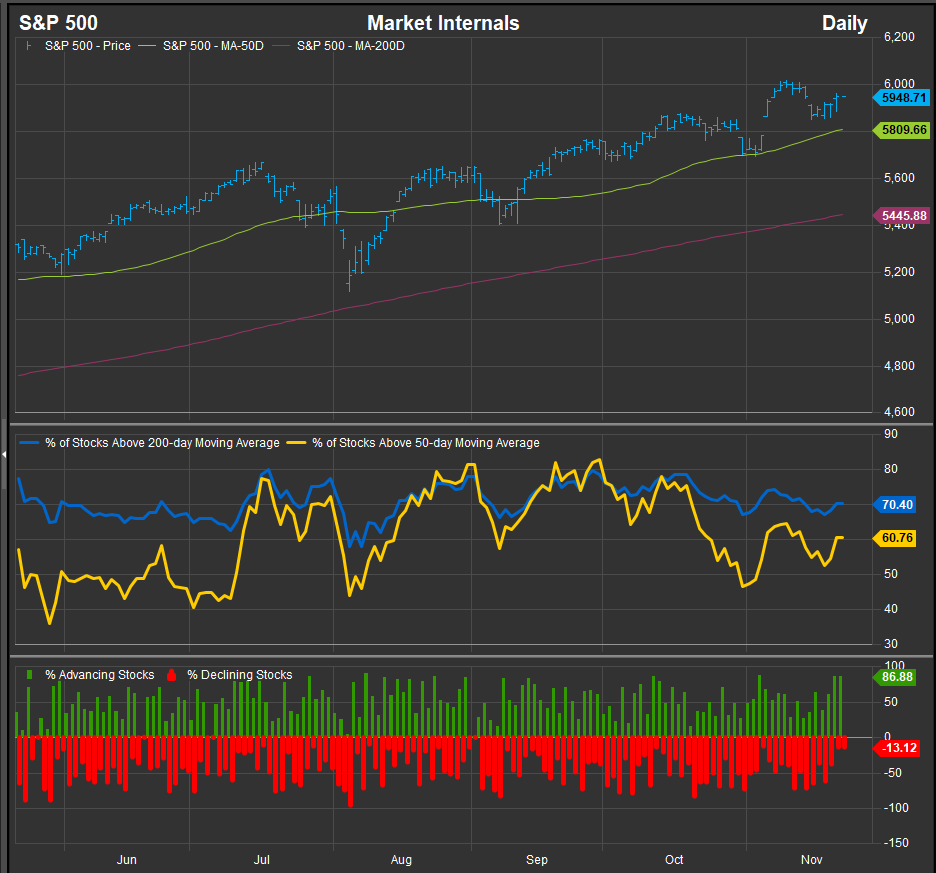

The S&P 500 remains firmly ensconced in its long-term uptrend. However, interest rates as proxied by the US 10yr Treasury yield have backed up to near-term resistance and the pace of the equity advance has cooled since July with momentum gages showing a negative divergence to price.

What’s of slightly more concern is the negative divergence in equity breadth measures since the end of September. The chart below illustrates the dynamic. The top-line trend for equities has powered on, but less stocks within the index are being pushed above their 50 and 200-day moving averages, suggesting the potential for a correction is creeping higher. Given the inflationary concerns over the incoming Trump Administrations plans to deregulate and implement Tariffs, these technical conditions are unsurprising.

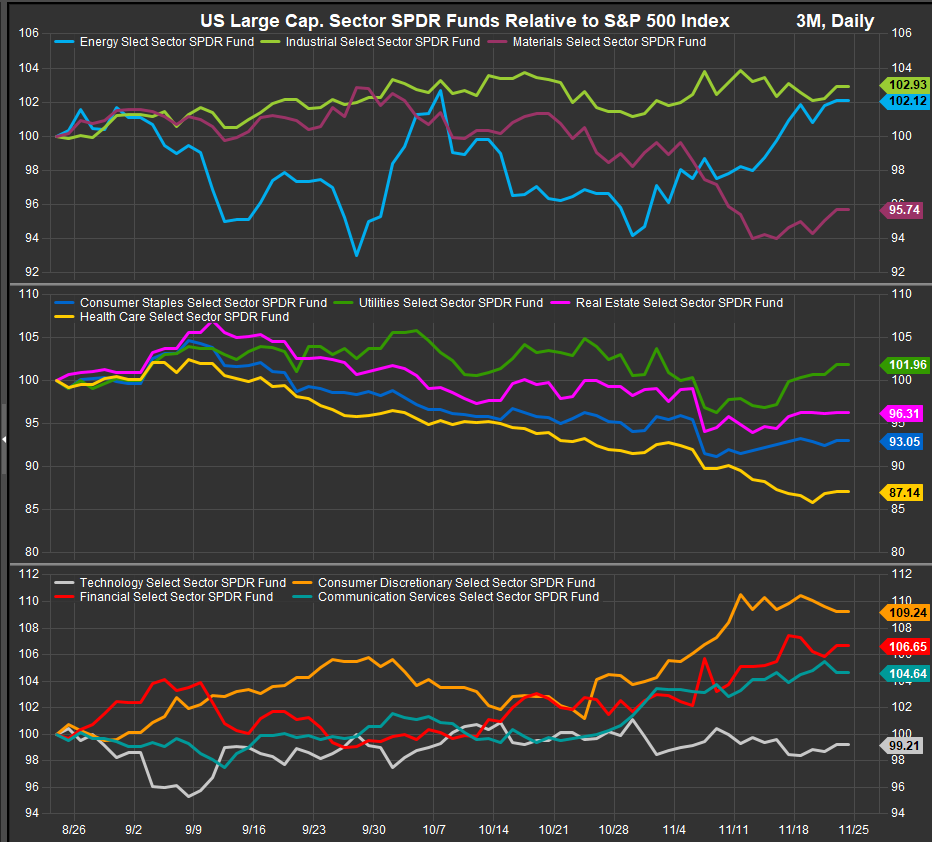

Looking at our suite of factors we are seeing continued assertiveness in the domestic Small/Mid trade and a rotation in Large Cap. sector leadership away from Technology and towards cyclicality and commodities linked sectors in

Sectors

NVDA posted in-line earnings this week which didn’t move the needle for the Bull. Demand for Technology Sector shares has remained tepid with a preference for cyclicality evident over the past 3-months. In the very near-term concerns about rising rates and inflationary potential have resulted in some rotation back into the lower vol. sectors, Utilities, Real Estate and Staples, though as a theme min vol. remains the laggard.

The sector relative performance chart is notable for the Tech Sector flat-line over the past 3-months (chart below, panel 3). Discretionary, Financials and Comm. Services score more attractively in our process among historical bull market exposures. The Energy Sector continues to accrue buyer interest in the near-term while Industrials have been steady. Healthcare and Materials Sectors are clear laggards at present. However, the Healthcare Sector could be a “buy low” target if a sustained defensive rotation takes hold. Behaviorally, the type of fear that sparks defensive rotations in equity typically has investors avoiding overbought stocks and favoring oversold stocks because of the “profit taking” motive that effects the former group when markets come under stress.

Large/Mega Cap: Value Performance Improving Near-term

Over the past 3 months, Growth stocks have fended off a challenge from Value for style factor leadership. With rates rising, Large Value stocks have established equilibrium in November and the performance spreads have tightened to wthin 200 basis points of each other on a 3-month basis.

Large Cap. Growth and Value remain completely negatively correlated over the trailing 12-month period in sharp contrast to small and midcap counterparts.

Small/Mid Stocks: MidCap Growth has Surged

Small/Mid Stocks in aggregate have gained in the near-term and the longer-term setup offers some “catch-up” potential vs. Mega Cap. as the latter cohort has been leadership throughout a majority of the past 2 years. The recent surge in MidCap Growth comes in the context of a multi-year underperformance trend, so a bullish reversal with strong momentum has potential for more upside follow-through here. The 4-year weekly chart below shows the context of long-term underperformance.

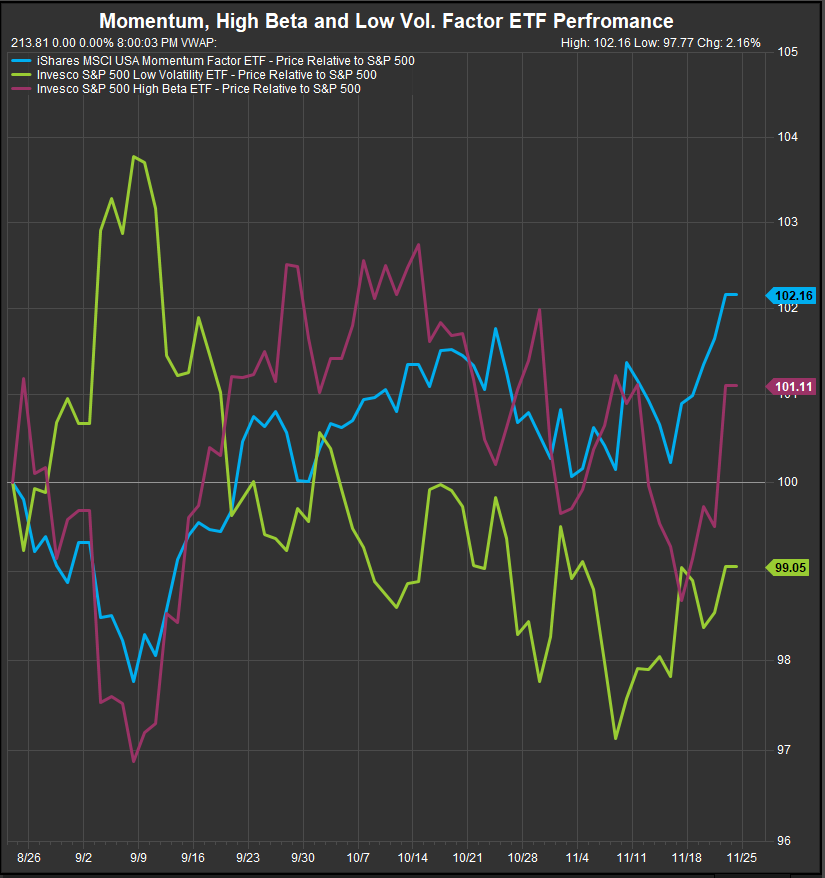

Momentum & High Beta have the Edge over Low Vol.

Momentum has maintained an edge despite the Tech Sector stalling out since July. High beta stocks have rallied in the past week as Discretionary and Energy Sector shares have outperformed while the Tech Sector continues to consolidate and the FTC looks into busting up monopolies at Alphabet Corp.

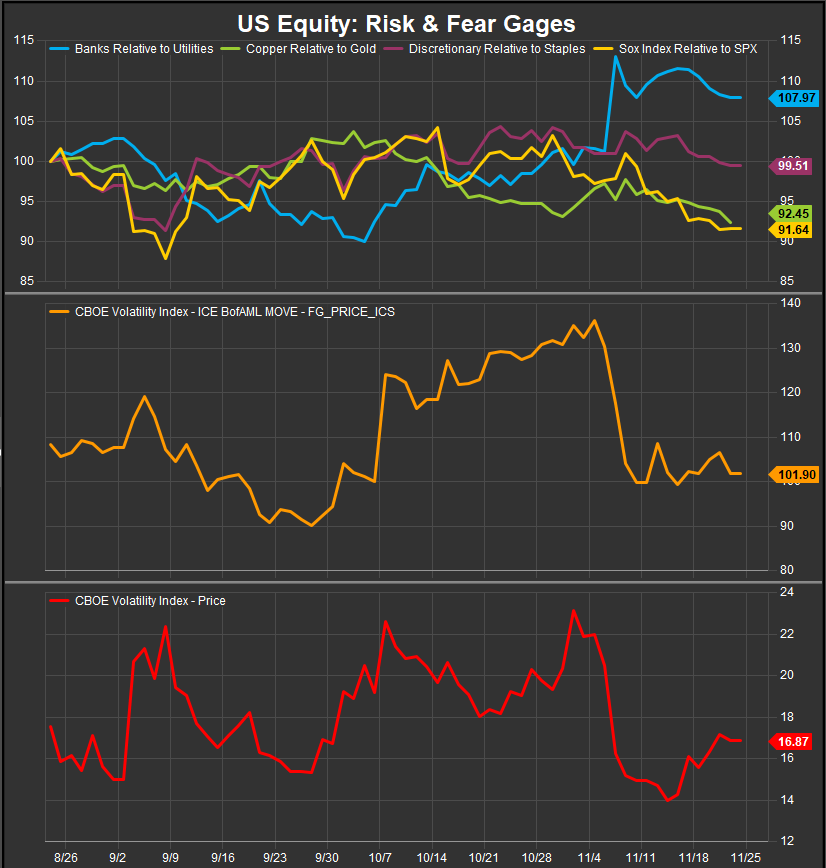

Risk On/Risk Off: Semiconductors and Copper/Gold hint at Deteriorating Risk Appetite

Risk Appetite indicators have pulled back after surging post-election. Semiconductors and the Copper/Gold ratio are looking soft despite stock and bond volatility indices (chart below, bottom panel) at the low end of their recent ranges. Investor optimism post-election needs some new catalysts.

In Conclusion

Equity leadership has been fleeting since July, but the upward pressure has come off Commodities prices while rates have pushed higher regardless. We are seeing a loss of momentum in the Technology Sector and a corresponding near-term sluggishness in Growth shares vs. Value. Interest rates will likely determine the course of style leadership from here. If they remain elevated we could see Value and Min Vol. factors taking over leadership from Growth into 2025. If prices and performance continue on their current trajectory, we project to move to an underweight position in the Tech Sector for December as momentum and breadth have narrowed there.

Data sourced from FactSet Research Systems Inc.