The S&P 500 made its 53rd daily new all-time high of 2024 this past week and breached the 6000 level for the first time in history. For the time being, the Fed has executed a policy shift without hindering the bull market advance for US equities. Ten and a half months through 2024, the bull remains in control of the tape. Based on our risk gages, investors are bullish but not overheated with exuberance.

We have seen a subtle but clear change of leadership over 2024. The Technology Sector and the Semiconductor Industry have been in distribution since July. However, from a factor perspective, Growth and Momentum continue to have a performance edge, despite rotation within those factors.

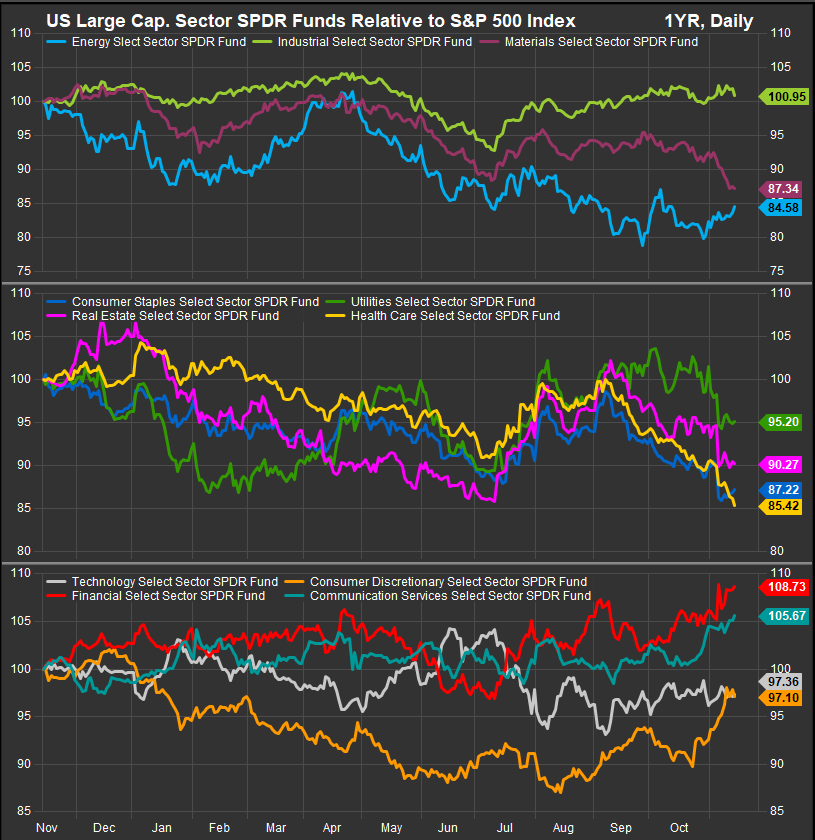

Sectors

A dovish pivot from the Fed and the election of the Republican ticket for President have rejuvenated investor’s risk appetites after a summer rotation towards lower vol. sectors. As mentioned above, Technology sector shares haven’t been able to make significant headway in 2024 relative to the S&P 500. Instead, leadership has come from Financials and Communications Services sectors, while the Consumer Discretionary sector has been a clear beneficiary of the Fed’s stimulative moves.

The sector relative performance chart below shows min vol. sectors (middle panel) clearly in retreat over the past 2 months.

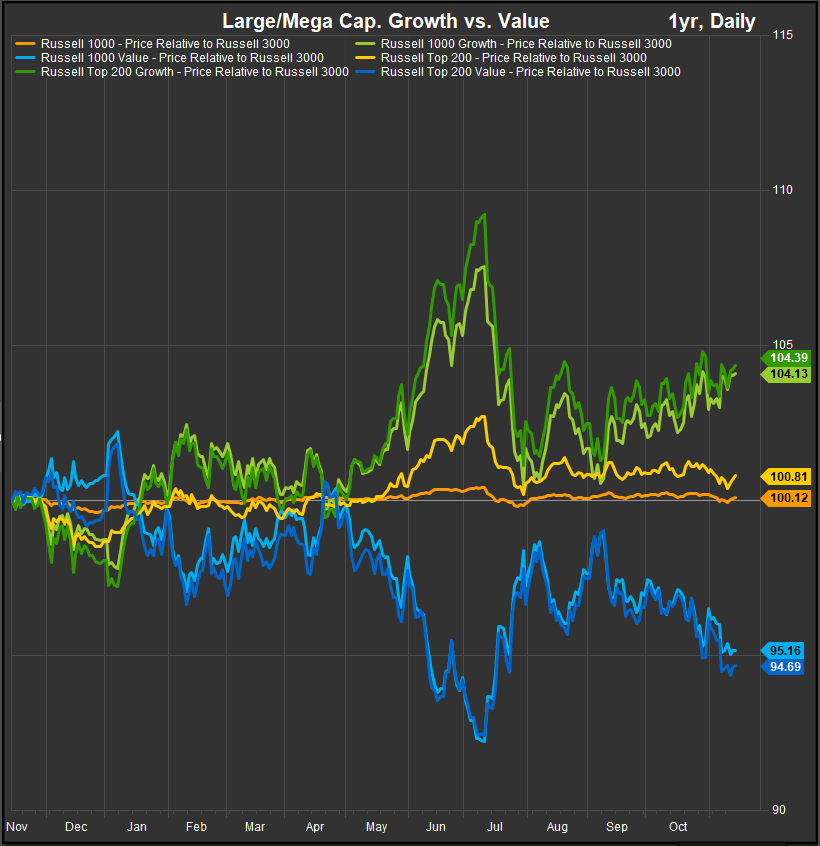

Large/Mega Cap. Growth Continues to be Leadership over the Intermediate term

Over the past 3 months, Growth stocks have fended off a challenge from Value for style factor leadership. This has happened despite the near-term back up in US Treasury Yields. We would continue to favor Growth over Value while commodities prices continue to languish.

It almost goes without saying, but Large Cap. Growth and Value remain negatively correlated over the trailing 12-month period in sharp contrast to small and midcap counterparts.

Small/Mid Stocks: Growth a Persistent Edge Here as Well

Correlation remains positive, but Growth has maintained a slight edge in the Small/Mid space all year. The past week has seen some profit taking, but we’d expect some accumulation into year-end given the improvement in risk-on gages near-term.

Momentum, High Beta & Low Vol: Investors Shunning the Tails of the Risk Curve

Momentum has maintained an edge despite the Tech Sector stalling out since July. Both our high-beta and low vol. proxy ETF’s have underperformed in the 2nd half of 2024. This likely has to do with the resilience of the Mega Cap. Growth trade even as it migrates around sectors.

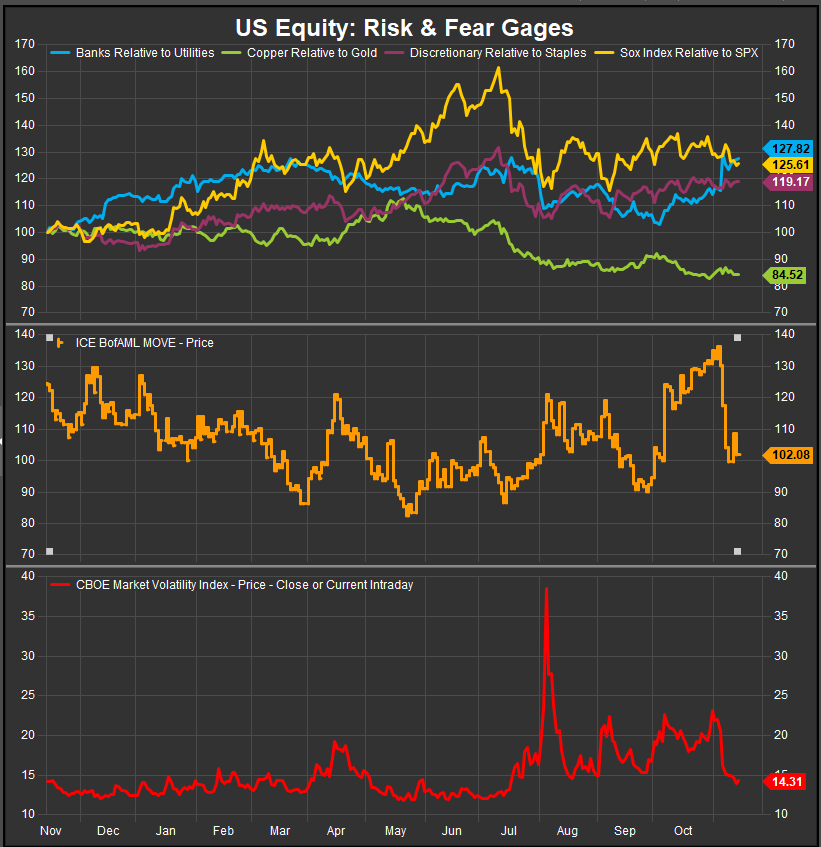

Risk On/Risk Off: Equity Risk-on Ratios Remain Constructive, Banks have Broken-out vs. Utilities

Looking at our equity market risk gages, Banks have executed a sharp positive turn against Utilities while Semiconductors have struggled for convincing upside follow through after their summer pull-back. Copper vs. Gold reflects the continuing malaise in Commodities prices while Discretionary stocks have improved vs. Staples.

Equity and bond Volatility proxies, the VIX and MOVE indices have collapsed towards lows for the year.

In Conclusion

Equity leadership has been fleeting since July, but the upward pressure has come off Commodities prices while rates have pushed higher regardless. With Commodities prices lower, Growth performance has improved and has an edge at present. Rates have stayed above the 4.4% level on the US 10yr Yield and we continue to monitor that situation closely. For the time being the bull is in control.

Data sourced from FactSet Research Systems Inc.