We wish everyone a happy 2025 as we get underway with our first Factor Friday Report of the year. Equities ended 2024 on a sour note with the S&P 500 price consolidating below its 50-day moving average to start 2025. We note an interesting technical setup has developed since the price gap higher on election day, November 5th. The chart below shows near-term support informed by that level which is 5785.55. The old heads of technical analysis will tell you that “all gaps are filled” and we could see that being the case during the current correction which is near oversold conditions on the RSI study (chart below, bottom panel). We expect the support zone for equities to reside between the 5651 level which coincided with the mid-year highs of 2024 and the 5785.55 level from election day.

10yr US Treasury Yields have pivoted higher since December 9 and recently made a new near-term high above the 4.6% level. The level of the 10yr yield will be pivotal in 2025. Since 12/23, the 10yr yield has been in consolidation, but any move higher would likely shake investor confidence in the Growth trade and imperil the bull trend. The chart below shows the MACD and RSI studies rolling over from overbought conditions as the yield consolidates near recent highs.

Sectors

Sector performance has shown an expected near-term tilt towards Defensive Sectors while the Consumer Discretionary sector has seen the heaviest selling into year end. The Energy Sector has shown signs of life while Industrials and Materials remain somnolent. The Tech Sector continues to drift sideways since mid-year 2024. If rates resolve their current consolidation higher, we could see increased selling in Growth focused sectors like Discretionary, Info Tech. and Comm. Services, but with commodities prices weak and higher rates cooling down the housing market, that isn’t our base case scenario.

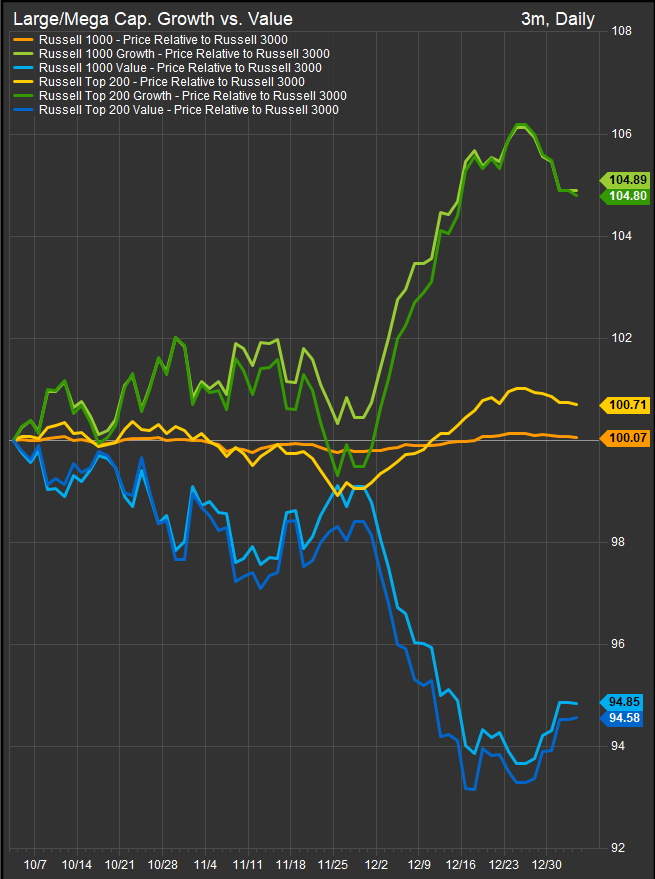

Large/Mega Cap: Growth stretched near-term, likely to give back gains if rates keep rising

Large Cap. Growth opened up a wide spread vs. Value into mid-December. Some retracement was always likely, but we remain aligned with Growth exposures and expect buyers will eventually accumulate this pull-back.

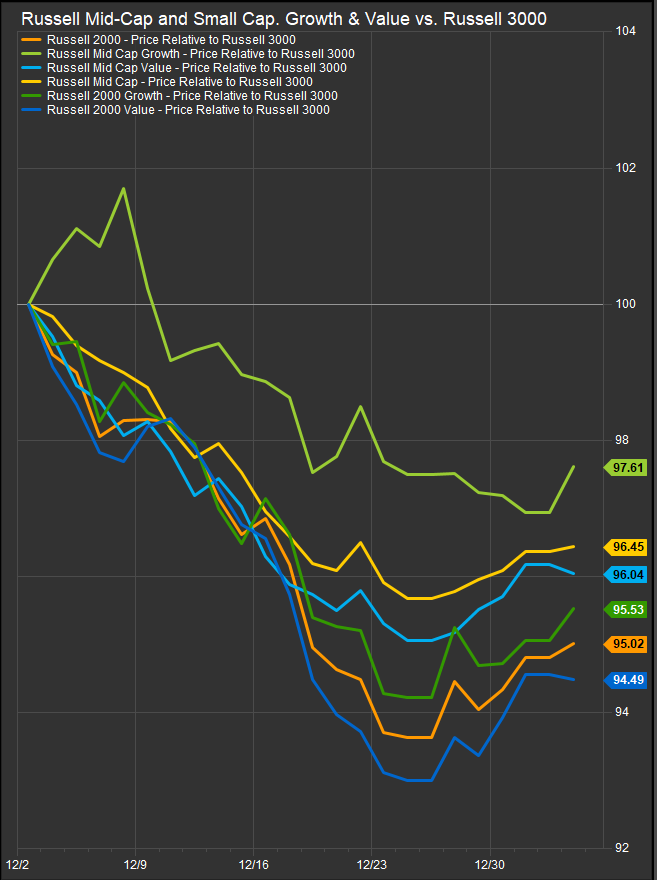

Small/Mid Stocks: Trading like a block over the past 3-months

We noted in previous reports that small/mid Growth and Value cohorts were back to trading as a block in December. The year-end sell off has seen the block inflect higher. We would expect this to continue if Mega Cap. Growth remains under pressure as the “Growth vs. Value” trade has morphed into the “Large Cap. Growth vs. Everything Else” trade.

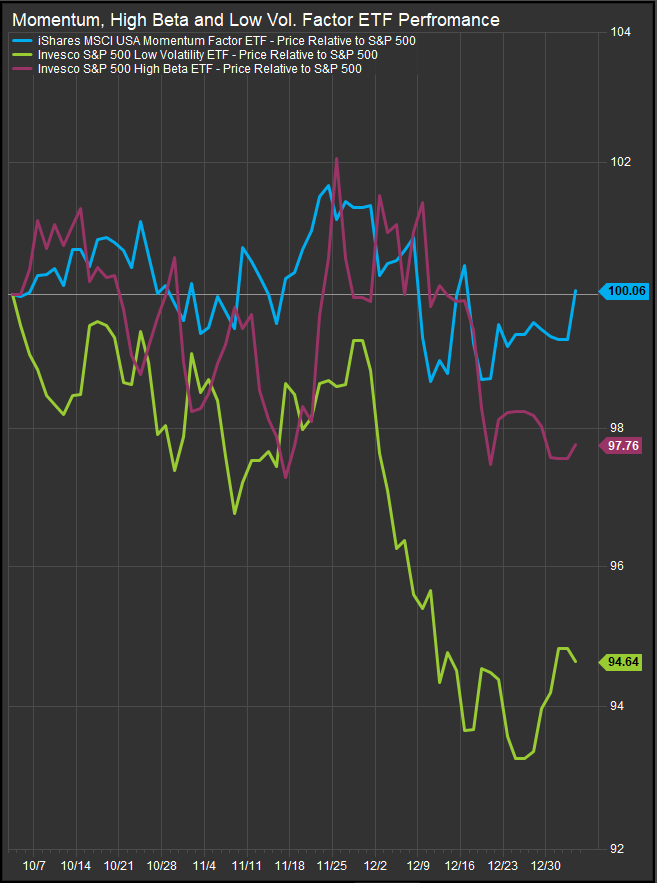

High Beta, Low Vol and Momentum

Both high beta and low vol. tracking ETFs have underperformed since the beginning of December. Momentum has held up the best as proxied by the iShares MSCI USA Momentum Fund (MTUM).

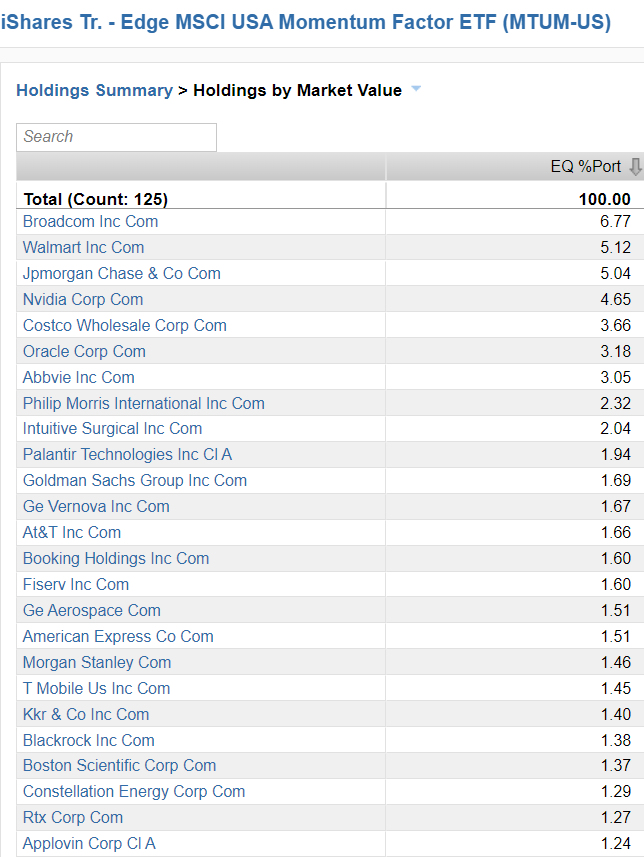

A look at the top 25 holdings of MTUM show the fund is under-exposed to Mag7 and big positions across sectors.

Risk On/Risk Off: Vol. Creeping Higher, Risk Gages Mixed

Risk gages have flattened out into year-end as rising rates dampened optimism around Fed. policy and the election. We would note that just as enthusiasm for equities eventually pushes rates higher, skepticism and selling within the equity market generally pushes them lower. This has been a persistent feedback loop in the current bull cycle back to 2023, and we could see it play out again. That’s why rates the direction of rates figures so prominently into our thinking.

VIX and MOVE Indices (chart below, panels 3 & 4) have bounced higher after the VIX spiked in mid-December. Since then Semiconductors (largely on the back of a blow-out quarter from AVGO) have made a bullish pivot. Discretionary is retracing gains vs. Staples, while Banks are in stasis vs. Utilitis after a big spike on election day.

In Conclusion

Equities have begun a modest correction since the Fed signaled hesitance to continue cutting its policy rate while Treasury Yields rise. The question of course is how deep will the current correction go before the buyer finds the sale appetizing. We think the longer-term bull trend will find its footing sooner rather than later as we are skeptical that rates can go higher against a backdrop of soft commodities prices and a cooling housing market. However, if rates resolve higher and equities continue in correction, we may be forced to change our tune.

Data sourced from FactSet Research Systems Inc.