March 20, 2026

The debate between Growth and Value in the current market is ultimately a debate about interest rates and inflation expectations. The Iran conflict has introduced a powerful new variable into that equation through higher oil prices, but the direction of rates—not just the level of crude—will determine which factor leads over the next month.

When 10yr “Real Rates” have moved above the 220bps level, Growth has eventually sold off.

At a fundamental level, Growth and Value respond very differently to changes in interest rates. Growth stocks, particularly in Technology and Communication Services, derive a larger share of their valuation from future cash flows. When interest rates rise, those future earnings are discounted more heavily, compressing valuations. Value stocks, by contrast, tend to be more near-term cash flow oriented, with a heavier presence in sectors like Energy, Financials, and Industrials. These sectors are less sensitive to discount rate changes and, in some cases, benefit directly from the conditions that push rates higher.

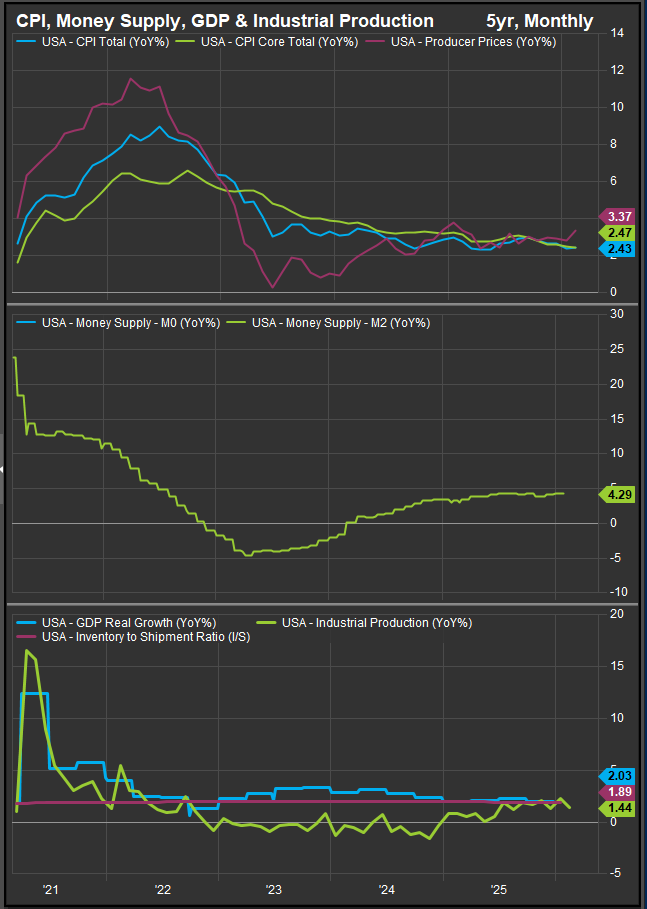

This is why the recent move in rates matters so much. Treasury yields have been drifting higher alongside oil, while market pricing for Fed easing has been pushed further out. The March FOMC reinforced this dynamic, with policymakers signaling a “wait and see” approach and acknowledging the uncertainty created by the Middle East conflict. At the same time, inflation data is beginning to firm again. Core PPI surprised to the upside, running at a 7.8% three-month annualized pace, while energy prices have turned from a disinflationary force into a renewed source of pressure.

If this trend continues, it creates a macro backdrop that favors Value—at least tactically. Sustained upward pressure on oil, particularly if crude begins to approach the $120–$150 range, would feed through into transportation costs, goods prices, and inflation expectations. That would likely push yields higher across the curve and reduce the probability of near-term Fed easing. In that environment, Energy and Financials would benefit from stronger earnings visibility, while Growth would face valuation headwinds from rising discount rates.

WTI Crude

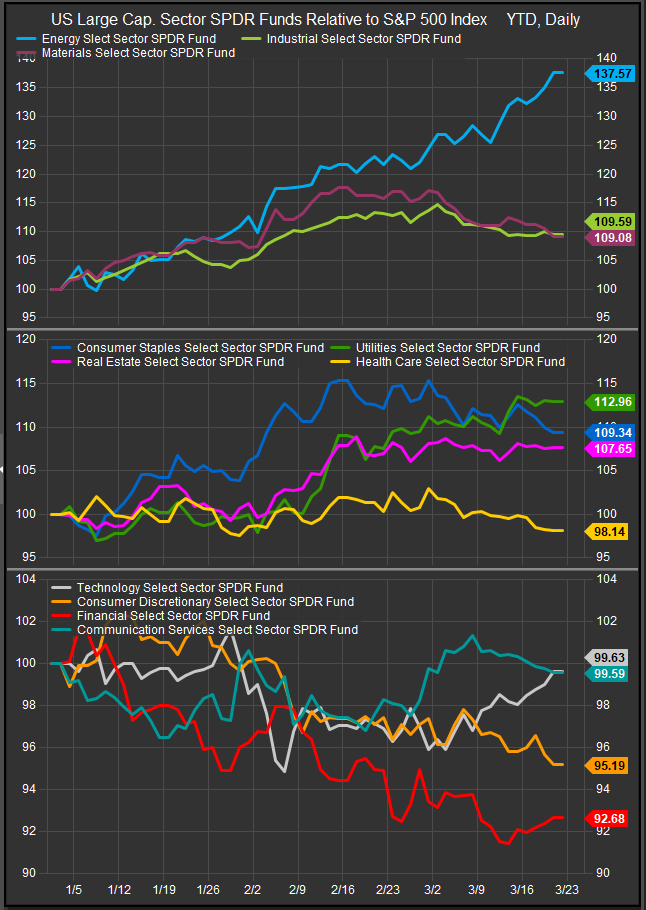

From a sector lens, the biggest allocation question regards Technology, Comm. Services and Discretionary sectors as clear Growth exposures. With the expansion of Technology stock multiples and focus on Mag7 throughout the cycle, the other 8 sectors have been skewed towards the Value as the market bifurcated between Mega Cap. Growth and “everything else” from early 2023-2025.

But the relationship is not linear, and the current environment is more nuanced than a simple “higher rates = Value wins” framework. Growth has held up well despite rising yields because its leadership is being driven by earnings momentum rather than multiple expansion. Technology sector earnings are still expected to grow at over 40% year-over-year, supported by AI infrastructure spending and strong corporate demand. That creates a buffer against moderate increases in rates, particularly if those increases are driven by supply-side shocks rather than demand overheating.

The key question, then, is what would push the macro environment more decisively toward an inflationary regime. The most obvious catalyst is a sustained disruption in global energy markets. If the Strait of Hormuz remains impaired for weeks, or if infrastructure damage spreads across the Gulf, oil prices could remain elevated or continue to rise. That would likely be accompanied by broader supply chain disruptions, higher shipping costs, and renewed pressure on food and goods prices. A second catalyst would be a reacceleration in wage growth or services inflation, which would signal that inflation is becoming more entrenched beyond energy. Finally, any policy response that adds fiscal stimulus into an already supply-constrained environment could further reinforce inflationary dynamics.

Despite stable CPI readings, the spike in commodities prices is concerning for Growth investors

In that scenario, interest rates would likely move higher and remain elevated, creating a more durable tailwind for Value. Financials would benefit from higher net interest margins, Energy from elevated commodity prices, and Industrials from defense and infrastructure spending tied to geopolitical realignment. Growth, particularly the more rate-sensitive segments, would face increasing pressure as discount rates rise.

On the other hand, there is a clear path to a more stable—or even lower—rate environment, which would tilt the balance back toward Growth. The most important condition would be stabilization in oil prices. If diplomatic or military efforts succeed in reopening the Strait of Hormuz and energy markets normalize, the inflation impulse from oil would fade relatively quickly. Even if crude remains elevated, a plateau rather than a continued rise would reduce upward pressure on inflation expectations.

In addition, continued moderation in core inflation—particularly in shelter and goods—would reinforce the disinflationary trend that had been in place prior to the conflict. Recent CPI data already shows shelter inflation easing, with rent growth slowing to its lowest pace in several years. If that trend continues, it could offset some of the pressure coming from energy. A softening labor market would also contribute, particularly if unemployment begins to drift higher toward or above the Fed’s 4.4% projection. That would reduce wage pressures and give policymakers greater confidence that inflation is under control.

Finally, clear communication from the Federal Reserve that it is willing to look through energy-driven inflation shocks would help anchor rate expectations. Powell has already hinted at this framework, noting that the Fed’s standard approach is to avoid overreacting to temporary energy spikes. If markets begin to believe that policy will remain stable despite higher oil prices, yields could stabilize or even decline, removing a key headwind for Growth.

The most likely near-term outcome is a range-bound rate environment with episodic spikes, rather than a sustained move sharply higher or lower. That suggests neither Growth nor Value will achieve clean dominance. Instead, leadership will rotate based on incoming data and headlines—oil prices, inflation prints, and central bank signals.

For investors, the implication is to focus less on binary factor bets and more on rate sensitivity within each factor. Growth exposures with strong earnings visibility and less reliance on multiple expansion should remain resilient even if yields drift higher. Value exposures tied directly to energy and financial conditions can perform well during inflation scares but may lose momentum if rates stabilize.

In the end, the Growth vs. Value debate is not being decided by geopolitics alone. It is being decided by how geopolitics feeds into inflation, and how inflation feeds into interest rates. That transmission mechanism is what will determine leadership in the weeks ahead.

-

FactSet / StreetAccount – Earnings growth expectations (S&P 500 ~11–12%, Technology ~40%+), macro summaries, and sector sensitivity to inflation and rates.

-

Bloomberg – Coverage of Treasury yield movements, oil price spikes tied to Iran conflict, and shifting rate-cut expectations.

-

Reuters – Reporting on Strait of Hormuz disruptions, energy-driven inflation risks, and central bank policy outlooks (Fed, ECB, BoE).

-

Federal Reserve (FOMC, SEP, Powell commentary) – Guidance on policy path, inflation risks, and willingness to “look through” energy shocks.

-

U.S. Bureau of Labor Statistics (CPI, PPI) – Data on inflation trends, including elevated core PPI and moderating shelter inflation.

-

International Energy Agency (IEA) – Analysis of global oil supply risks and energy market disruptions.

-

Goldman Sachs, JPMorgan, Morgan Stanley Research – Insights on factor performance, rate sensitivity of Growth vs. Value, and macro scenario analysis